Blockbuster NFP Report Changes Growth Narrative, Supporting Risk Assets Despite Increasing the Likelihood of “Higher for Longer” Fed Policy Stance - Midday Macro – 10/6/2023

Color on Markets, Economy, Policy, and Geopolitics

Blockbuster NFP Report Changes Growth Narrative, Supporting Risk Assets Despite Increasing the Likelihood of “Higher for Longer” Fed Policy Stance

Midday Macro – 10/6/2023

Market’s Weekly Narrative and Headlines:

The weeks are long these days again. However, despite the choppy, somewhat hectic price action in equities this week, today’s post-jobs report rally left the S&P little changed on the week, a week that saw the VIX finally breach 20 for the first time since May. Growth was the clear winner thanks to Tech outperforming despite yields not materially falling, while small caps lagged their larger-sized brethren. Although initially seen as a negative, the blockbuster NFP beat was not accompanied by increased wage pressures and pushed back on growth worries. If everyone has a job, how can we have a hard landing? With Manufacturing and Service ISM moving closer to neutral earlier in the week, the former rising and latter falling, as well as in-line construction spending and better-than-expected factory orders, new economic readings on the week didn’t flash red. Add in a JOLTs report that showed more openings and little change in quits while the Challenger Job Cuts Report improved on the month, and labor markets continue to be resilient, as clearly seen in today’s jobs report. With almost every Fed official seemingly speaking this week, we heard concerns regarding tighter financial conditions from a once dove-turned-hawk while a very dovish voice chirped about only needing one rate cut next year if things stayed as projected. All in all, the Fed continues to be unsure if an additional hike is needed on the aggregate, but today’s data certainly increased the likelihood, although we push back on that personally (see below’s Deeper Dive sections). Oil is certainly indicating that global growth is in trouble, with rising inventories, reduced domestic gas demand, and the likelihood that notably more barrels may hit the market, driving WTI down to below $82 this week before rebounding ever so slightly. Copper echoed this sentiment as growth concerns regarding China, especially its property market, continued, although it joined the risk-on mode today and recovered some of its weekly losses. The aggs sector was mixed on the week as better harvests have helped drive prices lower for grains and beans more generally, while cattle fell from recent highs earlier in the week. The dollar ended the week little changed, with the $DXY moving above 107 mid-week only to fall back to 106 at the end of today despite yields remaining near recent highs. Things will get really interesting next week, given the slew of inflation data we receive, Treasury supply, FOMC minutes, and a slew of Fed speakers again.

Deeper Dive:

Today’s larger-than-expected payroll gains opens the door for a potential tactical relief rally in risk assets and Treasuries as growth fears subside while declines in energy costs already seen over the last week reduce headline and inflation expectation pressures. Next week’s inflation readings and how well Treasury supply is received will be the ultimate determinant of whether today’s positive price reversal has legs. We believe it will, and as a result, we used this morning's opening pullback, as well as hitting specific price targets throughout the week, to close our U.S. and Mexican equity short positions in our mock portfolio. We maintain our short position in the broader European FTSE index given our belief growth will continue to slow there while the ECB is not done raising rates, let alone close to easing policy. We also closed our long dollar position as we believe we are at peak rate differentials against major crosses and generally overbought, locking in a 7%+ gain in less than three months. With financial conditions tightening as much as they have in the last two weeks and energy prices falling notably, we see the probability that the Fed’s raises rates further in November as much lower despite today’s stronger jobs report. With the participation level remaining high, wage pressures not worsening, and multiple Fed officials noting they see a better alignment of supply and demand in the labor market, today’s NFP results will likely prove to be an anomaly, not a change in trend and hence not a reason for the Fed to tighten further. As we have highlighted in past writings, we still see numerous headwinds hitting growth in the coming quarters and are by no means calling for new all-time highs in equities. Neither do we believe that Treasuries are in the clear, but we do expect reduced “higher for longer” fears to allow some retracement in yield rises, and in our view, the recent bear curve steepener will turn into a bullish one. To be clear, the consumer continues to cool, showing an increasing amount of cracks, while business investment is falling, albeit unevenly, as the rolling recession (by different industries) backdrop experienced over the last year and a half continues. This leaves us wanting to be tactical and, like the Fed, data-dependent, leaning more towards a “bad is good” mantra as slower growth is ultimately needed to help the Fed end its current tightening cycle and allow risk assets to resume a more sustainable rally.

*Weaker equity markets, higher Treasury yields, wider credit spreads, and a stronger dollar have all tightened financial conditions dramatically in the last few weeks

*Quits tend to fall in the second half of the year due to seasonal factors, and this will pressure wages to continue to trend lower

*Although large banks continue to report healthy consumer activity, smaller financial institutions are increasingly seeing cracks in the consumer's strength

*The number of small business bankruptcies is trending higher than in recent years, with this week’s Challenger Job Cut showing business closures as the largest reason for layoffs in September

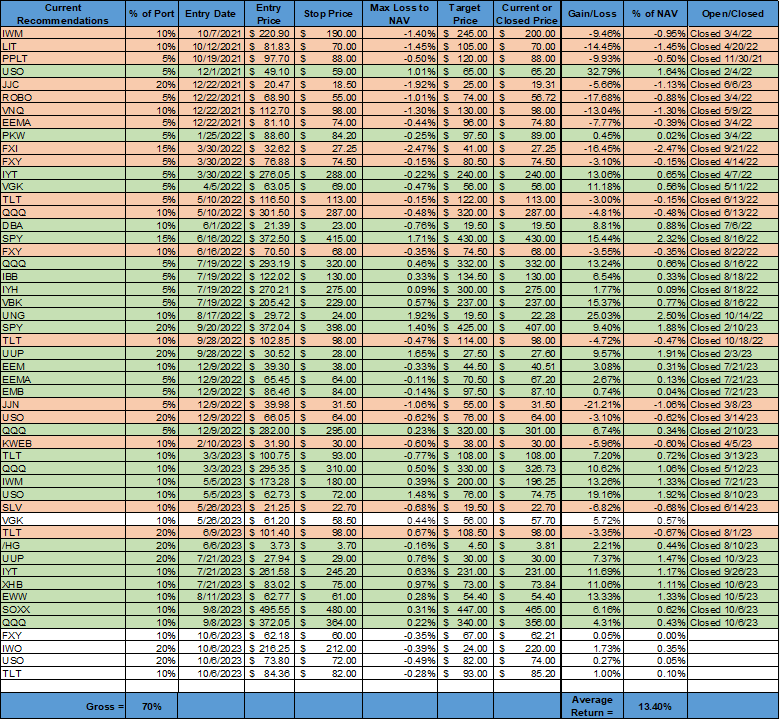

We are opening four new positions based on our change in views. Although each deserves a considerable explanation, something we hope to cover in the coming weeks, we want to give a quick overview and get them officially in the books. Again, due to the rapid and somewhat extreme price changes over the last weeks, these new additions look to capture a correction back to more normal levels, given the change in the macro narrative we see coming out of today’s payrolls report and expect to continue over the next few weeks. First, on the FX front, we believe that the Yen is oversold (shocker!) and that fundamentals will finally compel a change in policy by the BoJ that will end YCC. As a result, we are using the Invesco CurrencyShares Yen Trust ETF ($FXY) to open a 10% long position in the Yen, keeping a tight stop given a medium conviction level and the fact that we have got this wrong before. Second, we are opening a 20% long position in small-cap growth stocks through the iShares Russell 2000 Growth ETF ($IWO). Small caps are historically very cheap compared to large caps, having been hit the hardest by the recent pullback, so this is a tactical valuation correction play. Further, we believe that slowing (but not cliffing) growth coupled with a reduced inflationary pressured backdrop will support a tactical rebound in this size/factor combo as margins can expand more than forecasted, supporting a better earnings story. Third, we are opening a 20% long oil position through the $USO ETF. There is much to be said about oil, and we plan to cover it more extensively next week, but our central thesis is that despite recent drops in gasoline demand and the potential for greater supply next year, there is still a notable supply deficit until year-end and OPEC+ seems intent on keeping prices above $90. As a result, although the knife may still be falling, we are willing to take a stand at current levels. Finally, as highlighted above, we believe Treasuries are oversold on Fed “higher for longer” fears. We are starting a 10% long position in the iShares 20+ Year Treasury Bond ETF ($TLT). This may be premature given next week’s inflation data and Treasury auctions, but we see the 5% 30-year yield level as a good entry point. In summary, these new positions align with our view that a slowdown is upon us, but it is likely to still be shallow. At the same time, inflation continues to trend lower, and this will reduce how far and long the Fed needs to stay in restrictive territory. Effectively, markets will discount the duration/depth of the slowdown while increasing expectations the Fed will ease policy in Q2 of next year based on the “totality” of progress made. Ultimately, this may not be what occurs, but again, we are looking for this shift in the narrative to benefit our new positions tactically in the next few weeks.

*Rate differentials are unlikely to be able to stay at these levels for long, leading us to close our dollar-long bias and favor the Yen

*Things that are cheap can always get cheaper, but we believe a tactical bounce is warranted for small caps

*Gasoline demand dropped, and inventory levels rose recently, but we believe this will reverse and see supply deficits continuing, leading oil to recover recent loses

*Policy expectations are driving the selloff, and we expect that to change, with oversold conditions correcting

As always, thank you for reading, and please share our newsletter. Feel free to reach out with any questions or comments. - Michael Ball, CFA, FRM

Policy Talk:

There were numerous Fed speakers this week, with the majority mainly sticking to their hawkish or dovish tilts, although we saw some changes in posturing (both ways). Chair Powell spoke at a Fedlistens roundtable event in York, Pennsylvania, where the locals gave him an earful about the pains they were experiencing from higher inflation and now higher interest rates. He did not make any comments specific to policy or his outlook. Elsewhere, Richmond Fed President Barkin gave prepared remarks titled “The New Job Hierarchy” at an event sponsored by the Money Marketeers of NYU. He noted that the labor market was still key to determining where inflation would go, and they still seemed out of balance. As a result, he sees the range of potential outcomes as broad and, as a result, believes it may be necessary to raise rates further. Atlanta Fed President Bostic said he thinks rates will need to be held at “elevated levels for a long time” when speaking to reporters this week, as he does not see the need to raise but is also not in a hurry to cut rates, noting he expects only one rate cut at the end of 2024 as currently necessary. Bostic also posted an essay on the Atlanta Fed’s website, giving his outlook and concluding that reports from employers suggest the US labor market is poised to continue slowing. SF Fed President Daly sat for an interview hosted by the Economic Club of NY, where she suggested the recent tightening in financial conditions was equivalent to one 25 bp rate hike, doing a lot of work for the Fed and reducing the need for further hikes. She stressed that holding rates at current levels was an increasingly restrictive policy. Chicago Fed President spoke on Bloomberg’s Odd Lots podcast, acknowledging his “golden path” outlook was being increasingly challenged by the higher rates environment. He covered a lot of ground in the interview, and we recommend listening to the conversation, given his dovish tilt. We cover Clevland Fed President Mester and Governor Bowman in greater detail below, given their hawkish tilt.

Clevland Fed President Mester delivered a speech titled “A Timely Journey Back to Price Stability: Are We There Yet? No. Will We Get There? Yes” at the 50 Club of Clevland. She started with a recap of the last few years, noting how structural changes due to the pandemic created the current inflationary backdrop and the resulting response by the Fed to tighten policy. She sees tighter financial conditions beginning to moderate demand in the real economy while supply-side impairments have also improved notably. However, she still projects growth to be above trend and sees labor market conditions as strong, although she acknowledged some easing there. Mester highlighted that although wage pressures were subsiding, at 4% they remained well above the level consistent with the Fed’s 2% inflation target. She highlighted that progress was being made on the inflation front, especially when looking at it through a shorter time frame, but it remained too high, and the risks to the forecast remained skewed to the upside due to recent increases in energy costs. She concluded by worrying that inflation could become overly persistent if the Fed became complacent. With the economy on a “good path” and progress being made on inflation, Mester sees rates near their peak of the cycle, and the focus was now to ensure they stayed there long enough to return inflation to target.

“This overall performance suggests there is more underlying momentum in the economy than we thought even just three months ago. In fact, FOMC participants’ projections of economic growth this year were revised up at our recent meeting. Now, instead of projecting that growth will be well below trend this year, the median projection is that growth will be a bit over 2 percent, which is somewhat above trend.”

“Expected wage increases among our contacts have moved down, but at 4 percent, they remain higher than wage gains seen before the pandemic. In the nation, wage growth is still well above the level consistent with 2 percent inflation given current estimates of trend productivity growth.”

Governor Bowman gave remarks on the economy, monetary policy, and bank regulation at a banker's conference hosted by the Mississippi Bankers Association. She reiterated her belief that it would be appropriate for the Fed to raise rates further due to inflation remaining too high, highlighting recent rises in energy prices as increasing the risk that progress on inflation would be reversed. Bowman noted that the economy remained strong due to robust consumer spending and housing activity rebounding. She did acknowledge that labor market supply and demand “may” be coming into better balance. She discussed the “resilience” of the banking system and how lending standards were tightening and loan growth had slowed. However, she did not see a sharp contraction in credit that would slow the economy, noting that structural changes have reduced the effects of tighter monetary policy. She concluded her remarks by focusing on regulatory reform, where she saw the findings from the SVB and other bank failures as helpful but still limited in scope. She also pushed back on some of the upcoming reforms, hoping that policymakers would weigh the cost benefits they will have.

“Inflation continues to be too high, and I expect it will likely be appropriate for the Committee to raise rates further and hold them at a restrictive level for some time to return inflation to our 2 percent goal in a timely way.”

“I remain willing to support raising the federal funds rate at a future meeting if the incoming data indicates that progress on inflation has stalled or is too slow to bring inflation to 2 percent in a timely way.”

U.S. Economic Data:

Nonfarm payrolls increased by 336K in September, following an upwardly revised 227K in August and beating market forecasts of 170K. Job gains were largest in leisure and hospitality (96K), government (73K), and health care (41K). Employment showed little change in other major industries. The unemployment rate was unchanged at 3.8% in September, slightly above market expectations of 3.7%. The number of unemployed individuals was essentially unchanged at 6.36 million people. The U-6 unemployment rate fell slightly to 7% after touching a 15-month high of 7.1% in August. The labor force participation rate was also unchanged at 62.8%, the highest since February 2020. Average hourly earnings rose by 0.2% MoM, the same pace as in the prior month and slightly below market forecasts of a 0.3% MoM increase. The average workweek was unchanged at 34.4 hours in September, as forecast. In manufacturing, the average workweek was little changed at 40.1 hours, and overtime was unchanged at 3.1 hours.

Key Takeaways: September’s report showed the strongest job gains in eight months and was well above the 70K-100K needed per month to keep up with the growth in the working-age population, signaling that the labor market is not easing as quickly as the Fed would like and remains resilient despite the tightening campaign. The report changes the momentum picture in employment growth, moving the three-month average growth rate in payrolls to 266K. The household survey was weaker, with job growth of only 86K in September and a three-month average growth rate of 192K. Overall, payroll employment gains were broad-based, with the largest increase in leisure and hospitality, but government payrolls were also robust. Finally, over the past 12 months, average hourly earnings have increased by 4.2%, the least since June 2021, and below market estimates of a 4.3% rise, showing again that there is a detachment between job gains, average hourly earnings, and inflation overall.

*Gains were largest in Leisure and Hospitality and Government, although almost every industry grew

*The larger-than-expected rise in September’s payrolls stopped the downtrend in the three-month average

*The unemployment rate was unchanged in September at 3.8% versus the expectation of a drop to 3.7%

*Average hourly earnings in Sept posted its mildest monthly increase since Feb 2022 and its smallest year-over-year gain since June 2021

The number of job openings rose by 690K to 9.61 million in August, above the market consensus of 8.8 million. Job openings increased in professional and business services (+509K), finance and insurance (+96K), and state/local government education (+76K). Openings were higher across all regions, namely in the Northeast (+51K), the South (+278K), the Midwest (+238K), and the West (+124K). The job openings rate, which measures job openings level as a percentage of payrolls plus job openings, increased to 5.8% in August from 5.4% in July. The hires rate was unchanged at 3.7% and the layoffs rate held at 1.1%. The number of quits increased by 19K from the previous month to 3.638 million in August, rising from the revised two-and-a-half-year low of 3.619 million in the previous month. Quits rose in several sectors, including accommodation and food services (+88K), finance and insurance (+28K), and state and local government, excluding education (+21K). However, the number of quits decreased in the information sector (-30,000). The so-called quits rate, which measures voluntary job leavers as a share of total employment, was unchanged at 2.3%, remaining at its lowest level since January 2021.

Key Takeaways: The increase in openings moved the much-watched ratio of vacancies to unemployed higher to 1.5 compared to 1.4 last month. This compares to a peak of 2 in March 2022 but remains well above levels that will make Fed officials comfortable about the outlook for wage pressures. Although an important indicator of the excess demand for labor, the JOLTs data remains problematic. Most of the headline monthly increase in August came from an outsized move higher in professional and business services, mainly from small businesses, which saw a 6.5 standard deviation move higher than normal. This increase was not corresponded in other data series, such as the NFIB Survey. This is on top of a historically low sample size due to poor respondent participation and a general theme of ghost postings being reported. However, with that said, this report certainly was a step back in the recent labor market loosening narrative.

*The total number of openings moved higher due to an abnormally large jump in professional and business services

*The number of quits and layoffs was little changed in the month

*The vacancies to unemployed ratio is at 1.5, still well above the pre-pandemic level

New orders for manufactured goods increased by 1.2% MoM to $586.1 million in August, higher than the market expectations of a 0.2% MoM rise following a -2.1% decline in July. New orders for durable goods rose slightly by 0.1% MoM (vs. -5.6% in July), led by fabricated metal products, machinery, and electrical equipment. New orders for nondurable goods rose by 2.1% MoM, extending a 1.5% gain in July. Excluding transportation, factory orders increased by 1.4% MoM, the most since March 2022, following an upwardly revised 0.9% MoM increase in July. Excluding defense, orders rose 0.8% MoM after a -2.2% decline in the prior month. Total shipments increased by 1.3% MoM, after rising by 0.7% in July, while unfilled orders increased by 0.4% MoM following a 0.5% increase in July.

Key Takeaways: Factory orders in August beat expectations, with broader increases in sub-categories like electrical equipment, machinery, and motor vehicles outweighing notable declines in the volatile civilian aircraft industry. New orders for non-defense capital goods, excluding aircraft, which is a measure of business capex spending plans, increased by 0.9% MoM in August. This indicates that after a solid Q2, business spending on equipment also continued for the first two months of Q3. Shipments also picked up nicely, indicating activity in the manufacturing sector is still growing despite contracting PMI readings for some time now.

*August’s Factory Orders data was significantly stronger than expected thanks to broad increases, while transport equipment didn’t fall as much as feared

The Challenger Jobs Cut report showed firms announced plans to cut 47,457 jobs in September, below 75,151 in August. Employers announced 146.3K cuts in the third quarter, a 92% increase from 76.3K cuts announced in the same quarter last year. “Closing” was the largest reason cited by firms for their job cuts reasons, followed by no reason provided. Employers announced plans to add 590.4K jobs in September, up from the 380K announced a year earlier.

Key Takeaways: Despite the drop from August’s announced cuts, September’s total marks the eighth time this year when cuts were higher than the corresponding month a year earlier. So far this year, companies have planned 604.5 cuts, a 198% increase from the 209.5K cuts announced through September 2022.”Employers are grappling with inflation, rate increases, labor issues, and consumer demand as we enter Q4," Andrew Challenger, senior vice president of Challenger, Gray & Christmas, said. Technology is leading the annual cuts with 151K cuts, followed by retail (70.7K) and health care/products manufacturers (52.6K). The top reason for job cuts this year is due to market/economic conditions. So far this year, employers have announced 726.3K hiring plans, down 38% from the 1,163K plans recorded through September 2022, and the fewest year-to-date hiring plans since 2016 when 588.9K were announced through the third quarter.

*Market/Economic reasons and business closures are the leading reasons for job cuts this year

*Retail had 15K job cuts in Sept, leading cuts by industry

Construction spending increased by 0.5% MoM to $1,983.5 billion in August, after an upwardly revised 0.9% increase in July, in line with market forecasts. Private spending grew by 0.5% MoM, boosted by the residential segment increasing 0.6% MoM, supported by spending on single-family projects increasing by 1.7% MoM and multi-family rising by 0.6% MoM. Spending on the non-residential segment increased by 0.3% MoM. Public spending advanced by 0.6% in August, as growth in the non-residential segment increased by 0.6% MoM, offsetting declines in the residential decreased by -1.1% MoM. On an annual basis, construction spending is higher by 7.4%.

Key Takeaways: Total private construction continues to grind higher, with a broad rise in sub-categories. The largest contributor, private residential construction, continues to grind higher due to the large backlog of projects, especially in single-family units. However, private single-family is still lower by -10.6% YoY. Manufacturing construction also rose on the month again after falling earlier in the summer. Further, Highway and Street and Power continue to rise, reflecting a positive fiscal multiplier there from the infrastructure and IRA bills. There seems to be no notable reduction in construction activity due to tighter policy yet.

*Total Construction spending is higher by 4.2% YoY on a non-seasonally adjusted basis

The ISM Services PMI decreased to 53.6 in September from 54.5 in August, and in line with market expectations. Activity and demand readings were mixed, with Business Activity/Production (58.8 vs. 57.3) continuing to expand at a faster pace, while New Orders (51.8 vs. 57.5) dropped notably, closing in one more neutral reading. However, this decline was offset by a further expansion in New Export Orders (63.7 vs. 62.1) from an already strong level. The Backlog of Orders (48.6 vs. 41.8) also recovered to a significantly less contractionary reading. Supplier Deliveries (50.4 vs. 48.5) increased to a more neutral reading, while Inventories (54.2 vs. 57.7) and Inventory Sentiment (54.8 vs. 61.5) both fell as respondents felt their inventory levels were still too high given business activity. The reading on Employment (53.4 vs. 54.7) fell again after picking up notably in August, although respondents noted the “labor market remains very competitive.” Finally, Prices were unchanged at 58.9, with only four industries reporting price decreases.

Key Takeaways: September’s report suggests that the service sector expanded moderately slower than in August, primarily due to a slowdown in new order growth. Thirteen industries reported growth in September, while five noted a decrease in their overall readings. “The majority of respondents remain positive about business conditions; moreover, some respondents indicated concern about potential headwinds,” said Anthony Nieves, Chair of the Institute for Supply Management. Respondents reported decreases in restaurant traffic, with accommodation and food services being one of only three industries that saw lower business activity on the month and also reported lower new orders. Regarding inventories, comments from respondents indicated that “reduced business has necessitated lower inventory levels,” and firms were “more comfortable with the current supply chain situation and have begun lowering inventory levels.” Finally, respondents again noted trouble filling key positions as normal attrition occurred. Commodities up in price continued to include electrical equipment for the 32nd month in a row, while labor costs were up for 34th month in a row.

*The headline ISM PMI Service reading was little changed in September as declines in New Orders were offset elsewhere

*Employment readings fell but remained expansionary while Price readings were unchanged, stopping a recent bounce higher after a notable correction lower into summer

*At the sub-index level, the report was more mixed

*Selected comments skewed more positive

The ISM Manufacturing PMI increased to 49 in September from 47.6 in August, above market expectations of 47.8. Demand and activity measures improved on aggregate, with Production (52.5 vs. 50 in August) continuing to trend higher and back in expansionary territory, while New Orders (49.2 vs. 46.8) and New Export Orders (47.4 vs. 46.5) improved but remained in contractionary territory. The Backlog of Orders (42.4 vs. 44.1) contracted further after improving in the previous three months. Imports (48.2 vs. 48) were little changed, contracting for the eleventh month. Supplier Deliveries (46.4 vs. 48.6) shortened while Inventories (45.8 vs. 44) contracted at a slower pace but indicated firms continue to run tight inventory levels. Further Customers’ Inventories (47.1 vs. 48.7) readings fell further into contractionary territory. Employment (51.2 vs. 48.5) expanded after three months of contractionary readings, but respondents indicated greater hiring freezes and layoffs. Prices (43.8 vs. 48.4) fell notably, with 87% of panelists reporting the same or lower prices.

Key Takeaways: The overall headline reading was the highest since November 2022, reflecting the slowest contraction in the US manufacturing sector in ten months. “Companies are still managing outputs appropriately as order softness continues,” said Timothy Fiore, Chair of the ISM Survey Committee. Overall, the improvement in output/consumption drove most of the headline gains, while demand eased slightly and inputs continued to signal future demand growth was coming. “Demand remains soft, but production execution improved compared to August as panelists’ companies prepared for the fourth quarter and the close of the fiscal year. Suppliers continue to have capacity. 71% of manufacturing gross domestic product (GDP) contracted in September, up from 62% in August. More importantly, the share of sector GDP registering a composite PMI calculation at or below 45%, a good barometer of overall manufacturing weakness, was 6% in September, compared to 15% in August and 25% in July, a clear positive,” says Fiore. Regarding the decrease in prices, panelists’ comments indicate that buyers and suppliers continue “to aggressively negotiate price levels as commodity markets remain volatile.” Respondent comments were more mixed but generally skewed more upbeat, although the rolling slowdown/recession theme was apparent given the divergence in more negative views by a few industries. Finally, electrical/electronic components remained in short supply while industrial metals and ocean freight rates fell in price.

*The headline reading of 49 was the highest in almost a year, with much of the gain due to increases in production and employment

*New orders improved, although the backlog of orders contracted further, while employment rebounded back into expansionary territory

Technicals, Positioning, and Charts:

The Nasdaq is outperforming the S&P and Russell on the day. Factor and sector performance on the week changed frequently, as expected, with today's moves making growth the best-performing factor while small-caps were the worst on the week. Tech and Communication were the best-performing sectors on the week despite rising yields, helped by short covering and call buying following today’s NFP report. The majority of sectors did finish the week negative, with Energy being the worst-performing one due to the selloff in oil.

@Koyfin

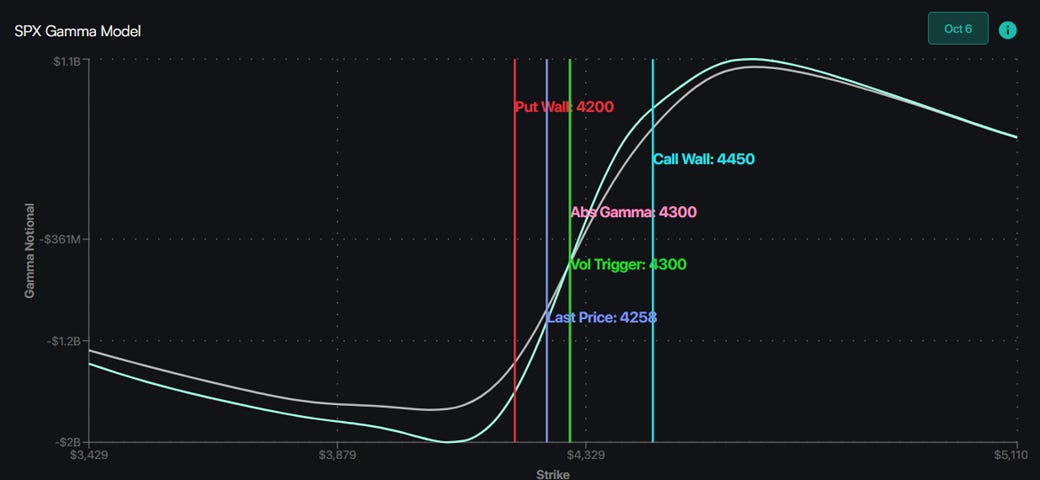

S&P optionality strike levels have the Zero-Gamma Level at 4330 while the Call Wall is 4450 and the Put Wall is 4200. The S&P went into payrolls in a more neutral place, allowing it to be a key catalyst for a short-term pivot higher once the 4300 area was recaptured. Going into today, the VIX premium to realized vol was high and traders were being forced to price in larger moves than were being delivered. This looks to have somewhat corrected today, with the move higher being larger than expected while the VIX corrected lower. If rates do fall, then IV will likely mean revert, and put buyers will “feel the burn.”

@spotgamma

S&P technical levels have support at 4348, then 4320, with resistance at 4380, then 4400. The longer-term October 2022 core bull market trend line, now currently in the low 4300 area, was recaptured today. Major resistance is now at the 4380 area from the downsloping blue trendline connecting June and August lows. The 4340 level still remains the key pivot area as it is the area where the summer melt up really started, and a close above this today means bulls have control.

@AdamMancini4

Treasuries are lower on the day, with the 10yr yield higher by 6 bps to 4.78%, while the 5s30s curve is unchanged on the session, sitting at 20 bps.

Four Key Macro House Charts:

Growth/Value Ratio: Growth is higher on the day and the week, with Large-Cap Growth the best-performing size/factor on the week.

Chinese Iron Ore Future Price: Iron Ore futures are lower on the day and the week.

5yr-30yr Treasury Spread: The curve is steeper on the week.

EUR/JPY FX Cross: The Euro is stronger on the day and the week.

Other Charts:

In recent years, when the proportion of S&P 500 stocks trading above their 50-day moving average dipped below 10%, we usually got a quick bounce.

Call volumes have fallen drastically, although that is likely to change after today’s rally.

More companies have issued Q3 guidance, with negative guidance dominating in most sectors.

It is not just the U.S. Government yields are higher everywhere.

The rise has been unparalleled, with global median 10-year real rates rising around 10% in two years.

The modeled term premium for the U.S. 10-year Treasury is now safely positive.

Solid economic growth and sticky inflation/elevated interest rates could benefit cyclical value stocks. Could we see a rotation? According to Stifel, a higher for longer Fed, better economic growth, and sticky inflation would favor cyclical value stocks.

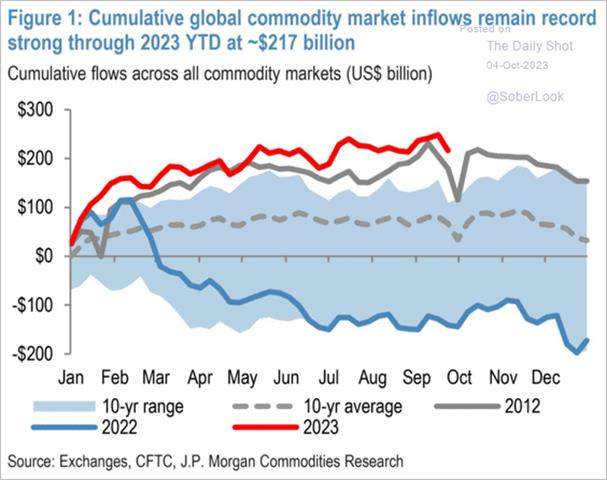

Commodity market inflows remain robust.

Articles by Macro Themes:

Medium-term Themes:

China’s Post-Pandemic Life:

Groundwork: The US and China are moving closer to setting up a meeting between Presidents Joe Biden and Xi Jinping at next month’s APEC summit in San Francisco. But Xi, who skipped last month’s Group of 20 summit in India and whose government has expressed frustration with recent comments by the American president, has not yet committed to the meeting. A summit between the two leaders would be the first time they have spoken since they met during the G-20 Summit in Bali, Indonesia, last November and follows months of deteriorating relations between Washington and Beijing. Under normal circumstances, a one-on-one meeting between the two leaders on the sidelines of a major gathering like the Asia-Pacific Economic Cooperation summit would be routine — even obligatory. The fact that China hasn’t committed to it even now underscores the fragility of the efforts to ease tension. - Biden, Xi Meeting Becomes More Likely, Though Not Definite - Bloomberg

Longer-term Themes:

A.I. All Day:

Going on Inside: As companies race to commercialize AI, the so-called “guardrails” that prevent these systems from going awry, such as generating toxic speech and misinformation or helping commit crimes — are struggling to evolve in tandem, according to AI leaders and researchers. In response, leading companies including Anthropic and Google DeepMind are creating “AI constitutions” — a set of values and principles that their models can adhere to, in an effort to prevent abuses. The goal is for AI to learn from these fundamental principles and keep itself in check without extensive human intervention. However, in a response to clean up the responses generated by AI, companies have largely relied on a method known as reinforcement learning by human feedback (RLHF), which is a way to learn from human preferences. - Broken ‘guardrails’ for AI systems lead to push for new safety measures - FT

Energy’s Midlife Crisis:

Thermal Loop: Thirteen US states are now implementing underground thermal energy networks to reduce buildings’ carbon emissions as part of a nationwide push to adopt cleaner energy sources. Thermal energy networks use pipe loops that connect multiple buildings and provide heating and cooling through water-source heat pumps. Geothermal heat is commonly used in these networks, but it is also possible to bring in waste heat from other buildings through the sewer system. When installed, these networks can provide efficient, fossil fuel-free heating and cooling to commercial and residential buildings. Thanks to legislative backing and widespread support from utility companies and labor unions, they’re likely to become an increasingly significant part of the future energy mix in the US. - Underground thermal energy networks are becoming crucial to the US’s energy future – MIT Tech Review

Authoritarianism in Trouble?:

Fact-Checking: After President Biden won the election nearly three years ago, three of every 10 Americans believed the false narrative that his victory resulted from fraud, a poll found. In the years since, fact-checkers have debunked the claim in lengthy articles and corrections posted on viral content, videos, and chat rooms. This summer, they received a verdict on their efforts in an updated poll from Monmouth University: Very little has changed. Three of every 10 Americans still believed the false narrative. With a wave of elections expected next year in dozens of countries, the global fact-checking community is taking stock of its efforts over a few intense years — and many don’t love what they see. - Fact Checkers Take Stock of Their Efforts: ‘It’s Not Getting Better’ - NYT

Lev and Igor: In recent years, a number of countries—China and Russia, in particular—have found ways to take the kind of corruption that was previously a mere feature of their own political systems and transform it into a weapon on the global stage. Countries have done this before, but never on the scale seen today. This is now also occurring in Western nations with an exponential increase in the scale of U.S. commerce involving foreign interest groups. Americans with connections to decision-makers now enjoy opportunities that can lead to all sorts of corrupt behavior. Political consultants and former U.S. officials who spend time in the large, lucrative, and lightly regulated marketplace of influence peddling face frequent tests of their ethics, integrity, and patriotism. Trump’s impeachment regarding his pressure on Ukraine to deliver dirt on Biden was a prime example of this type of corruption, and the article goes into detail on how that transpired. - The Rise of Strategic Corruption – Foreign Affairs

ESG versus the World:

Subpoena: Republican politicians over the past year have attacked Wall Street’s environmental, social, and governance financing strategies, saying that money managers are promoting liberal goals such as climate change at the expense of the fossil fuel industry. At least three state attorneys general sent formal demands to Wall Street money managers asking for information about their climate work as GOP officials step up attacks on ESG investing. The attorneys general asked money managers for their communications with Climate Action 100+ and the Net Zero Asset Managers initiative, which is part of the Glasgow Financial Alliance for Net Zero. The AGs are also seeking information about how the asset managers vote on climate-related shareholder resolutions, the people said. - Money Managers Get State AG Subpoenas Related to Climate Work - Bloomberg

Asian Tigers 2.0:

Slower Growth: The World Bank has cut its forecast for China’s growth next year and warned that East Asia’s developing economies are set to expand at one of the lowest rates in five decades, as US protectionism and rising levels of debt pose an economic drag. The projections show that the region, one of the world’s main growth engines, is set for its slowest pace of growth since the late 1960s, excluding extraordinary events such as the coronavirus pandemic, the Asian financial crisis, and the global oil shock in the 1970s. Economists expected China’s rebound from strict pandemic controls would be “more sustained and more significant than it turned out to be”, said Aaditya Mattoo, World Bank chief economist for East Asia and the Pacific. - Asia faces one of worst economic outlooks in half a century, World Bank warns - FT

Cold Places (Deep Sea, Artic, and Space Colonization):

Thawing: Faced with economic isolation over its invasion of Ukraine, Russia is turning to China for help developing the Arctic as Western energy companies are trying to pull out of Russian projects. The newfound cooperation is most evident in surging shipments of crude through the Northern Sea Route, which traverses the Arctic from northwestern Russia to the Bering Strait. The volume, while still small compared with what is carried via southern routes, has shot up in recent weeks. Russia asserts the right to regulate transit on the route. Further, Russia has joined with China in naval exercises and maritime security arrangements in the far north and looked to it for aid in technology, such as satellite data to monitor ice conditions. - China Is Gaining Long-Coveted Role in Arctic, as Russia Yields - WSJ

Other Articles of Interest:

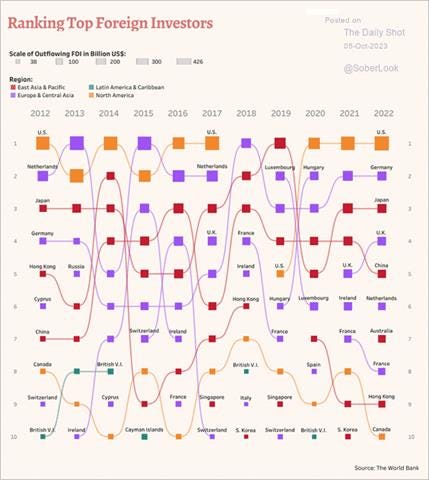

Ranking FDI: One of the most significant phenomena in 21st-century globalization, driven by the ascent of multinational corporations and the removal of investing barriers, is the vast cross-border flow of foreign capital. To analyze recent trends, Samidha Nayak utilized World Bank data spanning 2012–2022, charting the top 10 destinations for foreign direct investment (FDI) and the leading investing countries annually. The U.S. and China retained their top spots, but the difference grew much larger, with the U.S. attracting nearly 50% more foreign investment ($388 billion) than China ($180 billion). Singapore, which first appeared in the rankings in 2014, took third place with $141 billion. Meanwhile the bottom half changed almost entirely, with France, Canada, Sweden, and India replacing Cyprus, Germany, the British Virgin Islands, and Ireland. - Ranked: Top Countries for Foreign Direct Investment Flows – Visual Capitalist

Podcasts and Videos:

The Fed’s Tom Barkin On the Impact of Higher Interest Rates – Odd Lots Bloomberg

China Dominates the Global Lithium Industry. Can the U.S. Ever Catch Up? – WSJ Videos

VIEWS EXPRESSED IN "CONTENT" ON THIS WEBSITE OR POSTED IN SOCIAL MEDIA AND OTHER PLATFORMS (COLLECTIVELY, "CONTENT DISTRIBUTION OUTLETS") ARE MY OWN. THE POSTS ARE NOT DIRECTED TO ANY INVESTORS OR POTENTIAL INVESTORS, AND DO NOT CONSTITUTE AN OFFER TO SELL -- OR A SOLICITATION OF AN OFFER TO BUY -- ANY SECURITIES, AND MAY NOT BE USED OR RELIED UPON IN EVALUATING THE MERITS OF ANY INVESTMENT.

THE CONTENT SHOULD NOT BE CONSTRUED AS OR RELIED UPON IN ANY MANNER AS INVESTMENT, LEGAL, TAX, OR OTHER ADVICE. YOU SHOULD CONSULT YOUR OWN ADVISERS AS TO LEGAL, BUSINESS, TAX, AND OTHER RELATED MATTERS CONCERNING ANY INVESTMENT. ANY PROJECTIONS, ESTIMATES, FORECASTS, TARGETS, PROSPECTS AND/OR OPINIONS EXPRESSED IN THESE MATERIALS ARE SUBJECT TO CHANGE WITHOUT NOTICE AND MAY DIFFER OR BE CONTRARY TO OPINIONS EXPRESSED BY OTHERS. ANY CHARTS PROVIDED HERE ARE FOR INFORMATIONAL PURPOSES ONLY, AND SHOULD NOT BE RELIED UPON WHEN MAKING ANY INVESTMENT DECISION. CERTAIN INFORMATION CONTAINED IN HERE HAS BEEN OBTAINED FROM THIRD-PARTY SOURCES. WHILE TAKEN FROM SOURCES BELIEVED TO BE RELIABLE, I HAVE NOT INDEPENDENTLY VERIFIED SUCH INFORMATION AND MAKES NO REPRESENTATIONS ABOUT THE ENDURING ACCURACY OF THE INFORMATION