MIDDAY MACRO - 9/3/2021

Daily Color on Markets, Policy, and Geo-Politic

MIDDAY MACRO - DAILY COLOR – 9/3/2021

OVERNIGHT/MORNING RECAP & MARKET ANALYSIS

Narratives/Price Action:

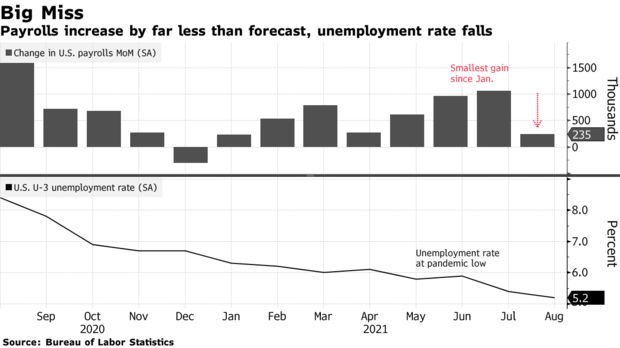

Equities are mixed, after a significant miss in headline NFP caused a drop that is now rebounding, led by Tech and Growth

Treasuries are lower, with the belly well anchored but the long-end under pressure as traders reassess Fed policy in light of the weaker data

WTI is lower, undoing some of its mid-week rally as traders now look past this week’s OPEC+ meeting to other demand/supply uncertainties

Analysis:

Equities dropped following this morning's worse-than-expected jobs report as bad news was apparently just bad news, leaving (likely junior) traders (in a low volume market) to reduce risk into the holiday weekend despite the increased probability of a later and longer Fed taper.

The Nasdaq is outperforming the S&P and Russell with Growth, Low Volatility, Momentum factors, and Technology, Healthcare, and Communication sectors are all outperforming.

S&P optionality strike levels have the zero gamma level at 4467 while the call wall remains at 4550; technical levels have support at 4515, and resistance is 4535.

Treasuries are mixed, with the curve steepening and the belly supported after weaker jobs data pushed back Fed tightening expectations.

We are coming up on a decision point for the “reflation trade” next week as traders return from holiday and put on positions, believing they have a better picture of economic growth, Delta, and the Fed.

In conjunction with other economic data seen recently, today's jobs and service PMI data shows growth continuing to be capped from shortages of materials and labor (while demand holds up) and a less optimistic consumer/worker burdened by higher prices and Delta-related uncertainties.

This emboldens the view that the Fed will remain patient and overly accommodative due to uncertainty over their outlook and a slower pace of “substantial progress” on the labor front being achieved.

It also allows for “hope” to build, as the current drag occurring from Delta and supply-side disruptions can still reverse into year-end, renewing the reopening demand/activity that never fully got unleashed over the summer.

We have a low conviction that this will occur for two main reasons; there has been no significant improvement in supply-side disruptions, and we simply don’t know how school re-openings (and the potential for another uptick in Delta cases) will go.

However, we expect reflation trades to increasingly be put on (continuing its past two-week recovery), helping small-cap and value outperform and steepening the Treasury curve before the Delta effects of school re-openings and longevity of supply-side disruptions emerge, clearing the picture one way or another into year-end.

This view continues our current mantra of dip-buying and tight stop-trails during the continuation of the current equity index melt-up, with a more reflationary themed outperformance (supported by higher yields and a weaker dollar) through the beginning of September.

Econ Data:

Nonfarm Payrolls increased by 235K, with private payrolls higher by 243K, far less than expected. The prior two months were revised 134K higher (entirely in private payrolls). Leisure and Hospitality hiring saw no change while Professional & Business Services increased by 74K. Retail employment decreased by 29K. The unemployment rate decreased to 5.2% from 5.4% (3.5% in February 2020), the participation rate was unchanged at 61.7% (63.3% pre-Covid), and the U6 underemployment rate fell to 8.8% from 9.2% (7.0% pre-Covid). The Fed favorite Employment-Population ratio increased slightly to 58.5% from 58.4%. Finally, Average Hourly Earnings increased 0.6% MoM, up from 0.4% in July, while Average Hours Worked decreased to 0.2% MoM from 0.6%.

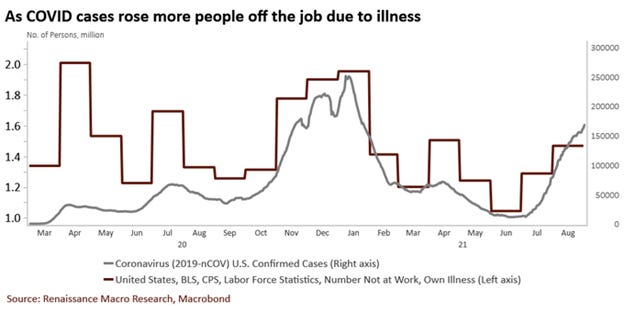

Why it Matter: A sizeable miss from a report that is clearly capturing the effects of the rise in Delta. This is seen in the unchanged leisure and hospitality employment, a small rise in teleworking from 13.2% in July to 13.4% in August, and the first increase in the number of people unable to work because of the impact of Covid on their employer since December (an increase of 497K). However, the labor market is still clearly tight, with average hourly earnings rising 0.6% in the month and by 4.3% over the last year. We see this further follow-through in wage growth as confirming our belief we are well into a wage-spiral inflation cycle. Even with the weaker headline number, the Fed is still on track to make “substantial progress” to allow a tapering announcement at the end of this year. However, given the data is now muddied again by the rise in Delta cases and uncertainty is growing around school re-openings and the holiday season, they have plenty of reason to remain cautious and patient.

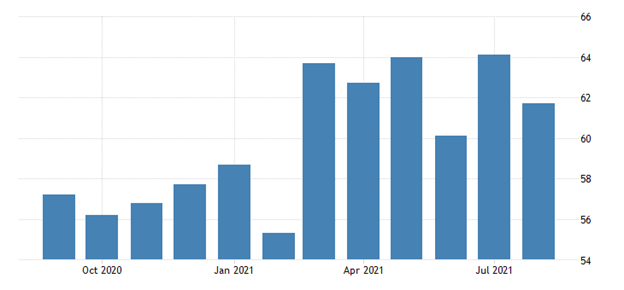

The ISM Services PMI registered 61.7%, 2.4% points lower than the all-time high reading of 64.1 in July. Business activity was the biggest drag, decreasing to 60.1 from 67 in July. New Orders and Employment was little changed. Supply chain disruption-themed sub-indexes slightly improved, with Supplier Deliveries and Prices both dropping. Inventories and Backlog of Orders both decreased, giving a neutral view on future demand as the two offset each other but were little changed.

Why it Matters: Given our concerns regarding the impact of Delta, the service PMI held in better than expected. There was some improvement in supply-chain-related sub-indexes and no change in the employment situation, respondent comments continue to highlight severe shortages of materials and labor. The majority of comments reflected firms still seeing strong demand, as confirmed by a steady New Order sub-index. Finally, the list of commodities up in price and in short supply continues to grow despite the drop in the Prices sub-index, reflecting a broader shortage of things.

TECHNICALS / CHARTS

FOUR KEY MACRO HOUSE CHARTS:

Growth/Value Ratio: Growth is higher on the week, helped by an outperforming Nasdaq today

Chinese Iron Ore Future Price: Iron Ore futures are lower on the week; in contrast, coking coal continues to rally, showing the difference in supply situations between the two even as steel demand weakens.

5yr-30yr Treasury Spread: The curve is steeper on the week, moving further into its post-June range, higher 3bps today.

EUR/JPY FX Cross: The Euro is stronger on the week, meeting some resistance at the top of its recent down-channel verse the Yen.

HOUSE THEMES / ARTICLES

MEDIUM-TERM THEMES:

China Macroprudential and Political Tightening:

Ante-up: Chinese state firms to take big stake in Ant's credit-scoring JV - Reuters

State-backed firms are set to take a sizeable stake in a key Ant Group asset for the first time, a move that will loosen the Chinese fintech giant's grip on a data treasure trove of over 1 billion users but help revive its IPO. The end goal of the state-private partnership is to form a personal credit-scoring firm, establishing what would be China's third licensed personal credit-scoring firm as soon as October.

Why it Matters:

The plan, part of Ant's business revamp, would represent one of the most prominent outcomes of a government push for state-backed firms to exert more control and influence over fast-growing but previously lightly regulated new-economy businesses. E-commerce and fintech firms such as Ant sit on a huge cache of consumer data that is the backbone of China's internet where, in finance, companies' offerings are as varied as loans and investment products sold via smartphones.

EveryXing: Xi Approves Action on Everything From Monopolies to Pollution - Bloomberg

Chinese President Xi Jinping chaired a high-level meeting that “reviewed and approved” measures to fight monopolies, battle pollution, and shore up strategic reserves. The meeting emphasized the need for policy measures to serve the interests of the Communist Party while paying heed to domestic and international markets. Xinhua is expected to publish details from the monthly Politburo meeting soon, likely including the date for the sixth full gathering of the current Central Committee.

Why it Matters:

This can all be seen as further consolidation of power into the hands of Xi and Beijing. The meeting explicitly called for officials to “guide and urge companies to obey the leadership of the party.” As the private sector grows in size and power, it further enriches China’s citizens, and their priorities change. The worry is that the growing middle class will no longer forgive the CCP for its authoritarian oversteps (which they did initially due to the promise of a better life). Instead, they will want more western/democratic freedoms, which is a threat to Beijing.

Curbs to Persist: China’s Restrictions on International Flights Could Last to 2022 - Bloomberg

China’s top three airlines told analysts the government’s tight restrictions on international flights could last into the first half of next year due to Covid-prevention measures ahead of the Beijing Winter Olympics in February. The continuation of curbs means a full international travel recovery isn’t likely until 2024. The carriers remain bullish on a recovery in domestic traffic, with China Eastern expecting a return to normal levels in the first two weeks of October.

Why it Matters:

The three Chinese airlines all suffered hefty losses in the first half of 2021, though the figures were an improvement from a year earlier thanks to a recovery in domestic demand. The airlines’ domestic traffic has already returned to 99% of 2019 levels, up from a low of 73% in the week of Aug. 9, the analysts said. However, don’t expect to see armies of Chinese tourists coming to a neighborhood near you for some time.

LONGER-TERM THEMES:

Electrification Policy:

Trust?: Facebook’s WhatsApp Fined Around $270 Million for EU Privacy Violations – WSJ

The second large EU privacy fine against a U.S. tech company in two months was issued Thursday by Ireland’s Data Protection Commission on behalf of a board representing all of its EU counterparts. It came as part of a decision that found WhatsApp didn’t live up to requirements to tell Europeans how their personal information is gathered and used, including regarding the sharing of their information with other Facebook units.

Why it Matters:

The WhatsApp decision is the latest in a wave of enforcement from EU regulators and comes after activists have complained that Europe’s application of GDPR has been too slow and weak. Ireland’s privacy regulator says more decisions are in the works. The days of selling personnel data may be ending in certain regions.

Shut it Down: Internet shutdowns by governments have ‘proliferated at a truly alarming pace’ - Verge

Nearly 850 intentional shutdowns have been recorded over the past 10 years by nonprofit Access Now’s Shutdown Tracker Optimization Project (STOP). They’re most frequently deployed during elections or times of protest, with governments claiming shutdowns are needed to stem the spread of “misinformation.”

Why it Matters:

In addition to the stifling of free speech and assembly, internet shutdowns have significant economic harms. In Myanmar, which has seen the longest-ever government-led internet shutdown in history as part of the recent coup, it’s estimated the economic loss has been equal to 2.5 percent of the country’s GDP, around $2.1 billion. We continue to watch the workaround here as VPN networks grow in popularity, allowing citizens to bypass local restrictions.

Surveillance Downunder: Australia: Unprecedented surveillance bill rushed through parliament in 24 hours.

The Australian government has been moving towards a surveillance state for some years already. Now they are about to pass an unprecedented surveillance bill that allows the police to hack your device, collect or delete your data, and take over your social media accounts. Politicians justify the need for the bill by stating that it is intended to fight child exploitation (CSAM) and terrorism. However, the bill itself enables law enforcement to investigate any offense which is punishable by imprisonment of at least three years, including terrorism, sharing child abuse material, violence, acts of piracy, bankruptcy and company violations, and tax evasion.

Why it Matters:

It's an incredible bill that would effectively allow government agencies to modify, copy, or delete your data with a data disruption warrant; collect intelligence on your online activities with a network activity warrant; also they can take over your social media and other online accounts and profiles with an account takeover warrant. The bill may really be targeted at China’s attempt to infiltrate Australian business and politics, but it requires a lot of trust from Australian citizens that their government will not abuse it.

Commodity Super Cycle Green.0:

Green Diesel: Chevron Makes Pact with Bunge to Join Chase for Renewable Diesel – Bloomberg

Chevron seeks to tap Bunge’s oilseed-processing expertise and farmer relationships to gain a steady source of soy oil that could be used to make cleaner diesel and jet fuel through a partnership announced Thursday. Bunge is expected to contribute soybean processing facilities in Louisiana and Illinois, and Chevron plans to put about $600 million into the venture.

Why it Matters:

U.S. renewable diesel production capacity could surge to 4.9 billion gallons a year by the end of 2024, from about 827 million gallons now. Refiners joining the renewable diesel race include Marathon Petroleum Corp. and HollyFrontier Corp. Agricultural firms, including Andersons Inc., one of the five biggest U.S. grain handlers, have said they’re open deals to take advantage of the fossil-fuel industry’s rapidly growing interest in making less polluting fuels.

ESG Monetary and Fiscal Policy Expansion:

Blocking Progress(ives): Manchin Jolts Democrats by Urging ‘Pause’ on $3.5 Trillion Bill – Bloomberg

Senator Joe Manchin said at an event in his home state on Wednesday and in a Thursday Wall Street Journal op-ed that rising inflation and a soaring national debt necessitate a go-slow approach and a “significantly” smaller plan than the $3.5 trillion one Democratic leaders and the White House have endorsed. Manchin last month voted with other Senate Democrats to help pass a fiscal blueprint that could help enable the broader economic bill to pass the Senate without any GOP support by short-circuiting the filibuster.

Why it Matters:

House panels are beginning work on select portions of the $3.5 trillion package, but timing isn’t clear in the Senate. Pelosi struck a deal with 10 Democratic House moderates, which set a Sept. 27 deadline for a vote on the infrastructure bill. We continue to believe both bills will pass, although the second may be at a smaller size. However, the road forward is very unclear, especially with the chance of a government shutdown lurking.

Oasis Spotting: John Kerry Seeks China’s Climate Cooperation, Gets an Earful on Fraying Ties – WSJ

Mr. Kerry, wrapping up a two-day visit to the northern port city of Tianjin, was warned repeatedly by his hosts that climate cooperation couldn’t be kept separate from worsening geopolitical ties between the two countries. China’s foreign minister, Wang Yi, while describing climate-change cooperation as an oasis in the desert, said that “cooperation on climate change cannot be divorced from the overall situation of China-U.S. relations.”

Why it Matters:

Mr. Kerry’s visit, the third trip to China by a senior Biden administration official and Mr. Kerry’s second this year, comes ahead of a United Nations summit set to take place in Glasgow in November, where world leaders will discuss efforts to cut emissions and support developing nations in pursuing low-emission economic growth. The Biden administration has said it wants to carve out space for cooperation with Beijing on climate change, notwithstanding bilateral frictions in issues including trade, technology, and human rights. This, however, does not look like Beijing’s approach, which will try to extract concessions elsewhere for cooperation on climate change. In the end, China is already well on the road to “greening” their economy due to their domestic priorities (all be it a long way to go still).

VIEWS EXPRESSED IN "CONTENT" ON THIS WEBSITE OR POSTED IN SOCIAL MEDIA AND OTHER PLATFORMS (COLLECTIVELY, "CONTENT DISTRIBUTION OUTLETS") ARE MY OWN. THE POSTS ARE NOT DIRECTED TO ANY INVESTORS OR POTENTIAL INVESTORS, AND DO NOT CONSTITUTE AN OFFER TO SELL -- OR A SOLICITATION OF AN OFFER TO BUY -- ANY SECURITIES, AND MAY NOT BE USED OR RELIED UPON IN EVALUATING THE MERITS OF ANY INVESTMENT.

THE CONTENT SHOULD NOT BE CONSTRUED AS OR RELIED UPON IN ANY MANNER AS INVESTMENT, LEGAL, TAX, OR OTHER ADVICE. YOU SHOULD CONSULT YOUR OWN ADVISERS AS TO LEGAL, BUSINESS, TAX, AND OTHER RELATED MATTERS CONCERNING ANY INVESTMENT. ANY PROJECTIONS, ESTIMATES, FORECASTS, TARGETS, PROSPECTS AND/OR OPINIONS EXPRESSED IN THESE MATERIALS ARE SUBJECT TO CHANGE WITHOUT NOTICE AND MAY DIFFER OR BE CONTRARY TO OPINIONS EXPRESSED BY OTHERS. ANY CHARTS PROVIDED HERE ARE FOR INFORMATIONAL PURPOSES ONLY, AND SHOULD NOT BE RELIED UPON WHEN MAKING ANY INVESTMENT DECISION. CERTAIN INFORMATION CONTAINED IN HERE HAS BEEN OBTAINED FROM THIRD-PARTY SOURCES. WHILE TAKEN FROM SOURCES BELIEVED TO BE RELIABLE, I HAVE NOT INDEPENDENTLY VERIFIED SUCH INFORMATION AND MAKES NO REPRESENTATIONS ABOUT THE ENDURING ACCURACY OF THE INFORMATION OR ITS APPROPRIATENESS FOR A GIVEN SITUATION.