MIDDAY MACRO - 9/15/2021

Daily Color on Markets, Policy, and Geo-Politic

MIDDAY MACRO - DAILY COLOR – 9/15/2021

OVERNIGHT/MORNING RECAP & MARKET ANALYSIS

Narratives/Price Action:

Equities are higher, picking up momentum currently after the S&P chopped around key levels of support for two days

Treasuries are lower, as better than expected economic data and a growing risk positive tone are driving yields higher

WTI is higher, up around 3%, and helped by larger EIA reported inventory drawdowns

Analysis:

Equities are currently bouncing as a more risk-on tone is forming following better than expected Empire State and Industrial Production data as a week of down days may finally be ending while Treasury yields are rising in conjunction with the change in sentiment.

The Russell is outperforming the S&P and Nasdaq with High Dividend Yield, Value, and Momentum factors, and Energy, Industrials, and Financials sectors are outperforming.

S&P optionality strike levels have the zero gamma level at 4449 while the call wall is at 4500; technical levels have support 4430 and resistance 4480.

Treasuries are lower, with the curve slightly flatter as traders now await Retail Sales tomorrow

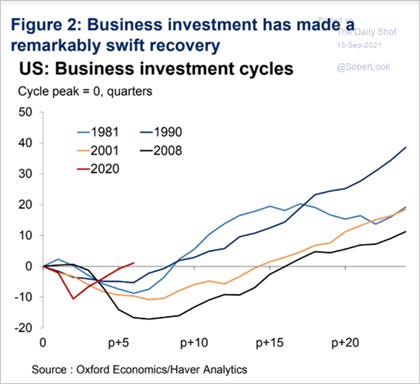

Today’s data painted a rosier picture for the remainder of the year as capital expenditure-orientated purchases and intentions continued to increase, showing firms, although frustrated with shortages of materials and labor, remain generally optimistic about future demand.

Business surveys gauging future capital expenditure plans have been improving, likely driven by the continued shortages causing lost sales and forcing businesses to invest in ways to do more with less.

Actual “tangible” data also shows that firms are spending on Capex, which we saw in today’s data (and further elaborated on in the Econ Data section), although so far its been overwhelmingly on the digital side verse fixed-asset.

However, despite the growing vote of confidence in future demand by businesses, the consensus view into year-end seems to be a growing “stagflationary” outlook keeping retail investors absent as dip buyers in the current pullback (now around -2.5% from ATH).

We don’t believe this negative outlook/dynamic will last, and although cash on the sidelines seems low and investor sentiment is undoubtedly negative, we continue to believe the majority of the “negative” is priced in, and the ongoing re-opening (as Delta cases fall) and the holiday season (as goods/services will be available) will outperform current expectations re-creating a favorable backdrop for the rotation to increase and an outperformance of reflationary themed trades into year-end.

Econ Data:

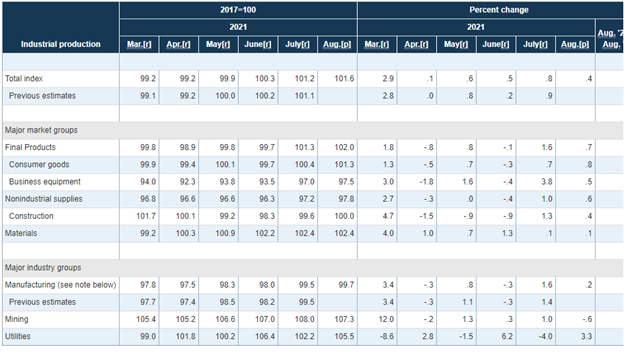

Industrial Production increased 0.4% in August with expectations of 0.5% after moving up 0.8% in July. Final Products for Consumer Goods increased 0.8% MoM while Business Equipment rose 0.5% MoM. Construction Production rose 0.4% MoM. Manufacturing increased by 0.2% MoM, hurt by Mining which was down -0.6% MoM due to shutdowns of oil and gas production in the Gulf of Mexico due to Ida. The output of utilities increased 3.3% on unseasonably warm weather. Capacity utilization increased slightly to 76.4%.

Why it Matters: The Fed reports that "late-month shutdowns related to Hurricane Ida held down the gain in industrial production by an estimated 0.3 percentage point" and "the hurricane forced plant closures for petrochemicals, plastic resins, and petroleum refining." Nonetheless, manufactured output still rose slightly. The increase in business equipment, construction supplies, and business supplies bodes well for stronger future growth as businesses continue to see a reason to invest in themselves.

Empire State Manufacturing Survey General Business Conditions Index increased by 16 points to 34.3 in September from 18.3 last month. New orders (+18.9), shipments (+22.5), and unfilled orders (+5.9) all increased substantially. The delivery times index reached a record high. Labor market indicators pointed to strong growth in employment and the average workweek. Prices Paid decreased slightly while Prices Received indexes rose by 1.8, a new all-time high. Looking ahead, firms remained very optimistic that conditions would improve over the next six months, and capital spending and technology spending plans increased markedly

Why it Matters: Business investment will remain a tailwind in the U.S. as seen in today's Industrial Production and NY Fed’s Empire Survey data. In the Empire Survey, six-month capital spending intention jumped to +33.9, the highest since January 2018, while technology spending plans hit +33, the highest level on record. However, the usual suspects of supply-side disruptions were still apparent. Delivery times hit an all-time high while Inventories only increased modestly, showing that firms are still struggling to get goods to sell for the upcoming holiday season. The stabilization in prices paid vs. continued increase in prices received shows firms are increasingly able to pass prices on and defend profit margins. This, along with continued strong demand, is likely helped support future outlook, with the 6-Month Forward-Looking General Business Conditions Index approaching last year’s highs.

TECHNICALS / CHARTS

FOUR KEY MACRO HOUSE CHARTS:

Growth/Value Ratio: Value is outperforming on the weak, as the Nasdaq is a lagger today

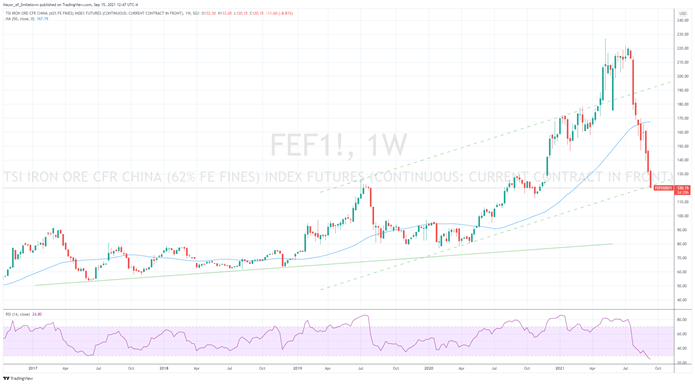

Chinese Iron Ore Future Price: Iron Ore futures are lower on the week, continuing their descent, down over 2% today

5yr-30yr Treasury Spread: The curve is flatter on the week, down slightly today

EUR/JPY FX Cross: The Yen is stronger on the week and slightly higher today following weaker data out of China set a more risk-off tone overnight

HOUSE THEMES / ARTICLES

MEDIUM-TERM THEMES:

Real Supply Side Constraints:

Plastic Trees: Supply-Chain Strains Hit Prices, Inventories of Artificial Christmas Trees – WSJ

Some U.S. retailers of Fake Christmas trees are raising prices by 20% to 25% to keep pace with skyrocketing shipping costs, and they are warning that certain trees could sell out early because deliveries from overseas producers have been hit by the congestion that has tied up distribution networks from ports in China to freight yards in Chicago. One holiday-themed business expects to run low on many holiday items, such as ornaments, toppers, and lights, because of shipping delays. The firm is currently struggling with fall items, such as autumnal wreaths and Halloween decorations. This time last year, the company had about 40,000 fall items in stock. As of the first week of September, it had fewer than 1,500 items.

Why it Matters:

We continue to use this theme to show just how far-reaching the shortage situation is and how dependent we are on foreign manufacturers for our goods. We see the increased number of ships waiting (to unload at ports around the country) as a positive, given it's occurring before the holiday season, showing businesses are adjusting to the challenges while still expecting strong demand. However, there will be price increases, dampening the holiday spirit and weighing on consumer sentiment.

China Macroprudential and Political Tightening:

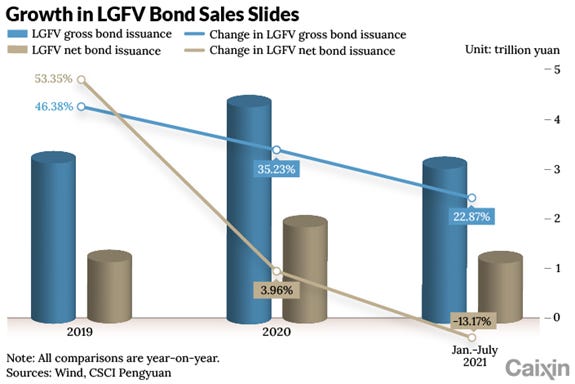

隐性债务: The Never-Ending Battle to Curb China’s Hidden Debt - Caixin

In a document sent to financial institutions recently, the China Banking and Insurance Regulatory Commission laid out a series of existing and new measures to tackle the problem and fix loopholes that have allowed local governments to skirt rules on borrowing limits. There are no official publicly available figures for the scale of local governments’ hidden debt, which refers to their financial liabilities that do not appear on their books, but some estimates put the number at around 50 trillion yuan ($7.7 trillion).

Why it Matters:

Defusing risks from hidden local government debt was listed as one of the top priorities for fiscal work in 2021, with the Ministry of Finance telling lawmakers at the annual meeting of the National People’s Congress that the problem must be to help safeguard overall national security and maintain sustainable economic and fiscal development. Beijing made it clear in the guideline that no one should be under any illusion that the state will step in to provide a bailout in the event of a local debt default.

Lock-Downs Matter: China’s Economic Recovery Is Looking Gloomier – WSJ

Retail sales, a key gauge of China’s consumption, rose just 2.5% in August from a year earlier, down sharply from July’s 8.5% year-over-year growth. Separate data released Wednesday by the statistics bureau showed home sales by value falling 19.7% in August from a year ago, the largest drop since April 2020. The weakness in these two sectors is likely to add to concerns about the growth trajectory in the world’s second-largest economy and prompt questions about whether authorities will intervene to support growth.

Why it Matters:

Consumption has been the weakest link in China’s pandemic recovery and the last corner of the economy to get back on its feet, hurt by stagnant income growth and the government’s stringent Covid-19 measures. The consumer is also China’s biggest stick and carrot tool to court foreign companies and the political influence they have over their governments. If China wants to keep this leverage, it’s going to have to deliver the goods (consumers), something which seems less and less likely given the nationalistic tilt (to consuming) and crackdown campaigns (that are destroying wealth).

LONGER-TERM THEMES:

Commodity Super Cycle Green.0:

Gas Needed: Germany's hydrogen dream needs gas for transition, industry says – Reuters

Germany plans to develop large-scale green hydrogen by using wind and solar electricity to make synthetic fuels for industry, energy, and transport sectors and has launched a 9 billion euro ($10.64 billion) hydrogen strategy up to 2030. However, until that infrastructure is up and running, natural gas will be needed to create hydrogen.

Why it Matters:

Germany's major political parties, which are in the midst of an election campaign, all favor a hydrogen market. Some environmental lobbies want green hydrogen or nothing, while energy companies offer plans for interim steps, including carbon capture and storage (CCS). Given the current rise in natural gas prices and the likely change in leadership, there will be more developments to watch here.

Going Nuclear: Uranium Heats Up, and Hedge Funds Score – WSJ

The price of uranium hit an eight-year high of $44 a pound this week, according to the price tracker UxC LLC. The surge follows the recent launch of an exchange-traded trust by Sprott Asset Management LP, which has bought large stockpiles of uranium after raising money from shareholders and emerged as a favored trading vehicle in its own right, traders said. “It’s become a momentum trade that’s kind of self-fulfilling,” said Kevin Smith, managing director for energy-metals trading at Traxys Group, one of the biggest uranium traders globally.

Why it Matters:

Uranium prices languished for years after the meltdowns at nuclear reactors in Fukushima in 2011. Demand for the fuel dropped as concern about the safety of nuclear power prompted Japan, Germany, and others to turn off reactors, and a glut emerged. More recently, uranium bulls have contended that achieving global goals to cut carbon emissions in the coming years will require nuclear power, which would boost the uranium sector.

ESG Monetary and Fiscal Policy Expansion:

What to Do?: Democrats Put Off Hard Decisions on $3.5 Trillion Spending Plan for Now – WSJ

Centrist Senate Democrats are raising concerns over Democratic leaders’ plans to assemble a package of $3.5 trillion in spending and tax cuts, even if offset by other sources of revenue and savings. Because Democrats cannot afford to lose a single vote from their own caucus in the evenly-split Senate, that means that overall spending level will likely have to come down, either by excluding or shortening the length of some proposed programs.

Why it Matters:

While party leaders agreed on the $3.5 trillion package, they aren’t bound to that spending level. The budget resolution passed by both chambers doesn’t require the overall spending level to be set or capped at $3.5 trillion. Instead, the Senate budget resolution specifies that it can add no more than roughly $1.75 trillion to the deficit over ten years. Bottom line, we still believe this will get done, but at a lower dollar amount (reducing offsetting tax increases) likely on a longer negotiating timeline, which given our view inflation will slow and growth will pick into year-end, likely means eventual passage will help support risk sentiment more in the first half of 2022 than this year.

Missing Person Report: Yellen’s Treasury Work Blunted With Many Key Posts Unfilled – Bloomberg

Treasury Secretary Janet Yellen has one of the biggest to-do lists in Washington: usher in a global tax overhaul, press Wall Street on climate change, and distribute billions of dollars in Covid-relief funds. Yet her efforts are hampered by vacancies in the Treasury’s top ranks. Part of the trouble: top Senate Republicans are threatening to hold five Treasury nominations indefinitely, over demands for the White House to undo a deal allowing the completion of the Germany-Russia Nord Stream 2 project.

Why it Matters:

The vacancies leave the department at risk of losing influence across the administration, such as in the government-wide review of China policy that’s been underway for months. Still, Yellen has achieved several key initiatives for Biden. In July, she led the Group of 20 finance ministers in striking a deal on global taxes that had eluded negotiators for nearly a decade. One area where Yellen’s department has a smaller footprint than expected is in U.S.-China relations.

VIEWS EXPRESSED IN "CONTENT" ON THIS WEBSITE OR POSTED IN SOCIAL MEDIA AND OTHER PLATFORMS (COLLECTIVELY, "CONTENT DISTRIBUTION OUTLETS") ARE MY OWN. THE POSTS ARE NOT DIRECTED TO ANY INVESTORS OR POTENTIAL INVESTORS, AND DO NOT CONSTITUTE AN OFFER TO SELL -- OR A SOLICITATION OF AN OFFER TO BUY -- ANY SECURITIES, AND MAY NOT BE USED OR RELIED UPON IN EVALUATING THE MERITS OF ANY INVESTMENT.

THE CONTENT SHOULD NOT BE CONSTRUED AS OR RELIED UPON IN ANY MANNER AS INVESTMENT, LEGAL, TAX, OR OTHER ADVICE. YOU SHOULD CONSULT YOUR OWN ADVISERS AS TO LEGAL, BUSINESS, TAX, AND OTHER RELATED MATTERS CONCERNING ANY INVESTMENT. ANY PROJECTIONS, ESTIMATES, FORECASTS, TARGETS, PROSPECTS AND/OR OPINIONS EXPRESSED IN THESE MATERIALS ARE SUBJECT TO CHANGE WITHOUT NOTICE AND MAY DIFFER OR BE CONTRARY TO OPINIONS EXPRESSED BY OTHERS. ANY CHARTS PROVIDED HERE ARE FOR INFORMATIONAL PURPOSES ONLY, AND SHOULD NOT BE RELIED UPON WHEN MAKING ANY INVESTMENT DECISION. CERTAIN INFORMATION CONTAINED IN HERE HAS BEEN OBTAINED FROM THIRD-PARTY SOURCES. WHILE TAKEN FROM SOURCES BELIEVED TO BE RELIABLE, I HAVE NOT INDEPENDENTLY VERIFIED SUCH INFORMATION AND MAKES NO REPRESENTATIONS ABOUT THE ENDURING ACCURACY OF THE INFORMATION OR ITS APPROPRIATENESS FOR A GIVEN SITUATION.