Time for the Push Back: Inflation Isn’t Beat, and the Fed Can Be Patient – Midday Macro – 12/8/2023

Color on Markets, Economy, Policy, and Geopolitics

Time for the Push Back: Inflation Isn’t Beat, and the Fed Can Be Patient

Midday Macro – 12/8/2023

Market’s Weekly Narrative and Headlines:

Major stock indexes are higher this week thanks to a post-jobs report Friday rally. Growth and Tech outperformed as AMD’s earnings report reinvigorated “AI” animal spirits, although the small-caps value combo was the best-performing size/factor on the week. The VIX is near its post-pandemic lows following a better headline beat in nonfarm payrolls and a drop in the UER, keeping the soft-landing narrative alive and well. Lower inflation expectations and a jump in consumer confidence, mainly driven by Republican-leaning respondents who are happier due to recent presidential polls, better aligned the University of Michigan’s report with realities at the gas pump and in the job market. The data was more mixed earlier in the week, with factory orders falling more than expected, although at its core, they were less alarming. At the same time, the ISM service PMI rose on stronger production and inventory activity, while changes in employment and prices were stable. The JOLTs report showed America had fewer job openings than expected while turnover was slowing. The Challenger Jobs Cut report also indicated a further loosening in labor markets, rising from October’s level. Finally, consumer credit grew less than expected in October, with credit card usage slowing. With the Fed in a blackout period due to next week’s December FOMC meeting, the flurry of new economic data, especially regarding labor market conditions, left Treasury yields higher, more so in the front end, on the week, mainly due to today’s sell-off, and flattened the curve.

Oil is ending the week lower, although today’s rally moved WTI above $70 again. Weaker U.S. gas demand, continued increasing production levels, growing inventories due to export impairments, and mixed views on global demand are outweighing OPEC+ cuts and leaving short speculators in charge. Copper was also lower on the week but fared better, moving out of its longer-term downtrend on continued hope that China would turn to more FAI-driven stimulus initiatives and stabilize financing to the property sector. This was more clearly seen in iron ore prices, which are at highs for the year. Finally, the dollar was higher on the week, mainly due to broad weakness outside of the Yen, which rallied off comments from the BoJ that the era of negative rates may actually end.

Deeper Dive:

The recent rally in both stocks and bonds has been predicated on a belief that the Fed will be able to ease policy sooner and more quickly due to disinflationary progress. At the same time, as seen again today with the stronger-than-expected jobs report, the soft-landing narrative is alive and well. We are increasingly questioning both of these views. We continue to believe that inflation isn’t beaten and will fall in a rolling fashion, not a linear path. The progress made in October was exceptional and suspicious in many regards, and we believe November’s CPI report will contain a notable level of payback. Business surveys have largely shown a stabilization in price readings. However, they still remain broadly expansionary. Energy price decreases continue, and supply-chain readings show reduced cost-push pressures. However, as the Fed has noted (and somewthing we have changed our view on), the “final mile” of disinflation needed to drop readings to the Fed’s target will require a multi-quarter period of below-trend growth. We are now entering that period, as seen in Q4 GDPNow readings of 1.2% (versus 2% being the trend), but given the pick up in consumer expenditures we saw in November following a weaker October, pricing power, especially in the service sector, is still too strong. Eventually, firms will increasingly shift strategy to cut prices to gain market share, something currently occurring in the goods sector, but expectations for a still resilient consumer during the holiday season are postponing that for services. As a result, the Fed still sees an economy that is cooling but not by enough to rebalance supply and demand to a non-inflation-accelerating level. This will force the Fed to push back on market expectations, likely through more forcefully hawkish comments and the SEPs at the December FOMC meeting next week. As a result, we want to push back on the current rally in stocks and bonds and see a further reversal in the recent broader dollar weakness that occurred in November. We opened short positions in the S&P ($SPY) and went long the $DXY dollar index ($UUP) yesterday. It was initially our intention to do this after year-end, given strong seasonals. However, we believe results from the November CPI report and December FOMC meeting will end the Santa rally early this year, especially given the magnitude of the gains seen in November.

*Disinflationary progress and continued QT have only made the stance of policy tighter

*Whether it is leading economic indicators, confidence readings, or the yield curve, a lot of historically strong recessionary indicators would have to be wrong for this time to be different

*Expectations are for spending to be weighed on by weaker real disposable income gains, weighing on 2024 growth, although forecasts highly vary

*Can financial conditions loosen any further, and even if they do, will they offset tighter credit conditions?

*The majority of declines in nominal yields have been from lower real rates, but if inflation firms, as we expect, this is unlikely to continue

We also see oil as oversold and started a long position there yesterday through the $USO ETF. Our more negative view on U.S. growth and less certainty around overall global demand gives us less conviction here, which is why it is a smaller position in the portfolio. However, we see speculators as overly bearish and positioning as now offsides with fundamentals. Yes, oil should not be $90, but given OPEC+ intentions to protect prices and the overly bearish views on U.S. demand despite indications the consumer is still actively spending and traveling elsewhere, we see this as a tactical opportunity to catch oil at the bottom of what we expect to be rangebound price action moving forward for some time. On the margin, we will be watching for improvements in the Panama Canal, Chinese refinery runs, and adherence to cuts by Russia to give us confidence that the bottom is in for WTI. We also believe that domestic gasoline demand will normalize over the year-end holiday period after what was a weaker Thanksgiving week. Finally, geopolitical tensions remain high, and the risk premium given to current prices is not representative of some of the negative developments we have recently seen. There is always more to say regarding oil, and we hope to do an oil-specific Deeper Dive soon.

*Net speculative oil positioning is near Covid lows, while fundamentals indicate a supply deficit in Q1 ‘24

*Gasoline demand has been seen as weaker than past average levels, while inventories are healthy

*Overall U.S. crude inventories are withing normal levels, but higher production and impaired export channels are leaving the Gulf flooded with barrels. Will this last?

We continue to want to be long the Japanese Yen despite a renewed stronger dollar bias. It does finally seem that the BoJ is getting ready to normalize policy. The relinquishment of yield curve control in October indicates an intention to leave behind negative rates. This also means a reduction in QE and the support that policy has given to domestic bonds and equities. As a result, we want to be short Japanese equities but hedged from what we expect will be an appreciating Yen, using the WisdomTree Japan Hedged Equity Fund ETF ($DXJ). We plan to write more about Japan in the coming weeks but wanted to enter the short equity position given how fast things seem to be moving in markets there.

*Markets are waking up to the fact that the BoJ may finally be serious about exiting its negative rate policy

*Positoning in Japanese equities by foreigners looks to be very long and a change in BoJ policy posturing may cause an exit

*Japanese firms are increasingly divesting from cross-shareholdings, changing the fundamental equity landscape, but will this positive structural development overcome macro headwinds?

Finally, we are starting a short position on Argentina equities through the Global X MSCI Argentina ETF ($ARGT). We believe Milie, like so many before him, although talking a good game, will be unable to enact the necessary reforms needed to give investors confidence that Argentina has brighter days ahead. He is already aligning himself closer to the Peronist Party and hiring mainstream figures, something Macri did and led to his progressive agenda becoming sabotaged from within. He is also walking back his promises to cut social spending as powerful labor unions and working-class interests line up against him. Milie will also be governing without a majority in Congress, and his moderation indicates that he knows he will need to build a coalition if he wants to make progress on his domestic policy promises. In our opinion, this means little will actually get done as the political corruption is deeply ingrained and will fight to remain. The bottom line is that Milei’s surprise victory was due to the dire economic situation Argentina is in, with growing levels of poverty and historically high inflation, even for there. We see the post-election sugar high wearing off soon and the weight of poor fundamentals weighing on risk assets there again relatively quickly.

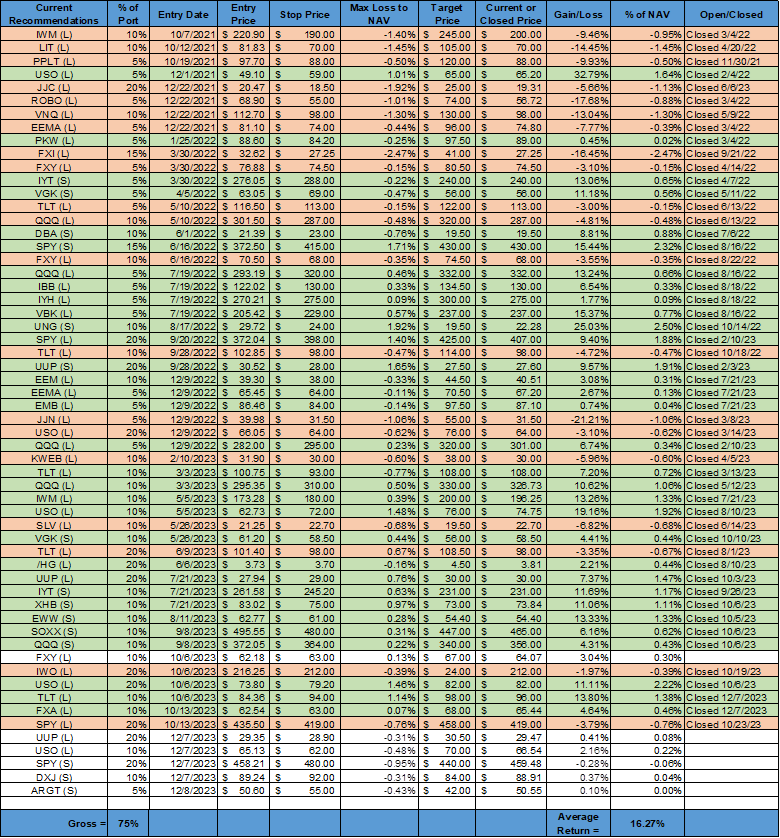

*We closed our long $TLT and $FXA positions and moved higher our stop for $FXY to lock in gains. Additionally, we added longs in $UUP (20%) and $USO (10%) and shorts in $SPY (20%), $DXJ (10%), and $ARGT (5%). The additive cumulative risk-adjusted additive gains for the portfolio moved to 16.27% on the week

As always, thank you for reading, and please share our newsletter. Please feel free to reach out with any questions or comments. – Michael Ball, CFA, FRM

Policy Talk:

Consumer credit increased at a seasonal-adjusted annual rate of 1.2% in October, or by $5.2 billion on the month, to $4,989.9 billion. Revolving credit increased at an annual SAR rate of 2.7%, or by $2.8 billion on the month, to $1,295.4, while nonrevolving credit increased at an annual SAR rate of 0.7%, or by $2.2 billion, to $3,694.4. The most recent readings (August) of interest rate levels for car loans is 7.88%, and credit cards are 21.19%.

*Consumer credit grew by a smaller-than-expected amount due to lower use of revolving credit

*In real terms, revolving credit, or credit card debt, is only back at pre-pandemic levels

*Consumers still have a credit card debt to disposable personal income ratio that is below pre-pandimc levels

U.S. Economic Data:

Nonfarm payroll employment increased by 199K in November, surpassing the 150,000 added in October and exceeding market expectations of a 180,000 gain. Gains were driven by increases in health care (77K) and government (49K), mainly due to increases in local government (+32K) and state government (+17K). Employment in manufacturing rose by 28K, slightly less than expected, as automobile workers returned to work following the resolution of the UAW strike. In contrast, retail trade employment declined by -38K. The unemployment rate fell to 3.7% in November from 3.9% in the previous month, the lowest since July, and firmly under market expectations that it would remain unchanged at 3.9%. The U-6 unemployment rate fell to 7%, down from a near two-year high of 7.2% in October. The number of long-term unemployed edged lower to 1.2 million. The employment-population ratio increased by 0.3 percentage points to 60.5% in November. The labor force participation rate changed little, at 62.8%, and has been essentially flat since August. Average hourly earnings rose by 0.4% in November, after a 0.2% increase in the prior month and above the market forecast of a 0.3% gain. Over the past year, average hourly earnings have increased by 4%, the same pace as in the prior month, and matching market estimates. Finally, the average workweek edged up by 0.1 hour to 34.4 hours in November, a tad below market forecasts of 34.3 hours.

Key Takeaways: Although the November payroll report was stronger than expected, it was not due to broad gains. November’s report included 47K workers returning from strikes, an increase of 49K government jobs, and a further 77K jobs added in health care. Excluding those non-cyclical sectors, the economy added only 26K jobs, which adds to the evidence that job growth is slowing. Further, private payroll gains have averaged 145K per month over the last three months, but excluding healthcare and leisure, the increase is only 7K. On the other side, the 0.4% MoM gain in real wages marks the strongest increase in four months. The decline in the UER to 3.7% backs the labor market away from triggering the Sahm Rule, a reliable recession indicator that would have been triggered at 4.0%. However, the sharper-than-expected decline in job openings lowered the ratio of vacancies to unemployment to 1.39 in November from 1.44 in October, indicating a loosening in labor markets. These readings feed into the narrative that the Fed still faces an inflation-accelerating wage growth level while the economy is increasingly slowing. As a result, cutting rates will still have to wait, especially if October's CPI progress reverses in November.

*Payrolls rose by 199K in November, near its three-month average

*The unemployment rate declined to 3.7%, alleviating worries that a recession was imminent

*The percent of unemployed for more than 27 weeks moved to 18.3%, down from 19.8% in prior month

*The participation rate continues to trend higher, something the Fed has watched closely

*Average hourly earnings rose by 0.4% in November, moving to the high end of its recent monthly change range, after only rising 0.2% in October

*The Fed Labor Market Spider Graph continues to indicate a broad loosening, now approaching or below prepandemic levels for many readings

*After a brief pause in October, employment at temp agencies resumed its gradual decline in November

The number of job openings decreased by -617 from the previous month to 8.73 million in October, marking the lowest level since March 2021 and falling below the market consensus of 9.3 million. During the month, job openings decreased in health care and social assistance (-236K), finance and insurance (-168K), and real estate and rental and leasing (-49K). On the other hand, job openings increased in information (+39K). Regarding regional distribution, job openings fell in the South (-289K), the Midwest (-193K), the West (-83K), and the Northeast (-52K). The number of total separations increased slightly to 5.65 million from 5.6 million. The number of quits declined to 3.63 million in October, down from September's revised figure of 3.65 million and moving closer to a two-and-a-half-year low reached in July. The incidence of quitting increased in the leisure and hospitality (-63K) and trade, transportation, and utilities (-48K). The number of layoffs changed little, increasing by 30K to 1.64 million. The quits rate, a metric that measures voluntary job leavers as a proportion of total employment, held steady at 2.3% for the fourth consecutive month. This rate remained at its lowest level since January 2021.

Key Takeaways: Job openings in the U.S. decreased in October to the lowest level since early 2021, underscoring the gradual cooling in the labor markets that the Fed wants to see. The figure was below sell-side economic forecasts, with the declines being broad-based across sectors. The report showed layoffs remained historically low, and hiring eased somewhat. The ratio of openings to unemployed people slid to 1.3, the lowest since mid-2021. While still somewhat indicative of a tight labor market, the figure has eased substantially over the past year from its peak of two-to-one in 2022.

*Job openings continue to trend lower due to broader-based decreases across most industries

*Financial activities and education and health service sectors saw the largest declines in openings

*Both quits and layoffs were little changed on the month

*Job openings and quits to unemployment are both trending lower, indicating a loosening in labor markets

*Retail trade continues to see a large reduction in openings while Professional and Business Services are trending higher

U.S. employers announced plans to cut 45,510 jobs in November, 24% higher than 36,836 cuts in October and 41% lower than the cuts announced in November last year. The retail sector announced the most cuts (6,548), followed by tech (5,049), financial (3,698), transportation (3,515), and health care/products (3,329). In November, employers announced plans to hire 15.6K workers, for a total of 775.5K year-to-date.

Key Takeaways: So far this year, companies have announced plans to cut 686.8K jobs, a 115% increase from the 320.1K cuts announced in the same period last year. It is the highest January-November total since 2020, when 2,227.7K cuts were recorded. Prior to 2020, it was the highest year-to-date total since 1,242.9K cuts were announced through November 2009. Market/Economic Conditions continue to be the main reasons for cuts, followed by no reason provided and closings. As of November, firms have the lowest year-to-date total for announced hiring plans since 2015, when 679.3K hiring plans were recorded through November. Through November, seasonal employers have announced 573,.3K hires, the lowest total since 518K seasonal hiring plans were announced in 2013. “The job market is loosening, and employers are not as quick to hire. The labor market appears to be stabilizing with a more normal churn, though we expect to continue to see layoffs going into the New Year,” said Andrew Challenger, labor expert and Senior Vice President of Challenger, Gray & Christmas, Inc.

*There was an uptick in cuts in November as employers continue to have less appetite for expanding their workforce

*Technology sector leads all industries this year with 163,562 cuts, 5,049 of which occurred in November

The ISM Services PMI increased to 52.7 in November from 51.8 in October, beating forecasts of 52. Demand and activity measures were mixed. Business Activity (55.1 vs. 54.1) expanded at a faster rate, with eleven out of fifteen industries reporting growth. New Orders (55.5) were unchanged and expansionary, as were New Export Orders (53.6 vs. 48.8), while the Backlog of Orders (49.1 vs. 50.9) contracted slightly. Supplier Deliveries (49.6 vs. 47.5) moved close to neutral as supply chain constraints continued to improve. Imports (53.7 vs. 60) fell notably but remained expansionary. Inventories (55.4 vs. 49.5) expanded as respondents noted a desire to build for holiday demand, while Inventory Sentiment (62.2 vs. 54.4) jumped, indicating that although building inventories, firms are worried they have too much stock. Employment (50.7 vs. 50.2) remained near neutral. However, comments indicated continued difficulty in staffing. Finally, Prices (58.3 vs 58.6) fell slightly, with only three industries reporting a decrease in prices.

Key Takeaways: Improvements in inventory readings and production drove the headline PMI index higher, as there were fewer changes at the sub-index level elsewhere. Fifteen industries reported growth in November, indicating sustained growth for the service sector at a slightly faster pace. Information, Mining, and Professional Scientific & Tech Services were the three industries that reported a decline in growth. "Respondents’ comments vary by both company and industry. There is continuing concern about inflation, interest rates, and geopolitical events. Rising labor costs and labor constraints remain employment-related challenges”, Anthony Nieves, Chair of the ISM Services Business Survey Committee, said. “It’s not getting worse overall, but it seems to keep moving sideways,” he said. “Some industries are struggling to backfill positions, typically with customer-facing roles. Construction is another industry having difficulty. Still, others are looking to control that variable expense, with business levels not as high to withstand carrying a large roster of employees. So, it remains a mixed bag.” There looks to be a continual mending of supply chains. One respondent noted that “due to supply chain improvement, backlogs are under control” and “suppliers are making good progress clearing up back orders.” Supplier delivery times' average reading in the last ten months reflects the fastest delivery times since June 2009.

*The services sector had a slight uptick in growth in November, attributed to the increase in business activity and slight employment growth

*Sub-index readings and comments were more mixed, with various industries experiencing different levels of growth

Factory orders declined by 3.6% in October, following a downwardly revised 2.3% rise in September, worse than market forecasts of a -2.8% fall. Orders for transportation equipment declined by -14.7%, due to a large decline in nondefense aircraft and parts (-49.6% MoM). Excluding transportation, factory orders declined by -1.2% MoM (vs. 0.4 MoM in Sept), and excluding defense, orders declined by -4.2% MoM (vs. 2.7% MoM). Nondefense (core) capital goods excluding aircraft fell by a more modest -0.3% MoM (vs. -0.2% MoM) while consumer goods declined by a greater -3.1% MoM (vs. 0% MoM) rate. Orders declined for electrical equipment, appliances, and components (-1.1% MoM vs. -0.8 MoM in Sept), machinery (-0.3% vs. 0%), and primary metals (-0.3% vs. 0). In contrast, orders rose for fabricated metal products (0.4% vs. 0.9%) and computers and electronic products (0.3% vs. 0.8%). Shipments fell -1.4% on the month after a flat reading in September, with durable goods lower by -0.8% MoM and nondurables lower by -1.9% MoM. Unfilled orders rose by 0.3% MoM, following a 1.3% increase in the prior month. Total inventories were little changed for a second month in a row. With inventories edging higher and shipments falling, the inventories-to-shipments ratio rose to 1.48 in October from 1.46 in September.

Key Takeaways: The headline decline in new orders in October was the biggest monthly drop since April 2020, when orders at factories fell by -13.5% due to the spread of coronavirus lockdowns. Additionally, the October report revised September's numbers downward, such that the orders for nondefense capital goods excluding aircraft now indicated that business spending in September was not as strong as initially thought. However, when excluding aircraft and defense, capital goods orders were more stable while consumer goods fell by a greater amount, although this series is often volatile. There was a notable bounce back in mining and oil field machinery new orders after a drop in September. Interestingly, new orders for furniture were again up, rising by 1% in October following a 1.2% increase in the prior month. With shipments also negative, but positive fore core capital goods, and unfilled orders and inventories positive for a third month, the report was not as troubling as the headline declien would indicate.

*The sharp pullback in factory orders partly reflected a 5.4% decline in durable goods orders in October following a 4% increase in September

*There was a large decrease in new orders for transportation equipment, an often volatile category

*Demand for auto and parts is still weak given the effects of the UAW strike

The University of Michigan's consumer sentiment increased to 69.4 in December, rising from 61.3 in the previous month and surpassing market expectations set at 62.0, a preliminary estimate showed. The Current Economic Conditions sub-index rose to 74.0 from 68.3, while the Index of Consumer Expectations surged to 66.4 from 56.8. Expectations for inflation one year ahead declined to 3.1% from November's 4.5%, marking the lowest level recorded since March 2021. Additionally, expectations for the five-year outlook fell to 2.8%, matching the second-lowest reading seen since July 2021.

Key Takeaways: The report's overall tone was very positive mainly due to a catch-up in Republican-leaning respondents improving their outlook and lowering their inflation expectations. The 13% increase in overall sentiment reversed declines seen over the last four months, and given where prices at the pump have gone along with a labor market that is still positive, it makes sense. “All five index components rose this month, led by surges of over 24% for both the short and long-run outlook for business conditions. There was a broad consensus of improved sentiment across age, income, education, geography, and political identification. A growing share of consumers, about 14%, spontaneously mentioned the potential impact of next year’s elections. Sentiment for these consumers appears to incorporate expectations that the elections will likely yield results favorable to the economy.” Basically, Republicans are getting excited that Trump will return and all will be well again in their Fox News world due to recent polls. This trend will likely continue throughout 2024 until the election or Trump is arrested.

*Gains in sub-categories were broad, with overall consumer sentiment significantly beating expectations

*The largest increase in sentiment readings came from respondents affiliated with the Republican Party

The Logistics Manager’s Index fell to 49.4 in November from 56.5 in October, which was the highest in nine months. Inventory levels (-9.1 to 44.3) declined, leading to a dip in Warehousing Capacity (+3.6 to 60.6) and Transportation Capacity (+5.2 to 61.8) and a slowdown in Warehousing Utilization (-14 to 52.9) and Transportation Utilization (-10.7 to 50) slowed. Meanwhile, Inventory Costs (-7.6 to 62.1) continued to rise, although at a slower pace amid tightness in the warehousing market. Warehousing Prices (-6.5 to 64.2) also slowed, and Transportation Prices (-0.2 to 44.2) fell slightly faster.

Key Takeaways: The 7.1-point drop is the largest since the start of the ongoing downturn in logistic activity back in April 2022. However, November’s dip was largely triggered by a decline in inventory levels which is attributable to Q4 holiday sales. There was a similar decline in utilization metrics back in April 2022, but in that instance, it was because inventories were holding still as firms had too much inventory and couldn’t sell any of it. Essentially, November’s decline seems to have come because firms are selling off inventories quickly. The previous large decline from April 2022 happened because firms had too much inventory and couldn’t sell any of it. Both of these scenarios led to large drops in the overall LMI, but this more recent drop is significantly less concerning. Finally, although an overall contraction was reported from upstream respondents, downstream respondents are still seeing some growth. Interestingly, upstream firms are predicting increases in inventory levels going forward, while downstream ones are not. If those predictions hold, we may eventually see freight rates increasing for upstream and downstream firms.

*The overall drop this month was the largest but was less concerning given the sub-index moves

*Inventory levels dropped notably while transportation costs slowed for the first time since April

*Downstream respondents are still seeing some growth, while upstream have moved further into contractionary territory

Technicals, Positioning, and Charts:

The Russell outperformed the Nasdaq and S&P on the week, with the first two only marginally higher, while the S&P was flat on the week. Consumer Discretionary, Communication, and Technology were the best-performing sectors, while Small-Caps, Growth, and Momentum were the best-performing factors. Small-Cap Value was the best-performing size/value combo of the week.

@Koyfin

S&P optionality strike levels have the Zero-Gamma Level at 4524 while the Call Wall is 4600 and the Put Wall is 4400.

@spotgamma

S&P technical levels have support at 4570, then 4440, with resistance at 4620, then 4655.

@AdamMancini4

Treasuries are lower on the day, with the 10yr yield higher by 8.4 bps to 4.23%, while the 5s30s curve is flatter by 4bp on the session, moving to 8bps.

Four Key Macro House Charts:

Growth/Value Ratio: Value is higher on the week, with Small-Cap Value the best-performing size/factor on the week.

Chinese Iron Ore Future Price: Iron Ore futures are higher on the week.

5yr-30yr Treasury Spread: The curve is flatter on the week.

EUR/JPY FX Cross: The Yen is stronger on the week.

Other Charts:

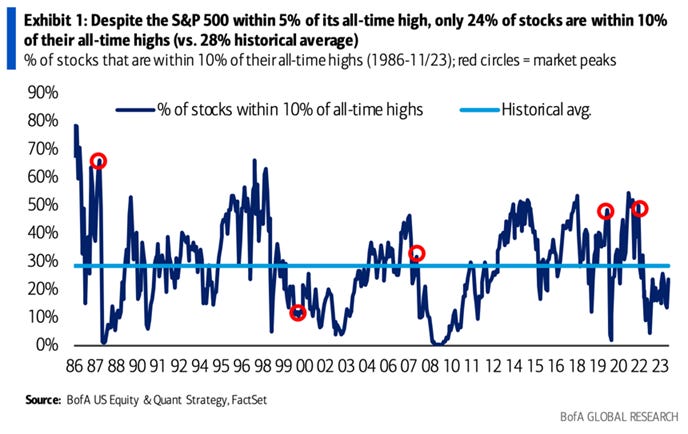

"Only 24% of stocks in the S&P 500 trade within 10% of their all time highs (vs. 28% historical average), much lower vs. prior bull market peaks." - Savita Subramanian of BofA

Removing the “Magnificient Seven” makes the S&P less expensive, but valuations for the equally-weighted S&P are no longer historically cheap.

Investors are back at their most bullish levels since the pandemic, with the 20 level on the AAII US Investor Sentiment Bearish Reading Index historically being an area of reversal.

CTA are as long equities as they have ever been and will likely switch to a more negative positioning on any sell-off quickly.

Investors may be more bullish on stocks, but insiders are not, with an increasing amount selling their holdings.

Market-derived inflation expectations fell heavily in November due to the pullback in oil and gas prices and are now near the lowest levels seen in the prior two years.

Rate vol remains elevated, with the MOVE index remaining range-bound while the VIX has broken down to pre-pandemic lows.

There is an extremely high correlation between liquidity in US markets and Bitcoin. “It’s just a beta play on liquidity,” he said. “Nothing more, nothing less.” If there’s more money around, more of it will find its way into crypto.” said Ian Harnett of Absolute Strategy Research

Russia’s oil product exports rebounded in November as the easing of restrictions on road fuels and the end of refinery maintenance boosted flows.

Articles by Macro Themes:

Medium-term Themes:

China’s Post-Pandemic Life:

Borrow More Responsibility: Cities and provinces across the country have accumulated a massive amount of hidden debt following years of unchecked borrowing and spending. The International Monetary Fund and Wall Street banks estimate that the total outstanding off-balance-sheet government debt is around $7 trillion to $11 trillion. That includes corporate bonds issued by thousands of so-called local-government financing vehicles, which borrowed money to build roads, bridges, and other infrastructure or to fund other expenditures. No one knows what the actual total is, but it has become abundantly clear over the past year that local governments’ debt levels have become unsustainable. Chinese authorities have realized that the risks to the country’s financial stability and overall growth have become too large to ignore. They are trying to tackle the problem more systematically and are starting to swap out some hidden debt for new and explicit government debt. - China’s Colossal Hidden-Debt Problem Is Coming to a Head – WSJ

Longer-term Themes:

Cyber Life and Digital Rights:

Temp Agreement: Lawmakers have reportedly reached an agreement to temporarily extend the Foreign Intelligence Surveillance Act (FISA). The agreement, which will reauthorize FISA through April, is part of bipartisan and bicameral negotiations on the annual National Defense Authorization Act (NDAA). The compromise still needs to be finalized in the text of the NDAA and would need to pass in both the Senate and the House. That is reportedly expected to happen before lawmakers leave Washington for the New Year at the end of next week. Reformers and civil liberties groups argue that Section 702 is over-used to collect large amounts of data without a warrant, including on American citizens whose data is collected when they interact with a foreign target. Lawmakers who support the program are pushing against proposed FISA reforms, saying they would be unworkable and lead to consequential delays in intelligence-gathering. The temporary extension of FISA through April included in the NDAA will buy members of Congress the two sides more time to try to find a compromise that can pass both chambers of Congressn. - Lawmakers reach a deal to temporarily extend major federal surveillance program – NBS News

Keyword Filtering: Thanks in large part to a two-decade-old federal anti-porn law, school districts across the US restrict what students see online using a patchwork of commercial web filters that block vast and often random swathes of the internet. Companies like GoGuardian and Blocksi govern students’ internet use in thousands of US school districts. As the national debate over school censorship focuses on controversial book-banning laws, a WIRED investigation reveals how these automated web filters can perpetuate dangerous censorship on an even greater scale. - Inside America’s School Internet Censorship Machine - Wired

A.I. All Day:

Triangle of Risk: EU lawmakers and governments agreed on provisional terms for regulating artificial intelligence (AI) systems like ChatGPT, taking a step closer to clinching landmark rules governing the technology. The European Commission would maintain a list of AI models deemed to pose a "systemic risk," while providers of general-purpose AIs would have to publish detailed summaries of the content used to train them. EU countries and lawmakers have been trying to finalise details of the draft rules proposed by the Commission two years ago but have struggled to keep up with the rapidly evolving technology. The current balance of rules could become the blueprint for other governments as countries seek to craft rules for their own AI industry, providing an alternative to the U.S.' light-touch approach and China's interim rules. - EU closer to landmark AI Act after marathon overnight talks – Reuters

Energy’s Midlife Crisis:

Retiring Coal: The United States committed to the idea of phasing out coal power plants, joining 56 other nations in kicking the coal habit that’s a huge factor in global warming. U.S. Special Envoy John Kerry announced that America was joining the Powering Past Coal Alliance, which means the Biden Administration commits to building no new coal plants and phasing out existing plants. No date was given for when the existing plants would have to go, but other Biden regulatory actions and international commitments already in the works had meant no coal by 2035. - US joins in other nations in swearing off coal power to clean the climate - AP News

")

Tripling: The United States and 21 other countries pledged at the United Nations climate summit in Dubai to triple nuclear energy capacity by 2050, saying the revival of nuclear power was critical for cutting carbon emissions to near zero in the coming decades. Britain, Canada, France, Ghana, South Korea, Sweden, and the United Arab Emirates were among the 22 countries that signed the declaration to triple capacity from 2020 levels. Tripling nuclear energy capacity by 2050 would require significant investment. In advanced economies, which have nearly 70 percent of global nuclear capacity, investment has stalled as construction costs have soared, projects have run over budget and faced delays. On top of cost, another hurdle to expanding nuclear capacity is that plants are slower to build than many other forms of power. - 22 Countries Pledge to Triple Nuclear Capacity in Push to Cut Fossil Fuels - NYT

Authoritarianism in Trouble?:

Growing Threats: CNN reviewed more than 540 cases involving people who have been federally charged with making threats against public officials or institutions between January 2013 and November 2023. At least 41% of all the cases dealing with “threats” across the decade were politically motivated. Nearly 95% of people prosecuted for making threats to public officials are male; the median age is 37. Politically motivated threats to public officials increased 178% during Trump’s presidency. Threats related to hot political topics like abortion or police brutality also skyrocketed during the Trump years, increasing by more than 300% from Obama’s second term. As the party in power, 16 Democrats received threats during Obama’s second term. This increased 169%, with 43 GOP lawmakers threatened under Trump. “I think Trump gave everyone a license just to say whatever they wanted, make whatever threats they wanted,” said Richard Barron, a former election official in Georgia, who received hundreds of vitriolic and threatening messages after the 2020 election, when Trump lasered in on the state during his failed bid to claim fraud. - A deluge of violent messages: How a surge in threats to public officials could disrupt American democracy - CNN

Cold Places (Deep Sea, Artic, and Space Colonization):

More Work Needed: Despite recent reforms, a new report concluded that the pace of space acquisition in the Defense Department has not kept up with industry. The study by the Defense Business Board, an advisory committee that provides independent business advice to the Department of Defense, concluded that while the establishment of the U.S. Space Force has helped streamline fragmented space acquisition organizations, the Pentagon is still not equipped to procure next-generation space systems at the pace required to maintain dominance. The disconnect between the speed of procurement and industry advancements puts pressure on national security space efforts, the report cautioned. It suggested more authority could be given to the office of the Space Force's senior acquisition executive, currently led by Frank Calvelli, assistant secretary of the Air Force for space acquisition and integration. - Pentagon advisors: Despite reforms, Space Force still shackled to sluggish procurement system - SpaceNews

Other Articles of Interest:

Copycat Cases: The Supreme Court on Thursday froze a bankruptcy reorganization plan for OxyContin maker Purdue Pharma that would have shielded members of the Sackler family, who own the company, from civil claims in exchange for paying up to $6 billion to address the U.S. opioid crisis. Justices will review the agreement and hear arguments in the case in December. It marks a win for the Biden administration after the Justice Department argued the bankruptcy court couldn't grant the family members legal immunity from claims by opioid victims. However, Purdue said it was confident in the legality of the reorganization plan and optimistic the high court would agree. - Supreme Court stops Purdue Pharma bankruptcy deal - Axios

Direct Taxes: The Supreme Court will hear arguments in Moore v. U.S., which challenges a piece of the 2017 tax law that imposed a one-time levy on profits that companies had accumulated outside the U.S. But its implications could reach much further, providing the justices an opportunity to define what Congress can tax under the Constitution—and what it can’t. The case raises a seemingly simple question: Must income be “realized,” or received before it can be taxed? Conservative groups see it as a chance to block future Congresses from taxing wealth or unrealized capital gains. A broad ruling could create a constitutional bar against some popular Democratic proposals to tax the superrich. - One Supreme Court Case Could Mess Up Chunks of the Tax Code – WSJ

Three Scenarios: When NATO celebrates its 75th anniversary at its Washington summit next year, it will do so from a position of unity and strength. This is a remarkable turnaround from only a few years ago, when trans-Atlantic ties were clouded by mutual suspicion and uncertainty about the bloc’s future. The first large-scale war of aggression in Europe since World War II has reinvigorated the alliance, which now has more member states and greater geographic cohesion than ever before. NATO’s renaissance comes just in time, as it may soon face an entirely new geopolitical landscape that will once again test its cohesion and adaptability. The article reviews the potential future of NATO. - NATO’s Remarkable Revival – Foreign Policy

Podcasts and Videos:

China Made a Chip Breakthrough That Shocked The World – OddLots Bloomberg

The Massive Cyberattack You Never Heard About – Bloomberg

For Fun:

Ego, Fear and Money: How the A.I. Fuse Was Lit – NYT

VIEWS EXPRESSED IN “CONTENT” ON THIS WEBSITE OR POSTED IN SOCIAL MEDIA AND OTHER PLATFORMS (COLLECTIVELY, “CONTENT DISTRIBUTION OUTLETS”) ARE MY OWN. THE POSTS ARE NOT DIRECTED TO ANY INVESTORS OR POTENTIAL INVESTORS AND DO NOT CONSTITUTE AN OFFER TO SELL -- OR A SOLICITATION OF AN OFFER TO BUY -- ANY SECURITIES AND MAY NOT BE USED OR RELIED UPON IN EVALUATING THE MERITS OF ANY INVESTMENT. THE CONTENT SHOULD NOT BE CONSTRUED AS OR RELIED UPON IN ANY MANNER AS INVESTMENT, LEGAL, TAX, OR OTHER ADVICE. YOU SHOULD CONSULT YOUR OWN ADVISERS AS TO LEGAL, BUSINESS, TAX, AND OTHER RELATED MATTERS CONCERNING ANY INVESTMENT. ANY PROJECTIONS, ESTIMATES, FORECASTS, TARGETS, PROSPECTS AND/OR OPINIONS EXPRESSED IN THESE MATERIALS ARE SUBJECT TO CHANGE WITHOUT NOTICE AND MAY DIFFER OR BE CONTRARY TO OPINIONS EXPRESSED BY OTHERS. ANY CHARTS PROVIDED HERE ARE FOR INFORMATIONAL PURPOSES ONLY, AND SHOULD NOT BE RELIED UPON WHEN MAKING ANY INVESTMENT DECISION. CERTAIN INFORMATION CONTAINED IN HERE HAS BEEN OBTAINED FROM THIRD-PARTY SOURCES. WHILE TAKEN FROM SOURCES BELIEVED TO BE RELIABLE, I HAVE NOT INDEPENDENTLY VERIFIED SUCH INFORMATION AND MAKE NO REPRESENTATIONS ABOUT THE ENDURING ACCURACY OF THE INFORMATION. I MAY OR MAY NOT HAVE POSITIONS IN ANY STOCKS OR ASSET CLASSES MENTIONED. I HAVE NO AFFILIATION WITH ANY OF THE COMPANIES OTHER THAN EXPLICITLY MENTIONED.