Hotter Inflation Readings and Poor Treasury Auctions Put Recent Rally to the Test - Midday Macro – 10/13/2023

Hotter Inflation Readings and Poor Treasury Auctions Put Recent Rally to the Test - Midday Macro – 10/13/2023

Color on Markets, Economy, Policy, and Geopolitics

Hotter Inflation Readings and Poor Treasury Auctions Put Recent Rally to the Test

Midday Macro – 10/13/2023

Market’s Weekly Narrative and Headlines:

Happy Friday the Thirteenth, things got spooky this week, although the S&P managed to put in its first green week after five red ones despite the negative price action following a poorly received 30-year auction on Thursday. The overall sector and factor performance tilted more defensive, with the exception of energy, benefiting from the added geopolitical risk premium oil received since the terrorist attack by Hamas on Israel. Despite the increased rate volatility following the new long-end supply, 10yr yields were lower on the week, helped by a large body of Fed officials noting that higher yields and tighter financial conditions may reduce the need for a further rate hike in November. We cover this wide breadth of speakers in our Policy section, where we also look closer at the September FOMC minutes released this week. In general, it feels like the Fed is changing its tune on aggregate, seeing a more two-side risk management approach as warranted despite the stronger jobs report and now higher-than-expected inflationary readings, both of which had underlying aspects that reduced their headline urgency. With treasury auctions tailing, liquidity low there, and again, financial conditions very tight, priorities are now shifting away from being laser-focused on inflation and instead thinking about the “totality” of the picture, including financial stability concerns and continued uncertainty regarding the lagged effects of cumulative tighter policy to date will have on future growth. WTI ended the week near $88, helped by a rebound in domestic gas demand and worries that sanctions would be actually enforced. Growth fears subsided slightly, too, as Beijing looks to be finally admitting it needs a more centralist approach to stimulating the economy; however, copper continues to trend lower due to excess inventories and fewer worries regarding future production. The agg complex was little changed on the week, with no notable developments on the weather or the political front. Finally, the dollar rose towards the end of the week, with the $DXY jumping up to 106.7 despite increased dovish rhetoric from Fed officials.

Deeper Dive:

Fed officials have been changing their tune these last weeks, becoming more dovish due to the rise in longer-dated yields and tighter financial conditions. This was also echoed (and first heard in some ways) in the September FOMC’s minutes, released this week, which noted that “all participants” agreed it was appropriate to proceed carefully given the better balance of risks. As a result of this more balanced approach, the higher-than-expected inflation readings this week in the CPI and PPI reports shouldn’t change this more dovish tone, especially given the heavy influence energy and shelter price increases had. This allows for a more favorable backdrop for risk assets throughout the third-quarter earnings season. Further, a more dovish Fed reduces stagflationary fears given core inflation continues to trend lower while consumer spending, and hence growth, cools but does not fall off a cliff from overly tight policy. All else equal, consumer behavior should still be supported by a “resilient to pragmatic” labor market and historically strong household balance sheet. Lower inflation and slower growth, supporting a dovish Fed, will lead yields to retrace recent gains due to reduced “higher for longer” Fed expectations, which should create a positive feedback loop for bonds. Further, this will reduce real rates, weaken the rate differential supporting the dollar, and loosen financial conditions, supporting equities and credit. Typically, this lower growth outlook would also make us bearish on commodities, especially oil, but the current supply deficit and the added geopolitical risk premium should support prices. We also see China reaccelerating, at least more than expected, as Beijing capitulates, increasing a more coordinated and centrally driven fiscal and credit pulse that uncaps currently low consumer and business confidence, releasing more positive animal spirits there. We maintain our current mock portfolio positions and are adding a long Aussie Dollar position and a long S&P position, which we will explain in further detail below.

*Goldman sees policy, followed by growth, as driving the recent increase in yields, although we see the two heavily tied together

*The rise in yields and steepening of the curve has become the topic of choice for Fed speakers lately as they debate how rising term premiums might substitute for a rate hike

*Longer-dated Treasuries should benefit from an exit from the recent more stagflationary environment

*Xi and company are increasingly realizing they need to take more substantial action to reverse the damage done by zero-Covid, the common prosperity crackdown, and slower global growth more generally

As we wrote last week, following the significantly better-than-expect jobs report, there remains a road to lower inflation that does not necessitate a full-out recession. To be clear, we still believe a multi-quarter below-trend growth period is upon us, with consumers and businesses increasingly showing cracks, albeit in an uneven and rolling fashion. However, as we have stressed in past writings, this is precisely what is needed to move the Fed into the next phase of the cycle and eventually begin to move policy out of a restrictive stance next year and set policy at a neutral level to promote productivity more organically. Interestingly, businesses and consumers are in sync with the Fed’s vision, with current sentiment readings softer than future expectations. This was seen in today’s University of Michigan Consumer Sentiment readings, with one-year expected business conditions dropping notably while longer-run views were unchanged. Regional Fed PMI readings and the NFIB Small Business survey have generally echoed this acknowledgment that a slower period is coming but should be shorter-lived. As a result, we continue to see reduced pricing power by firms and reduced margin pressures as input costs, which have recently ticked higher, trend lower again due to falling capacity utilization pressures, easing demand and allowing a better balance with supply. At the same time, despite all the noise around labor strikes, wage growth is slowly normalizing, as aggregate real disposable income is now positive, reducing labor bargaining incentives (and power). As a result, and although we highlighted the importance of this week’s inflation data, which was hotter, and Treasury auctions, which could have gone better to say it politely, we maintain a view that the “totality of the data” allows for a more dovish Fed given where financial conditions are. As growth cools and inflation falls further, the Fed will reduce the duration they plan to stay restrictive, which will improve investor sentiment, increase risk appetite, and hence loosen financial conditions.

*Future business conditions and financial situation expectations show a better outlook further out.

*The NY Fed’s manufacturing surveys six-month ahead outlook for demand and activity continues to be significantly higher than current readings

*Small businesses have maintained a solid intention to keep hiring versus a falling overall optimism index reading

*The Atlanta Fed Wage Tracker resumed its move lower, with switcher wage gains approaching stayers, indicating less incentive for turnover

With the VIX touching above 20 today due to the continued selling pressure that intensified following yesterday’s poor 30-year Treasury Auction, the S&P moved into a negative gamma reading but found supportive call buying around the 4340 level. This level coincided with the bottom of the S&P’s October ’22 uptrend channel, and as a result, the technical and optionality picture looks more supportive going into next week, given the gamma tilt and longer-term channel support, along with the fact that the 4,400 area will have strong gravity (and resistance) into next week’s OPEX. Further, when zooming out to a multi-year perspective, there is a strong cup and handle formation, a bullish technical pattern. In combination with the above-discussed more positive fundamental macro views that we are at peak financial condition tightness, we want to increase our exposure to U.S. equities through a 20% long position in the S&P through the SPDR $SPY ETF in our mock portfolio, with the tactical target of a 5% gain by mid-November. Finally, although we have been wrong many times in reading the Chinese tea leaves, we see a shift in both the “official” data and Beijing’s fiscal stimulus posturing. As always, the picture is opaque, and the risk of geopolitical escalation lurks, leaving us not wanting to own any direct Chinese financial assets. Instead, we expect the increased use of fixed asset investment to stimulate growth to benefit the Australian Dollar as imports of raw resources from there increase. Relationships between the two nations are also on the mend, reducing worries of protectionist measures by China. Further, RBA is likely done tightening policy given the progress made on inflation even as the domestic economy has remained resilient with a still tight labor market, creating a wait-and-see approach. We expect November’s RBA new forecasts to maintain a hawkish tilt, supporting the Aussie dollar on top of the expected increased trade with and better investor sentiment towards China. As a result of this line of thinking, we are starting a 10% long position in the Invesco Currency Shares Australian Dollar ETF $FXA.

*The S&P is sitting on its longer-term uptrend, and the bottom of its “handle part” of a cup and handle formation, a pattern with a strong bullish hit rate

*Renmac sees sentiment as relatively bearish, entering an area that generally indicates a bullish reversal is coming

*Fundamentals for earning shave improved and as a result, the earnings “recession” may be over

*If the high for longer-dated yields are in, then stocks should perform well over the next month, according to Goldman

*Globally, the cycle is turning as an increasing number of central banks are shifting gears towards a more neutral to easier policy stance

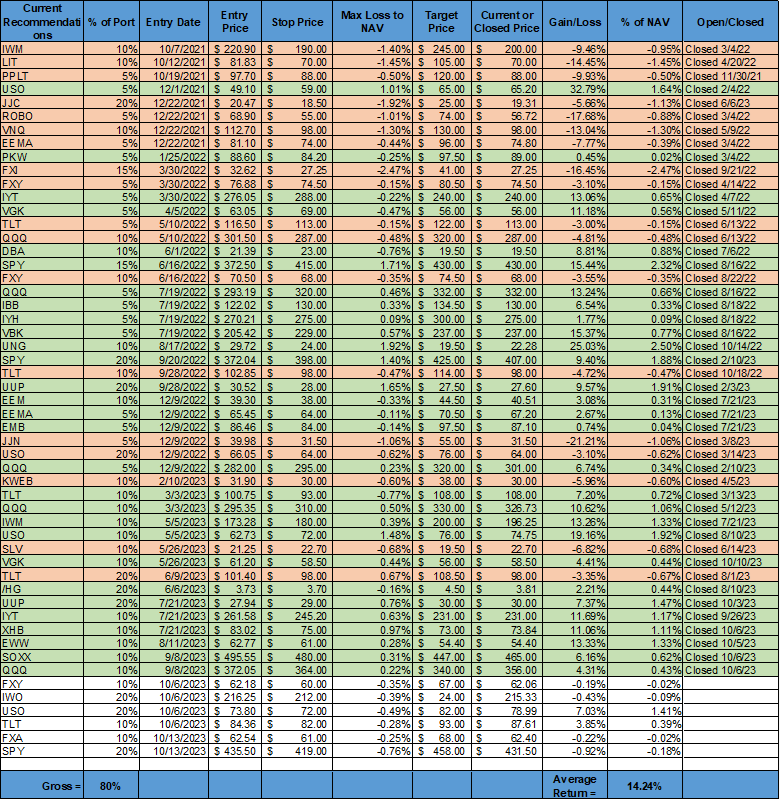

*This week’s price action increased the average return of our mock portfolio thanks to increases in our oil and long-end Treasury longs while our Yen long was flat and our small-cap growth long declined notably

As always, thank you for reading, and please share our newsletter. Feel free to reach out with any questions or comments. - Michael Ball, CFA, FRM

Policy Talk:

It was a busy week for Fed officials again, with around a dozen formal events and some policymakers speaking multiple times throughout the week. As always, we highlight a few specific speakers below, choosing Logan, Jefferson, Waller, and Collins while delving deeply into the September FOMC meeting minutes. A wide variety of topics were covered, but the overarching theme was Fed officials explaining how they interpreted the run up in bond yields and how it may affect their future policy decisions. San Francisco President Daly pontificated that the neutral rate, aka r*, might be structurally higher now while speaking at a town hall setting in Chicago, reinforcing a view that the Fed may stay higher for longer. Atlanta Fed Bostic reiterated his belief that rates were high enough given his outlook for the economy and inflation while speaking at the annual convention for American Bankers Association. Minneapolis Fed President Kashkari said he wasn’t yet convinced that the rise in long-term Treasury yields would lessen the need for further rate hikes while giving prepared remarks at Minot State University, “perplexed” by the run-up. NY Fed SOMA manager Perli covered how the implementation of tighter policy was working in the ample reserve framework world while giving a speech at the annual NABE meeting. Separate from the general economic and policy outlook rhetoric, Vice Chair Barr and Governor Bowman delved into regulatory reforms, speaking to changes to capital requirements and financial sector vulnerabilities and risk.

Dallas Fed President Logan gave prepared remarks titled “Financial conditions and the monetary policy outlook” before the 65th National Association for Business Economics annual meeting. She gave an overview of her economic outlook, highlighting “uneven” monthly progress on inflation, but still sees “encouraging” signs based on progress in three to six-month averages as well as core and trimmed-mean measures. Logan says it is still too soon to “say with confidence” that inflation is trending back to target in a timely manner. She highlighted that although the labor market has cooled, she still sees hiring conditions as tight, keeping wage growth “solid,” rising faster than would be consistent with 2% inflation. Logan noted that growth has been “broadly” surprisingly strong both in consumption and investment and recession fears have “faded.” However, she noted a mixed ability to pass through cost increases depending on the industry due to softening growth. As a result, regarding the appropriate policy, she still sees the risk tilted towards more persistent inflation and believes restrictive financial conditions will be needed for some time. She highlights how the cumulative policy tightening to date has translated into tighter financial conditions in recent months, mainly due to rising longer-dated yields. She decomposes the reason for these rises in yields, citing near and long-term expectations but mainly focusing on the rise in term premiums. Logan notes that the “resilience” of the economy likely indicates that the rate level needed to sustain price stability and maximum employment is higher. This coincides with a higher term premium due to possible structural changes, cooling the economy and reducing the need for additional rate rises in the front end. She concludes with the caveat that it is hard to know exactly why term-premium yields rise or fall, and she is currently getting a somewhat mixed message. She ends by reiterating that inflation is her focus, and restrictive financial conditions will be needed, but they have recently tightened, reducing the need for further policy tightening.

“Data such as the quits rate, the ratio of vacancies to unemployed workers, and surveys of consumers and businesses show progress toward better balance. Many of these measures are near or at 2019 levels. However, 2019 was a very strong labor market. Conditions like those of 2019 don’t necessarily mean labor supply and demand are in balance.”

“I expect that continued restrictive financial conditions will be necessary to restore price stability in a sustainable and timely way. I remain attentive to risks on both sides of our mandate. In my view, high inflation remains the most important risk. We cannot allow it to become entrenched or reignite.”

Fed Vice Chair Jefferson spoke at the 65th Annual Meeting of the National Association for Business Economics in Dallas, where he delivered a speech titled “U.S. Economic Outlook and Monetary Policy Transmission,” discussing his outlook on the economy, what he believes is coming, stressing the need for the Fed to proceed carefully. Jefferson reviewed the progress made on inflation, believing it would moderate further, especially in core services, ex-shelter. He noted evidence that labor markets were coming into better balance despite September’s strong NFP, citing improvements in supply due to a better participation rate and higher levels of immigration. On aggregate, he saw the third quarter as resilient but expected a slowing in growth “this fall.” Jefferson continues to see upside risk to inflation but sees “important downside risks to economic activity” coming from abroad. He went on to highlight the impact of tighter financial conditions, aka higher interest rates, affecting risk premiums and altering investor's behavior, reducing future growth potential. He sees these higher rates as increasingly hitting in the next year when an increasing amount of corporate debt needs to be rolled. Because of his view on the lagged effects of tighter policy on real economic activity, Jefferson believes the Fed should move forward more cautiously, with the balance of risks between not tightening enough and overtightening equal. Moving forward, he stressed he will be “cognizant of the tightening in financial conditions through higher bond yields and will keep that in mind as I assess the future path of policy.”

“Given that this additional tightening is in train, it may be too soon to say confidently that we've tightened enough to return inflation to our 2 percent target. At the same time, I will be mindful of the additional tightening in train because of our past rate hikes as I consider whether there is a need to tighten policy further in the future.”

“After increasing the target range for the federal funds rate by 525 basis points since early 2022, my view is that the FOMC is in a position to proceed carefully in assessing the extent of any additional policy firming that may be necessary. We are in a sensitive period of risk management, where we have to balance the risk of not having tightened enough against the risk of policy being too restrictive. The balancing of these two risks was a good reason for holding the policy rate constant at our most recent FOMC meeting.”

Governor Waller gave a speech titled “Monetary Policy Analysis and the Development of Federal Reserve Policymaking” at the conference sponsored by the Mercatus Center at George Mason University. Waller looked back on the works of Bennett McCallum, a person whose monetary policy research on the 1970s he admired and likened to his own works. Waller established Volker's actions as changing the Fed's credibility, furthered by the great moderation period brought on by Greenspan. Waller attributed an explicit policy target combined with communication of its policy rule to the public as the reason the Fed regained credibility in the 90s. Since then, further reforms have made the FOMC’s policy framework more “explicit” due to the introduction of things like the Statement of Long-Run Goals, strengthened by an inflation target. The addition of the official policy statement, a press conference, and the Summary of Economic Projections also increased transparency. Waller gave his views on how each of these developments increased the strength of monetary policy. Although this speech was more of a historical look back on the reforms that occurred over the last three decades, it also enforced why Waller believed what he did concerning where and why policy should be where it is. We recommend reading the speech as it provides a methodical look at the evolution of policy reform and why Hawks feel emboldened to rely on rule-based approaches.

Boston Fed President Collins delivered a rather long speech titled “Reflections on Phasing Policy Amidst (Pandemic) Uncertainty” at a Goldman Lecture in Economics event at Wellesley College. Collins began her remarks by focusing on the various forms of uncertainty that the pandemic presented, highlighting how problems with measurement issues, changing correlations, and understanding unforeseen events increased uncertainty. She believes policymakers need to address increased uncertainty differently depending on the situation, as was seen throughout the current cycle during the pandemic. Further, Collins noted that the uniqueness of the pandemic made it harder to relate at the time on the ground circumstances to previous cycles, noting the size of the supply shock brought policymakers into uncharted territory. Collins highlighted the recent resilience of the economy as being one of the unexpected developments. However, she believes we are entering the next phase of the cycle, with continued uncertainty now forcing the Fed to move more cautiously despite inflation being persistently too high. As a result, she stressed the need to keep policy restrictive until it was clear that inflation was moving back to target, something she does not see yet. Overall, Collins says she is “realistic about the economic uncertainties and risks but optimistic that price stability will be restored due to an orderly slowdown in activity and only a modest increase in the unemployment rate,” an outcome she sees as consistent with both parts of the Fed’s dual mandate. She concludes her remarks by noting on how she judges the Fed’s progress, looking at the trends that “show both sustained reductions in inflation and progress on the underlying goal of realigning supply and demand.”

“Household balance sheets have been solid, partially due to savings accumulated during the pandemic, and corporate cash holdings have been elevated due in part to locking in financing at previously low rates. Factors like these have likely made the economy less interest-sensitive than during past tightening cycles.”

“While the unemployment rate remains near historic lows, there is some evidence of demand becoming better aligned with supply in the labor market. Despite the September jump in employment, growth in payrolls this year has slowed relative to last year, though it is still significantly above trend. The previously very high voluntary quit rate has fallen to pre-pandemic levels. Lower, though still high, job vacancies are also consistent with a gradually cooling labor market. We are also seeing promising developments in terms of labor supply as labor force participation has increased, especially for prime-age workers (those aged 25 to 54).”

The Federal Reserve released the September FOMC Minutes this week, with the main takeaway being the recent resilience of the economy is adding to the upside risks to inflation, driving expectations that policy will likely need to stay in restrictive territory longer than previously anticipated. The FOMC saw this clearest in higher, longer-dated Treasury yields, indicating a greater term-premium, supporting a general tightening in financial conditions, which was also supported by lower equity prices and a stronger dollar. The committee noted that yield increases were generally driven by rises in real rates, with inflation expectations remaining well anchored, but there were other factors at play, too. However, a reduced need to take on new or refinance debt led to a delayed pass-through of tighter policy/higher rates on the household and corporate sectors, increasing the lag effect of the cumulative policy tightening to date. The staff’s review of the economic situation showed the economy was rising “at a solid pace,” supported by a broad private domestic final purchasing pulse, while the import/export picture improved. The staff saw job gains slowing but remaining strong, helping reduce labor market tightness and wage pressures. The staff noted that inflation remained elevated but “continued to show signs of slowing.” Foreign economic growth was seen as a greater headwind, with data pointing to “a continued subdued pace of economic activity abroad.”

“Available indicators suggested that real GDP was expanding at a solid pace in the third quarter. Private domestic final purchases—which includes PCE, residential investment, and business fixed investment (BFI) and often provides a better signal of underlying economic momentum than does GDP—also looked to be rising solidly, led by gains in both PCE and BFI.”

The staff’s review of the financial situation highlighted that tighter financial conditions occurred during the intermeeting period while funding markets remained stable. Borrowing rates “increased moderately,” while credit conditions “appeared to tighten somewhat,” with loan balances falling. However, the staff reported credit was “available for most consumers,” with credit card balances growing and mortgage availability little changed. Capital markets also made credit generally available, although issuance fell. Overall, credit quality weakened further but remained “broadly solid,” with delinquency rates little changed.

“Credit was available for most consumers. Credit card balances grew in the second quarter through late August. For residential real estate borrowers, credit availability was little changed. Credit conditions for small businesses were also fairly stable.”

The staff upgraded its economic projection at the September meeting compared to July, with consumer and business spending being more resilient to tighter financial conditions than previously expected. However, growth was expected to fall into year-end due to UAW strikes and higher interest rates, although the effects were highly uncertain. Forecasts for the next three years expected real GDP to be weaker, below potential, due to the lagged effects of tighter policy. At the same time, expectations for a better balance of supply and demand for products and labor meant inflation would continue to trend lower. However, the staff viewed the uncertainty around these projections as “considerable.”

“In all, the staff projected that real GDP growth in 2024 through 2026 would be slower, on average, than this year and would run below the staff’s estimate of potential output growth, restrained over the next couple of years by the lagged effects of monetary policy actions.”

FOMC participants submitted their economic and policy rate projections at the September meeting, where much of the staff’s assessment was reaffirmed. Participants judged policy was restrictive, “restraining the economy, but inflation was still unacceptably high, and they needed further evidence that it was “clearly on a path” to target. However, in their discussion, despite consumer spending resilience over the intermeeting period, “many participants” saw household coming under greater pressure due to declining savings and “greater reliance on credit to finance expenditures,” with a few noting rising delinquency rates and greater price sensitivity. The business sector was seen as “solid,” due to improved hiring conditions, better supply chains, and reduced input costs. However, a “few” participants commented that district contacts were having reduced pricing power and believed business activity would soften over the coming quarters due to higher interest rates, although banking stress earlier in the year was having a reduced effect than originally feared. Participants saw a loosening in labor market conditions, helped by greater participation, but “many” saw it still historically tight in certain sectors. Finally, inflation was seen as “generally” slowing, with expectations still well anchored. However, core-services ex-housing remained problematic. Overall, Fed officials noted a high level of uncertainty around their forecasts, similar to the staff, covering various reasons why.

“In their consideration of appropriate monetary policy actions at this meeting, participants concurred that economic activity had been expanding at a solid pace and had been resilient. While the labor market remained tight, job gains had slowed, and there were continuing signs that supply and demand in the labor market were coming into better balance. Participants also noted that tighter credit conditions facing households and businesses were a source of headwinds for the economy and would likely weigh on economic activity, hiring, and inflation. However, the extent of these effects remained uncertain.”

The minutes concluded by stating current economic conditions, coupled with the “significant cumulative tightening” in policy and the “lags with which policy affects economic activity and inflation,” drove “almost all” participants to agree it was appropriate to maintain rates at their current level of 5¼ to 5½ percent at the September meeting. The committee “judged” that policy was restrictive enough and wanted further “time to gather additional data to evaluate.” However, “a majority of participants judged that” one rate increase at a future meeting would “likely be appropriate.” However, a “vast majority” of participants continued to judge the future path of the economy as highly uncertain and wanted to proceed carefully.

“Participants generally judged that, with the stance of monetary policy in restrictive territory, risks to the achievement of the Committee’s goals had become more two-sided. But with inflation still well above the Committee’s longer-run goal and the labor market remaining tight, most participants continued to see upside risks to inflation.”

U.S. Economic Data:

Consumer prices increased by 0.4% in September, easing from a 0.6% advance in August but exceeding market expectations of a 0.3% MoM rise and keeping the annual rate at 3.7%. Core consumer prices rose by 0.3% in September, the same as August and in line with market expectations, moving the annual core rate lower to 4.1% YoY from 4.3% in the prior month. Energy rose 1.5% MoM (vs. 5.6% MoM in August), driven higher by Energy Commodities rising by 2.3% MoM (vs. 10.5 MoM%), while Energy Services increased by 0.6% (vs. 0.2% MoM). Food prices rose by 0.2% MoM for the third month in a row, with Food at Home falling slightly while Food Away from Home rose slightly. Core Goods decreased by -0.4% MoM (vs. -0.1% MoM), with New Vehicles higher by 0.3% MoM, the same as last month. However, Used Cars fell by -2.5% MoM (vs. -1.2% MoM), and Apparel was lower by -0.8% MoM (vs. 0.2% MoM). Shelter prices rose 0.6% MoM (vs 0.3% MoM), with Rents and OER up 0.5% MoM (vs. 0.4% MoM) and 0.4% MoM (vs. 0.5% MoM), respectively. Core services CPI, excluding Shelter, rose 0.6% MoM (vs. 0.4% MoM in August), driven higher by Transportation Services rising by 2% (vs. 0.3% MoM) due to a 4.9% increase in airfares and a 2.4% increase in Motor Vehicle Insurance. Finally, Medical Care rose by 0.3% MoM after several months of flat to negative readings.

Key Takeaways: Headline CPI came in hotter than expected due to rises in energy prices, mainly gasoline. However, core CPI continued to exhibit a notable disinflationary trend, with the three-month annualized rate falling to 3.1%, the lowest three-month annualized core rate since September 2021, versus a 4.1% official annual rate. As a result, and assuming this translates even more favorably to core PCE, this report's higher-than-expected results are not a game changer regarding whether the Fed decides to hike again in November. Of course, numerous Fed speakers have reaffirmed since the September FOMC meetings and the message received this week from that meeting’s minutes that they are still unconvinced that inflation is trending back to target in a timely manner. This view will be boldened by increases in alternative CPI measures from the Cleveland and Atlanta Fed’s. The Cleveland Fed’s Median CPI rose by 0.5% MoM (vs. 0.3% MoM in August) in September to 5.5% YoY rate, a decrease from 5.7% in August, while their Trimmed-Mean CPI rose by 0.4% MoM (vs. 0.3% MoM), a decrease to 4.3% YoY rate, from 4.5%. Further, the Atlanta Fed’s Sticky-Price CPI index increased to 5.5% YoY in September from 4.7% in August. Their flexible cut of the CPI increased by 3.9% YoY, up 1.0 percent on a year-over-year basis from August's reading. As a result, although the September CPI report may not warrant a further rate hike in isolation, it does support the need for the Fed to continue to stress the need to remain in restrictive territory for an extended period of time. Finally, shelter again accounted for the majority of the rise in September’s core reading, with the expected declines not yet materializing, increasing the uncertainty of the lagged effects the official data has in capturing price declines, which already occurred according to private data. In theory, the Fed should be looking through this because ex-shelter headline and core measure are now at 2% YoY, but in reality, it has not been.

*Increases in Shelter costs again made up the majority of headline and core increases on the month

*On an annual basis, Core CPI continues to trend lower, with Core Services ex-housing, resuming its downward momentum

*Rises in gas and stronger-than-expected shelter costs helped headline beat expectations.

*Without shelter, both headline and core CPI would be at 2% on an annualized basis

*Transportation costs continue to support supercore readings, although there was little change in the contribution from last month, more generally

*CPI shelter cost measures have diverged from private data, with Zillow’s Observed Rent Index indicating a drop should be coming

*The Clevland Fed’s Median and Trimmed Mean measures continue to fall at an annualized rate, but there was an uptick in the monthly readings in September

*The Atlanta Fed’s Sticky and Flexible CPI measures firmed in September, although Sticky is gradually trending lower

Producer prices rose by 0.5% in September, following a 0.7% rise in August, and above market forecasts of a 0.3% MoM increase, moving the annual headline rate to 2.2% YoY from 2% YoY in the prior month. Core PPI rose by 0.3% in September, following a 0.2% rise in August, and above market expectations for a 0.2% rise, moving the annual core rate to 2.7% YoY from 2.5% YoY in the prior month. Goods prices increased by 0.9% MoM, with nearly three-quarters of the increase due to a 3.3% increase in final demand energy prices, driven by a 5.4% surge in gasoline costs. However, food prices also increased by a notable 0.9% MoM after decreasing by -0.5% in August, driven by increases in meat costs. Core final demand goods prices only rose by 0.1% MoM. Final demand service prices rose by 0.3% MoM, slightly higher than the 0.2% increase in August due to an acceleration in trade (0.5% MoM vs. 0.2% MoM in August) prices, while transportation and warehousing costs (-0.4% MoM vs. -0.3% MoM) and “other’ was unchanged at 0.3% MoM. Intermediate demand prices for processed goods rose by 0.5% MoM, unprocessed goods rose by 4% MoM, and intermediate service prices rose by 0.3% MoM.

Key Takeaways: Increases in energy costs resulted in headline PPI rising more than expected, while food prices also reaccelerated to a lesser extent. Less food and energy gains were much weaker, with core service final demand prices increasing the same amount as in August, while “nonfood materials less energy” in processed and unprocessed goods were negative on aggregate. As a result, given the decline in energy seen over the last weeks, we don’t see this report as indicating a reacceleration in inflation is meaningfully occurring. However, it is notable that all four stages of intermediate demand saw broad increases in good and service input prices. As a result, in totality, this report will increase the inflation forecasting uncertainty currently being expressed by Fed officials, given the increased, albeit mainly energy-related, inflationary pipeline pressure.

*Headline PPI beat expectations, helped again by large increases in energy-related prices and a firming in services.

*Core PPI also beat expectations, but the underlying subindexes showed a mixed picture, with intermediate demand readings falling

Import prices increased by 0.1% in September, slowing from an upwardly revised 0.6% increase in August and below forecasts of a 0.5% MoM rise, moving the annual rate to -1.7% YoY from -2.9% YoY in the prior month. Imported fuel costs increased by 4.4% MoM after rising by 8.8% in August as higher prices for petroleum (4.9% MoM vs. 9% MoM in August) offset the natural gas prices decline (-7.8% vs. 13.4% MoM). Excluding nonfuel imports, import prices declined by -0.2% MoM, due to lower costs for foods, feeds, and beverages (-1.3% MoM vs. 0.7% MoM in August), the largest fall since August 2022, mainly due to lower prices for fruits. Elsewhere, declines were seen in nonfuel industrial supplies and materials (-0.5% MoM vs. -0.7 MoM), while capital goods (-0.1% MoM vs. -0.1% MoM) and automotive vehicles (-0.1% MoM vs. 0.0% MoM) were little changed. Export prices increased by 0.7% in September, above market expectations of a 0.5% MoM increase and following a downwardly revised 1.1% increase in August. On an annual basis, export prices fell by -4.1% YoY in September, compared to -5.7% YoY in August and the least since February. Prices for nonagricultural exports rose by 1% MoM (vs. 1.5% MoM in August) due to increases in prices for industrial supplies and materials (2.2% MoM vs. 3.5% MoM), automotive vehicles (1% MoM vs. 0.3% MoM), and capital goods (0.1% MoM vs. 0.1% MoM). Prices fell for consumer goods (-0.3% MoM vs. -0.3%) and nonagricultural food (-2.7% MoM vs. -1.3% MoM). On the other hand, prices for agricultural exports (-1.1% MoM vs. -2.1% MoM) declined due to lower prices for soybeans, corn, wheat, and meats.

*Less favorable base effects and a stronger August increase are moving the annual rate higher for both Imports and Exports Prices

*Agriculture Prices declined for a second month with broad declines across various sub-categories

Wholesale inventories declined slightly by 0.1% in August, following a -0.2% decline in July and in line with estimates. Nondurable goods inventories dropped by -0.4% MoM after remaining unchanged in July, led by falling stocks of apparel (-2.6% MoM), chemicals (-2.4% MoM), and drugs (-0.6% MoM). On the other hand, durable goods stocks were unchanged, following a -0.4% decline in the previous month, as rising inventories of autos (2.1% MoM), hardware (0.7% MoM ), and machinery (0.6% MoM) were offset by decreases in stocks of electrical (-1.8% MoM), metals (-1.7% MoM), furniture (-1.4% MoM). Retail trade inventories rose by 1.1% MoM, driven higher by a 2.3% MoM increase in motor vehicle & part dealers. Sales at wholesalers jumped 1.8% in August, the largest increase since June 2022, after increasing 1.2% in July. At August's sales pace, it would take wholesalers 1.36 months to clear shelves. That was the lowest ratio since October 2022 and was down from 1.39 months in July.

Key Takeaways: This was the ninth consecutive month of either stagnant or decreasing stock levels. However, expectations are for business inventories to boost gross domestic product in the third quarter after being neutral in the second quarter and a notable drag in the first quarter. With that said, August will not be contributing to those expected gains as excluding autos, wholesale inventories fell by -0.4%, and this is the component that goes into the calculation of GDP. Looking forward, the low inventory-to-sales ratio indicates new orders for durables should increase over the next quarters, all else equal. With end demand expectations falling, this ratio could remain below normal historical levels for some time, reducing its normal signaling power.

*Wholesale inventories continue to contract for much of this year while sales have been notably rising in the last two months

The NFIB Small Business Optimism Index decreased to 90.8 in September from 91.3 in August and well below market forecasts of 91.4. Five of the ten index components increased, four decreased, and one was unchanged. Twenty-three percent of owners reported that inflation was their single most important problem in operating their business, unchanged from last month and tied with labor quality as the top concern. This was followed by 9% citing labor costs as their top business problem.

A net -8% of owners reported higher sales over the past three months, up 6 points from August’s reading. -13% of owners expect higher sales, an increase of one point. However, owners expecting better business conditions over the next six months deteriorated six points to a net negative -43%. The frequency of reports of positive profit trends was a net -24%, up 1 point from August. Among owners reporting lower profits, 29% blamed weaker sales, and 20% blamed the rise in the cost of materials. For owners reporting higher profits, 55% credited positive sales volumes.

A net 43% of owners reported job openings they could not fill, up 3 points from August. Filling open positions is most challenging in the construction, retail, manufacturing, and services sectors. 61% of owners reported hiring or trying to hire in September, down 2 points, with 18% planning to create positions, up 1 point. 36% of owners reported raising compensation, unchanged from August, while 23% of owners plan to raise compensation in the next three months, down 3 points from August.

A net 29% of owners raised their average selling price, an increase of 2 points from August. Unadjusted, 13% (up 1 point) reported lower average selling prices, and 41% (up 3 points) reported higher average prices. Price hikes were most frequent in finance, construction, and retail sectors. 30% of owners plan to raise prices moving forward.

A net -3% of owners reported inventory gains, an increase of 4 points, with -4% reporting current inventory stocks as “too low” in September, up one point from August. -1% of owners plan inventory increases in coming months, down one point from August. A net 57% of owners reported capital spending in the last six months, up one point from August, with the majority purchasing new equipment. 24% plan capital outlays in the next few months, unchanged from last month.

A net 2% of owners reported that their borrowing needs were not satisfied, unchanged from August, with 65% saying they were not interested in a loan. However, 8% reported their last loan was harder to get, up four points since August. The average rate paid on a short-maturity loan was 9.8%, 0.8 of a percentage point above last month.

Key Takeaways: This was the lowest reading in four months for the overall index, with the optimism index falling while the uncertainty index rose. The NFIB Small Business Optimism Index has been signaling a recession for over a year, with commentary this month saying, “The economy is skating on thin ice, cracks have appeared, but there has been no significant crash through the ice.” Still, the third quarter was stronger than expected, with investment and consumption remaining resilient, while housing also held up better than expected, given affordability issues. Moving forward, this may increasingly change as inflation and finding qualified workers remaining top concerns among small business owners as compensation increases remain near record levels. Further, despite a growing need, investment is at historically low rates as profits have been squeezed, financing costs have more than doubled, and the federal regulatory burden has increased. “Owners remain pessimistic about future business conditions, which has contributed to the low optimism they have regarding the economy. Sales growth among small businesses has slowed, and the bottom line is being squeezed, leaving owners few options beyond raising selling prices for financial relief”, said Bill Dunkelberg, the NFIB’s chief economist.

*The overall NFIB Small Business Optimism Index declined for a second month in a row, reaching a four-month low

*The softer components of the Optimism Index continue to weigh on the outlook

*The Uncertainty Index continues to trend higher, coinciding with decreases in the headline index

The University of Michigan's Consumer Sentiment fell to 63 in October from 68.1 in September, the lowest in five months and missing market estimates of 67.2, preliminary estimates showed. The Current Economic Conditions sub-index fell to 63 from 68.1, while the Consumers’ Future Expectations sub-index retreated to 60.7 from 66. Year-ahead inflation expectations rose to 3.8% from 3.2% in September, the highest level since May 2023, and the five-year outlook increased to 3% from 2.8%.

Key Takeaways: Sentiment fell notably in October’s preliminary reading after moving sideways since August. Consumers looks to be more concerned about inflation again due to the persistence of gas prices staying elevated at the pump while food costs have not fallen enough. Nearly all demographic groups posted setbacks in sentiment, reflecting the continued weight of high prices This renewed focus on inflation weighed on personal finance views in October’s report, which declined by -15% MoM, while one-year expected business conditions also fell by a notable -19%. However, long-run expected business conditions were little changed, suggesting that consumers believe the current worsening in economic conditions will not persist. Add in growing headlines of labor strikes, a new war in the Middle East, worries regarding government shutdowns, and the resumption of student loan payments, and it is not surprising confidence is falling. Higher rates are also likely playing a role on weighing on sentiment.

* Consumer Sentiment plunges 7.5% to 63 in October, reflecting increased worries over inflation, price level fatigue, and worse expected biz conditions

* One-year inflation expectations jumped 0.6 ppts to 3.8% in October, the biggest jump in half a year.

*Although prices are rising by less, the persistence of higher prices is increasingly weighing on the consumer’s outlook

The New York Fed’s October Survey of Consumer Expectations showed inflation expectations increased slightly in the short and medium term while labor market expectations were mixed with unemployment expectations deteriorating and perceived job loss risk improving. Households’ perceptions and expectations for income increased while spending was unchanged. Perceived credit conditions deteriorated slightly.

Median inflation expectation increased by 0.1 and 0.2 percentage points at the one- and three-year-ahead horizons to 3.7% and 3.0%, respectively. In contrast, median inflation expectations decreased by 0.2 percentage points to 2.8% at the five-year-ahead horizon. Inflation uncertainty increased slightly across all three horizons. Home, gas, medical, and rent price growth expectations fell slightly to 3%, 4.8%, 8.8%, and 9.1%, respectively, while year-ahead expectations for food increased to 5.6%.

Median year-ahead earnings expectations increased slightly to 3%, remaining in a narrow range since September 2021. Total unemployment expectations increased to its one-year average, while the perceived probability of losing your job decreased to 12.4%, slightly above its one-year average. The probability of leaving your own job voluntarily fell to 18.2%, while the probability of finding a job increased to just below its one-year average.

Median household income growth increased slightly to 3% but remained below its one-year average of 3.5% while spending growth remained unchanged at 5.3%. Perceptions about household current financial situations deteriorated slightly. However, year ahead outlooks improved. Perception of current and future credit access worsened, with the percentage of respondents expecting tighter credit conditions in a year increasing. Respondents also saw higher rates as more likely.

Key Takeaways: Inflation expectations were little changed in totality, with shorter-term overall expectations rising slightly but individual items one year ahead decreasing. Similarly, expectations for overall unemployment rose while earnings and individual perceptions of job security improved. This view was further bifurcated by the fact respondents said they were less likely to leave their jobs but also believed finding a job was easier. Respondent income security increased slightly while spending intentions were unchanged, but altogether, the new series on current financial security worsened slightly, likely driven lower by expectations that credit access at more costly rates would be harder. This report did not raise any red flags regarding the state of the consumer, indicating that the economy was not in imminent danger as the consumer’s “perceptions” were, on the aggregate, little changed.

*Shorter-tem inflation expectations ticked up slightly in September

*Job security sentiment was more mixed in September’s broad SCE readings

The Atlanta Fed's Wage Growth Tracker moved to 5.2% in September, down slightly from a 5.3% reading for August. The annual wage growth for job switchers moved to 5.6%, the same as in August, while those staying in their jobs saw their annual wage growth decrease to 5.0% from 5.2% in the prior month.

*Job switcher gains are falling to meet the overall index

Technicals, Positioning, and Charts:

The S&P outperformed the Russell and Nasdaq on the day. Factor and sector performance on the week favored energy, followed by a more defensive tilt, as expected, with the sell-off and rise in volatility. Outside of the Energy sector, Utilities and Real Estate outperformed, while High Dvd Yield and Low Volatility factors were the best performing. Small-caps were the worst performing factor, and Consumer Discretionaries were the worst performing sector. Finally, Large-Cap Growth was the best-performing size vs. value/growth combo on the week.

@Koyfin

S&P optionality strike levels have the Zero-Gamma Level at 4357 while the Call Wall is 4400 and the Put Wall is 4200. The S&P moved deeper into negative gamma, with the QQQs seeing the greatest weakness as it crossed under the volatility trigger level of 369, with SPY taking less than half that damage and finding support at its key gamma strike at 430. However, more generally, the SPY and QQQ both lost their volatility trigger level today and violently so, which is concerning for bulls moving forward. Finally, when implied correlation is high as it currently is, and many stocks are moving in the same direction, it is easier for volatility to increase, and this is what happened at the end of this week. Volatility skew is up, and today's major volatility outliers were put tails (very low deltas) and vol of vol (demand on implied volatility itself).

@spotgamma

S&P technical levels have support at 4355, then 4330, with resistance at 4380, then 4525. The latest rally, which started after last week’s NFP, lasted four days, totaling 187 points and making it the largest four-day green stretch of the year despite the end-of-the-week weakness; this was the first green week after five red ones for the S&P. The S&P has retraced half of this rally and is now in a failed breakdown/breakout trap pattern, potentially allowing markets to grab liquidity and trapping shorts, forcing a squeeze. Big picture structures are still the yellow triangle, at 4445, which is strong resistance now. The 4420 area is the backtest line that needs to be recaptured and may remain a key pivot zone given the gravity 4400 has. Finally, 4320 remains the core bull market uptrend line and is now the bull/bear line, as a move below puts bears in charge.

@AdamMancini4

Treasuries are higher on the day, with the 10yr yield lower by 9 bps to 4.61%, while the 5s30s curve is lower by 5bp on the session, sitting at 11.5 bps.

Four Key Macro House Charts:

Growth/Value Ratio: Growth is little change on the day and higher on the week, with Large-Cap Growth the best-performing size/factor on the week.

Chinese Iron Ore Future Price: Iron Ore futures are higher on the day and the week.

5yr-30yr Treasury Spread: The curve is flatter on the week.

EUR/JPY FX Cross: The Yen is stronger on the day and the week.

Other Charts:

The BofA Bull & Bear Indicator's latest reading is a 2.2, a neutral reading bordering on extremely bearish.

Active managers increased exposure over the past week according to the NAAIM Exposure Index, which rose from 36.2 to 45.8.

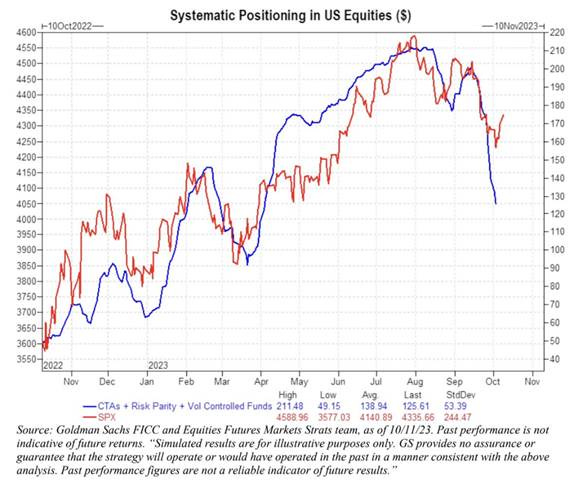

CTAs now present asymmetric upside risk after selling -$75bn in US equities over the last month and -$137B globally. This is the largest (and fastest) one-month change on record. In an up tape, GS estimates CTAs have $84bn in S&P futures to buy." said GS Scott Rubner. He also noted that when combined with risk parity and vol control, we are at a large divergence between positioning and price action, asking was the selling too fast?"

"Margins are expected to improve for the second straight quarter in 3Q." - BofA

"We expect S&P 500 margins will trough at 11.2% in 2023 but remain below the 2021 record high of 11.8% through 2025." - Goldman Sachs

"The distribution of single stock valuations for the Russell 2000 small-cap index is already comparable to previous market bottoms...while the S&P 500 distribution still looks different compared to previous lows." - @VrntPerception

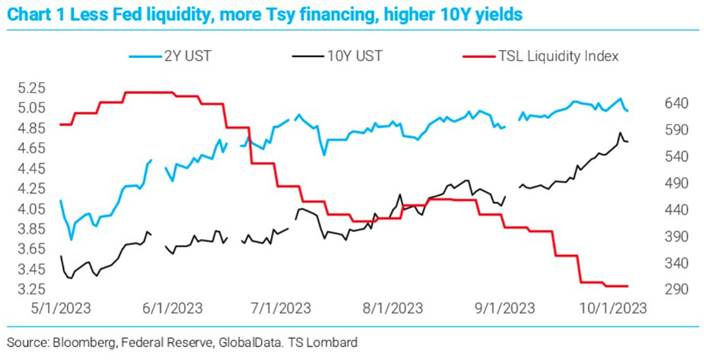

"The Fed is taking advantage of QT combining with a refinancing of Treasury to tighten the long end of the market, and a passively rising real funds rate." - @TS_Lombard

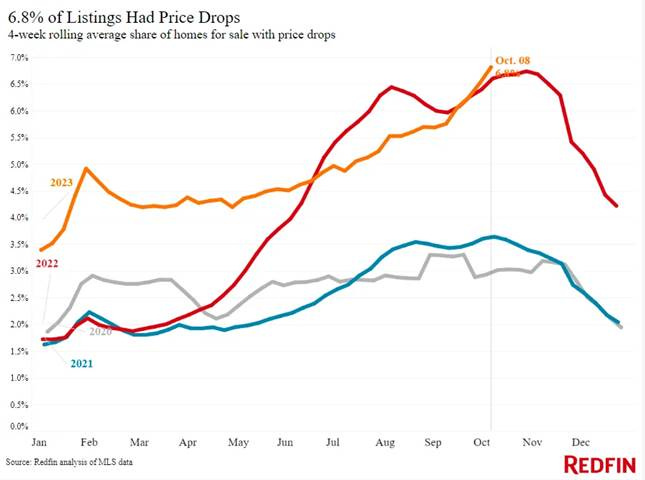

Despite the tight supply propping up prices, there are increasing indications that the housing market is cooling.

"The share of for-sale homes with a price drop at its highest level in nearly a year." According to @Redfin via @dailychartbook

Implied gas demand shot back up this week after fallin last week, sending oil prices lower.

IEA sees early signs of ‘demand destruction.’ However, it still forecasts global oil demand to grow by 2.3m b/d in 2023, followed by a 0.9m b/d in 2024. The market remains in deficit, but will turn into a surplus in the first half of next year." – IEA via @dailychartbook

GDI is indicating a more subdued growth backdrop versus GDP, while Citi sees total spending contracting notably

Mortgage loans on apartment buildings that are three months or more past due or in foreclosure are rising as rent growth has slowed, vacancy rates have increased, and interest rates have increased sharply. However, single-family delinquencies are still well-contained.

New credit card delinquencies are rising despite low overall levels of credit card debt as a percentage of disposable income.

Stepping further out, the continued contraction of the money supply will begin to bite at growth, as intended by the Fed increasingly.

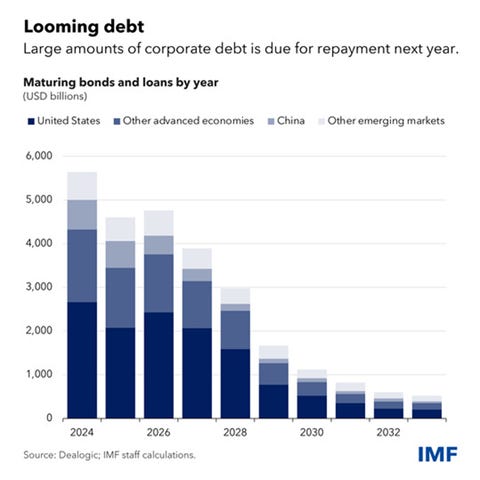

The IMF’s recent Global Financial Stability Report shows increasing shares of small and mid-sized firms in both advanced and emerging market economies with barely enough cash to pay their interest expenses. Defaults are on the rise in the leveraged loan market, where financially weaker firms borrow. These troubles are likely going to worsen in the coming year as more than $5.5 trillion of corporate debt comes due.

Articles by Macro Themes:

Medium-term Themes:

China’s Post-Pandemic Life:

Rare Revision: Policymakers are considering raising the budget deficit for 2023 by issuing at least 1 trillion yuan ($137 billion) in sovereign debt for infrastructure spending, an amount that would push the deficit to well above the 3% cap set in March. A rare mid-year revision to China’s national budget would put more of the fiscal burden on the central government and underscore President Xi Jinping’s desire to counter an economic slowdown while also highlighting growing concern among authorities that indebted local governments are running out of room to leverage up. So rare is the landmark proposal to revise the budget in the middle of the year that it’s only been done a handful of times during emergencies, such as in the aftermath of the 2008 earthquake in Sichuan province and the 1998 Asian Financial Crisis. - China Budget Revision Would Mark ‘Sea Change’ in Fiscal Strategy - Bloomberg

Underwhelming?: Chinese tourism noticeably rebounded during the nation’s eight-day Golden Week holiday, with around 826 million people traveling domestically. That amounts to a 4.1% increase from 2019 levels when accounting for the extra day, according to the government. That figure is rather underwhelming, given how high expectations were about China’s post-Covid reopening just a few months ago. Tourism spending was up only 1.5% from 2019’s Golden Week levels, meaning that each traveler actually spent less than before the pandemic. Retail sales at key firms increased only 9% YoY. Given the low base last year because of China’s strict pandemic restrictions, that doesn’t exactly amount to a bonanza. Consumers still seem reluctant to splurge. Restaurants were the bright spot, with revenue growing 20% YoY during the holiday. - China’s Golden Week Doesn’t Glitter – WSJ

Persistently Depressed: China’s former top builder warned in a stock exchange filing Tuesday that it will not be able to meet all of its future offshore payment obligations, including dollar bonds. Such non-payment may lead to relevant creditors demanding acceleration of payment or pursuing enforcement action, it added. With its peer China Evergrande Group facing a rising risk of liquidation amid uncertainties about its own restructuring, the developer’s deepening woes underscore the need for Beijing to adopt stronger measures to support a key growth engine as home sales keep slumping. Subdued home sales are further squeezing the breathing room of Chinese distressed developers like Country Garden despite the fact that the central government has rolled out a slew of measures, including an easing of mortgage restrictions at the end of August, which triggered a spurt of home sales in larger cities, to prop up the property market this year. - Country Garden Signals Default as China Property Woes Deepen - Bloomberg

Longer-term Themes:

Cyber Life and Digital Rights:

First Time: The EU has opened an investigation into X, formerly Twitter, over the way illegal content and disinformation of terrorist and violent content is spreading on its platform in the wake of the attacks by Hamas against Israel. EU officials have sent a series of questions that the social media platform must answer by next week. The formal probe, which is the first to be launched under the newly approved Digital Services Act, comes days after EU commissioner Thierry Breton wrote to billionaire Elon Musk raising concerns that the platform was “being used to disseminate illegal content and disinformation.” Failure to reply or a submission of incomplete or misleading information by X could lead to periodic penalties or fines amounting to up to 5 percent of the company’s daily global turnover. - EU opens probe into X over Israel-Hamas war misinformation – FT

Food: Security, Innovations, and Climate Change Implications:

Worse Before Better: Alaskan officials recently canceled the Bering Sea snow crab season for the second year in a row and the second time ever due to dwindling crab population levels. Only a few years ago, in 2018, the Bering Sea snow crab population was thriving. Then marine heat waves struck the region that year and again in 2019, contributing to low sea-ice cover. Snow crab numbers started to drop after that. Climate change and warming ocean waters likely played a role, although scientists are still figuring out the details. - Alaska Shuts Down Its Snow Crab Harvest for the Second Year in a Row – Bloomberg

Cold Places (Deep Sea, Artic, and Space Colonization):

Space Mining: A NASA spacecraft is finally on its way to a metallic main belt asteroid after a successful Falcon Heavy launch. Psyche is a Discovery-class planetary science mission whose destination is an object in the main asteroid belt also called Psyche. That asteroid is made primarily of metal and could be the core of a larger object whose outer layers were stripped away.The spacecraft will spend 26 months orbiting at Psyche in four different orbits, studying the largest solar system body made primarily of metal. “This will be our first time visiting a world that has a metal surface,” said Lindy Elkins-Tanton, Psyche principal investigator at Arizona State University, at a pre-launch briefing. - NASA launches Psyche mission to metal world - SpaceNews

Other Articles of Interest:

240 – Minutes: Texas Governor Abbott’s border-security crackdown is clogging up commercial crossings, leaving at least 19,000 trucks loaded with $1.9 billion of goods stuck waiting in Mexico. Texas announced a renewed push for cargo-truck inspections last month as part of Abbott’s “Operation Lone Star” plan to deter illegal border crossings and drug smuggling amid what he says is a lack of enforcement by the federal government. His administration did the same in April 2022, prompting protests from business interests on both sides of the border. The inspections were halted a week later after Texas officials said they’d reached security agreements with their Mexican state counterparts across the border. - ‘Absurd’ Inspections Halt 19,000 Trucks at Texas-Mexico Border - Bloomberg

Substitute for a Hike: Top central bank officials have signaled in recent days that they could be done raising short-term interest rates if long-term rates remain near their recent highs and inflation continues to cool. The Fed raises rates to combat inflation by slowing economic activity, and the main transmission mechanism is through financial markets. Higher borrowing costs lead to weaker investment and spending, a dynamic that is reinforced when higher rates also weigh on stocks and other asset prices. The upshot: If the run-up in the 10-year Treasury yields to their highest levels since 2007 persists, those increases could substitute for additional rises in the fed-funds rate. - Higher Bond Yields Likely to Extend Fed Rate Pause – WSJ

Podcasts and Videos:

For Fun:

VIEWS EXPRESSED IN "CONTENT" ON THIS WEBSITE OR POSTED IN SOCIAL MEDIA AND OTHER PLATFORMS (COLLECTIVELY, "CONTENT DISTRIBUTION OUTLETS") ARE MY OWN. THE POSTS ARE NOT DIRECTED TO ANY INVESTORS OR POTENTIAL INVESTORS, AND DO NOT CONSTITUTE AN OFFER TO SELL -- OR A SOLICITATION OF AN OFFER TO BUY -- ANY SECURITIES, AND MAY NOT BE USED OR RELIED UPON IN EVALUATING THE MERITS OF ANY INVESTMENT.

THE CONTENT SHOULD NOT BE CONSTRUED AS OR RELIED UPON IN ANY MANNER AS INVESTMENT, LEGAL, TAX, OR OTHER ADVICE. YOU SHOULD CONSULT YOUR OWN ADVISERS AS TO LEGAL, BUSINESS, TAX, AND OTHER RELATED MATTERS CONCERNING ANY INVESTMENT. ANY PROJECTIONS, ESTIMATES, FORECASTS, TARGETS, PROSPECTS AND/OR OPINIONS EXPRESSED IN THESE MATERIALS ARE SUBJECT TO CHANGE WITHOUT NOTICE AND MAY DIFFER OR BE CONTRARY TO OPINIONS EXPRESSED BY OTHERS. ANY CHARTS PROVIDED HERE ARE FOR INFORMATIONAL PURPOSES ONLY, AND SHOULD NOT BE RELIED UPON WHEN MAKING ANY INVESTMENT DECISION. CERTAIN INFORMATION CONTAINED IN HERE HAS BEEN OBTAINED FROM THIRD-PARTY SOURCES. WHILE TAKEN FROM SOURCES BELIEVED TO BE RELIABLE, I HAVE NOT INDEPENDENTLY VERIFIED SUCH INFORMATION AND MAKES NO REPRESENTATIONS ABOUT THE ENDURING ACCURACY OF THE INFORMATION