MIDDAY MACRO - 8/17/2021

Daily Color on Markets, Policy, and Geo-Politics

MIDDAY MACRO - DAILY COLOR – 8/17/2021

OVERNIGHT/MORNING RECAP & MARKET ANALYSIS

Narratives/Price Action:

Equities are lower, as overnight weakness continuing through the morning’s data and NY-open, with Delta and China again weighing on sentiment

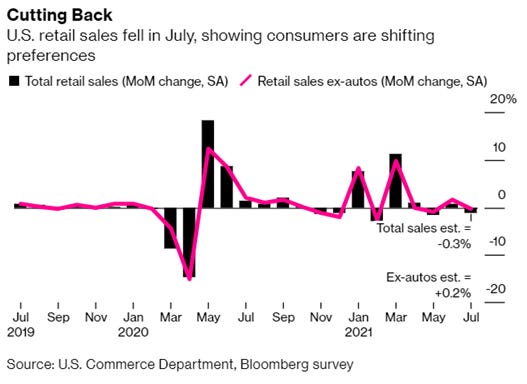

Treasuries are slightly lower, with overnight strength being lost post Retail Sales, despite the data coming in weaker than expected

WTI is lower, with a morning rally now reversing as traders continue to weigh the global growth/demand outlook

Analysis:

Equities are notably lower, with risk sentiment weakening on the back of continued rises in Delta cases domestically, renewed/increased shutdowns abroad, and concerns over the Fed’s tapering pace, leading dip buyers to be absent in today's pullback so far. At the same time, Treasuries are relatively flat after overnight strength faded.

The S&P is outperforming the Nasdaq and Russell with Low Volatility, Value, and High Dividend Yield factors, and Health Care, Consumer Staples, and Real Estate sectors are all outperforming.

S&P optionality strike levels have zero gamma level at 4418 while the call wall is 4500; technical levels have support at 4430, and resistance is 4470.

Treasuries are little changed, with the curve slightly flatter on the session as weaker Retail Sales data failed to elicit a bid, but the general risk-off tone is now supporting price levels.

The more positive tone seen yesterday afternoon in equities reversed overnight, with selling increasing as the S&P broke through tactical support levels while other risk-off indicators are signaling trouble.

Although Delta concerns and uncertainty over China continue to be the main drivers of risk sentiment tactically, today’s price action looks to be reflecting a growing belief that the Fed will announce a faster pace of tapering in September.

As a result, concerns over reduced excess liquidity are weighing on growth and value factors, driving overall equity markets lower while Treasuries are reluctant to rally.

FX markets are also indicating a more risk-off sentiment, with the yen currently the best G10 performer on the quarter, while the U.S. Dollar and Swiss Franc are also well bid.

Finally, commodities are broadly weaker today, with copper breaking lower (-2.8%) through its March 2020 uptrend channel as stronger than expected Industrial Production data did little to change sentiment there.

Stepping back, this could be the beginning of a more sustained pullback in risk-assets into the Jackson Hole Symposium as traders look for clarity on tapering while awaiting the peaking of Delta cases domestically and clarity on further stimulus from China.

Econ Data:

Retail Sales data for July fell -1.1% MoM, missing expectations of a -0.3% decline. Excluding motor vehicles and parts, the monthly decline was -0.4. June’s monthly increase was revised higher to 0.7%. The drop in July sales was fairly broad, with 8 of 13 categories registering decreases. Clothing and Sporting Goods & Hobbies were notably weaker as back to school (or work) buying did not meaningfully materialize (yet). Online sales were significantly weaker than expected, potential due to Amazon moving its Prime Day into June. Restaurants and bars were a bright spot, with sales rising 1.7% over the month but lower than June’s growth rate.

Why it Matters: This was a weak Retail Sales report, which many expected due to previously known slowing credit card usage data. It continued to show a consumer moving away from goods to services but at a weaker rate than in June. Interestingly the increase in restaurant spending contrasted with OpenTable bookings, which moderated throughout the month, indicating that the effects of Delta, which worsened throughout July, may not have been fully captured. The drag coming from autos was more due to limited inventory than a lack of demand. However, auto price increases are weakening consumers' buying intentions, as seen in the Univ. of Michigans Consumer survey.

Industrial production increased 0.9% in July, beating expectations for an increase of 0.5% after moving up 0.2% in June. Manufacturing output rose 1.4%, with about half of the gain in factory output attributable to a jump of 11.2% for motor vehicles and parts production, as many vehicle manufacturers trimmed or canceled their typical July shutdowns. Excluding autos and parts, manufacturing output rose 0.7%. Manufacturing capacity utilization, a measure of plant use, jumped to 76.6%, finally breaking above the pre-pandemic level of 75.5%. Utility output decreased 2.1% in July, with temperatures somewhat below average, while mining output rose 1.2% after a 0.5% gain in June.

Why it Matters: The continued supply-side shortages/disruptions (in both labor and materials) show that there is still room for further growth in factory output, especially if producers have more success filling open positions. There was an increase of 27k manufacturing jobs in the last BLS report, bringing the total to 433k, still below the February 2020 level. We also haven’t seen any improvement in “the ability to find qualified workers” from regional Fed business surveys, leading us to worry this problem will persist and continue to cap growth. Elsewhere we are encouraged by the increase in the production of business equipment (+2.8%), the most in four months, while the output of construction supplies climbed 0.9%, the first gain since March. This bodes well for third-quarter GDP growth being supported by greater investment spending.

TECHNICALS / CHARTS

FOUR KEY MACRO HOUSE CHARTS:

Growth/Value Ratio: Growth is outperforming Value today, but the ratio is little changed on the week as tapering concerns reduce the allure of growth defensively

Chinese Iron Ore Future Price: Iron Ore futures are lower on the week as steel output continues to fall and demand weakens

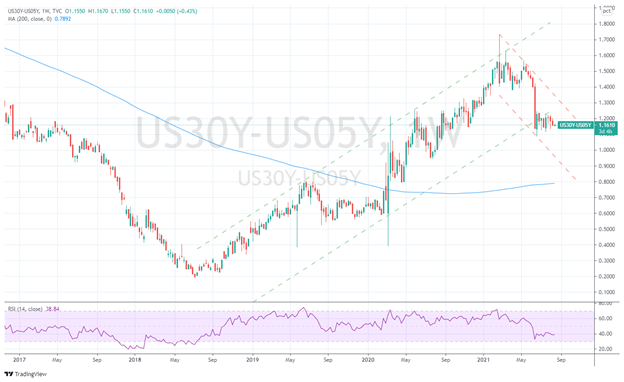

5yr-30yr Treasury Spread: The curve is little changed on the week as overnight strength in the long-end faded post-U.S. data

EUR/JPY FX Cross: Yen is notably higher on the week as the FX markets continue to reflect a more risk off tone

HOUSE THEMES / ARTICLES

MEDIUM-TERM THEMES:

China Macroprudential and Political Tightening:

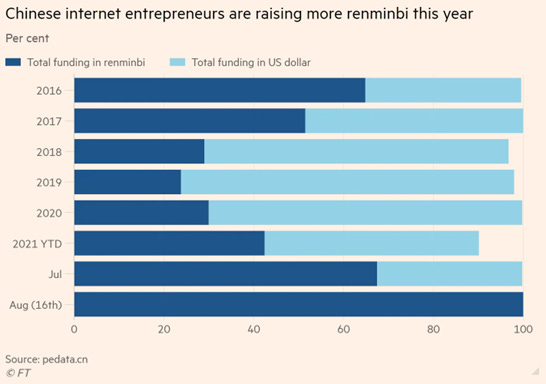

Yuan > Dollar: Chinese tech entrepreneurs grow wary of foreign funding - FT

For Chinese entrepreneurs in an increasing number of sectors, the currency they choose to raise from venture capitalists is a growing point of consideration. There are early signs that the preference for renminbi is now expanding. This is due to the growing uncertainty of whether VIE structures, which bypass China’s foreign investment restrictions, will be allowed in the future.

Why it Matters:

For the past three years, dollar funding accounted for about 70% of Chinese internet start-ups’ total fundraising haul, with the remainder raising renminbi. In July and August, as regulators kicked off investigations into Didi and halted US IPOs, that flipped so renminbi accounted for 70% of internet start-ups’ investment haul. Beijing wants to move its start-up community away from foreign investment and dollar needs.

Take a Seat: Beijing takes stake, board seat in ByteDance's key China entity - Reuters

ByteDance sold a 1% stake in an April 30 deal to WangTouZhongWen Technology, which is owned by three state entities, citing Tianyancha, an online database of China's corporate records. The deal also allowed the Chinese government to appoint a board director at Beijing ByteDance. The deal does not give the Chinese government any stake in the firm's hit short video app TikTok because of ByteDance's complex corporate structure.

Why it Matters:

Further investment in the country’s major internet companies is likely to continue with the backing of the CIIF, which was cobbled together with funding from state-owned banks and companies, with oversight by the CAC and the Ministry of Finance. Wu, the government official with a seat on Beijing ByteDance Technology’s board, has spent most of his public sector career in propaganda since he joined China’s Ministry of Education in 2007, according to Chinese government websites and official media reports. The bottom line is Beijing is taking a more significant role in social media companies to push its agenda.

LONGER-TERM THEMES:

National Security Assets in a Multipolar World:

Chip Overload: China’s semiconductor output hits record high in July as new capacity added to meet strong demand – SCMP

China’s integrated circuit (IC) output rose more than 41.3% YoY in July, a new monthly record. Chip production is a priority in China’s five-year plan as the country braces for a heightened tech war with the US. The value-added industrial output in computing, telecommunications, and electronics manufacturing, one of the 17 main sub-sectors tracked in China’s industrial output, rose 13% in the last month from a year earlier, outperforming overall industrial output growth of 6.4%.

Why it Matters:

A global semiconductor crunch, which started in the second half of last year, is still wreaking havoc on industries from automobiles to consumer electronics. China’s output of automobiles in July fell 15.8% from a year earlier, partly due to chip supply problems, according to the statistics bureau. It's not surprising to see China quickly ramping up its production levels while also adding capacity. The real test will be how quickly they can move on to more complicated chip production.

Electrification Policy:

100 Million: T-Mobile Confirms It Was Hacked - Vice

T-Mobile confirmed they were hacked after a seller of the stolen data told Motherboard that 100 million people had their data compromised in the breach. In the forum post, they offered data on 30 million people for six bitcoin, or around $270,000. The seller said that the data includes social security numbers, phone numbers, names, physical addresses, unique IMEI numbers, and driver's license information.

Why it Matters:

T-Mobile is still accessing the situation across its systems to identify the nature of any data that was illegally accessed. If what is currently reported is true, it will be one of the bigger personal information hacks ever. There will likely be little fallout for T-Mobile, though, as we have all been conditioned to accept that our personal information will be available for sale on the dark web. This is also not their first hack, showing they continue to underinvest in data security.

Commodity Super Cycle Green.0:

Transition: Glencore backs battery start-up behind plans for UK’s first gigafactory - FT

Glencore has acquired a stake in Britishvolt, the battery start-up behind ambitious plans for a gigafactory designed to equip the UK’s car industry for an electric future. As part of the agreement, Glencore will also supply the gigafactory, which is under construction in Northumberland, with cobalt. The world’s biggest producer of cobalt, Glencore will supply 30% of the metal that Britishvolt uses from 2024 to 2030.

Why it Matters:

With the UK banning petrol and diesel vehicle sales from 2030, the car industry is under pressure to establish the infrastructure, including the supply of batteries, to produce electric cars at scale and protect jobs. Six companies are in talks with the UK government about building battery gigafactories, but only Britishvolt, which is still testing its chemistry, and Nissan have publicly declared their plans. The weight of electric batteries and the importance of having a secure source will support the need to have local production in more and more countries.

VIEWS EXPRESSED IN "CONTENT" ON THIS WEBSITE OR POSTED IN SOCIAL MEDIA AND OTHER PLATFORMS (COLLECTIVELY, "CONTENT DISTRIBUTION OUTLETS") ARE MY OWN. THE POSTS ARE NOT DIRECTED TO ANY INVESTORS OR POTENTIAL INVESTORS, AND DO NOT CONSTITUTE AN OFFER TO SELL -- OR A SOLICITATION OF AN OFFER TO BUY -- ANY SECURITIES, AND MAY NOT BE USED OR RELIED UPON IN EVALUATING THE MERITS OF ANY INVESTMENT.

THE CONTENT SHOULD NOT BE CONSTRUED AS OR RELIED UPON IN ANY MANNER AS INVESTMENT, LEGAL, TAX, OR OTHER ADVICE. YOU SHOULD CONSULT YOUR OWN ADVISERS AS TO LEGAL, BUSINESS, TAX, AND OTHER RELATED MATTERS CONCERNING ANY INVESTMENT. ANY PROJECTIONS, ESTIMATES, FORECASTS, TARGETS, PROSPECTS AND/OR OPINIONS EXPRESSED IN THESE MATERIALS ARE SUBJECT TO CHANGE WITHOUT NOTICE AND MAY DIFFER OR BE CONTRARY TO OPINIONS EXPRESSED BY OTHERS. ANY CHARTS PROVIDED HERE ARE FOR INFORMATIONAL PURPOSES ONLY, AND SHOULD NOT BE RELIED UPON WHEN MAKING ANY INVESTMENT DECISION. CERTAIN INFORMATION CONTAINED IN HERE HAS BEEN OBTAINED FROM THIRD-PARTY SOURCES. WHILE TAKEN FROM SOURCES BELIEVED TO BE RELIABLE, I HAVE NOT INDEPENDENTLY VERIFIED SUCH INFORMATION AND MAKES NO REPRESENTATIONS ABOUT THE ENDURING ACCURACY OF THE INFORMATION OR ITS APPROPRIATENESS FOR A GIVEN SITUATION.