MIDDAY MACRO - 7/28/2021

Daily Color on Markets, Policy, and Geo-Politics

MIDDAY MACRO - DAILY COLOR – 7/28/2021

OVERNIGHT/MORNING RECAP & MARKET ANALYSIS

Narratives/Price Action:

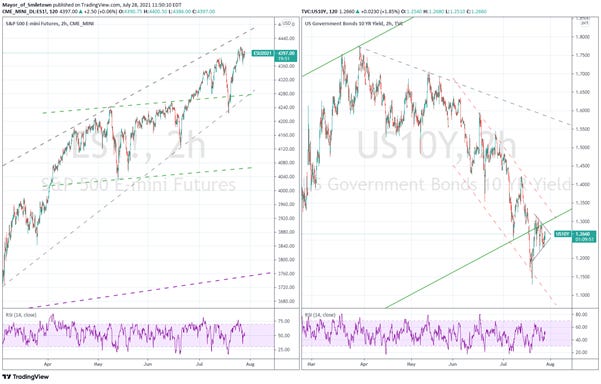

Equities are higher, with generally strong earnings eliciting mixed reactions initially but morphing into positive price momentum now

Treasuries are lower, as the curve slightly steepens while traders await the FOMC meeting’s results this afternoon

WTI is higher, continuing to consolidate in a tight range since last Friday as inventory data this AM failed to change sentiment meaningfully

Analysis:

Beijing’s private calls to banks yesterday may have stopped the bleeding there for now, while strong earnings (with mixed outlooks) are supporting U.S. equity markets and moving Treasuries slightly lower.

The Russell is outperforming the Nasdaq and S&P with Growth, Momentum, and Small-Cap factors, and Communications, Energy, and Materials sectors all outperforming.

S&P optionality strike levels increased with the zero gamma level moving to 4362 while the call wall remains at 4400; technical levels have support at 4385, then 4360, and resistance at 4415, then 4430.

10yr Treasury yields continue to be stuck in a tightening range and the flattening of the curve has lost momentum; however, all eyes will be on any changes to policy following today’s FOMC meetings conclusion.

Our expectations are for minimal changes to the statement and overall message from the Fed today, as a “dovishly-dragged” Powell’s FOMC continues to be committed to being “late, but not behind the curve.”

As a reminder, normalization already began in January, and even with the shortest recession on record, the “tightening” cycle will be a long protracted process verse prior episodes.

Tapering of purchases and the ultimate balance sheet size will not be announced yet, and we expect it only at November’s meeting at the earliest, but potentially as late as December.

This will be due to a lack of clean data, as labor markets will only normalize late fall, and the persistence of “transitory” inflation will, well, continue to be seen as transitory. At the same time, the increases in Delta cases and uncertainty over infrastructure/fiscal spending will provide cover for further patience.

Finally, the succession of key personnel (Powell, Clarida, and Quarles) will need to be set before a true regime shift can be embarked upon (changing course mid-voyage does not go over well)

Bringing it all together, we should continue to have favorable financial conditions which will be supportive of the grind higher in equities (and the BTD mentality on display today) until a more stagflationary environment comes forth next year.

Econ Data:

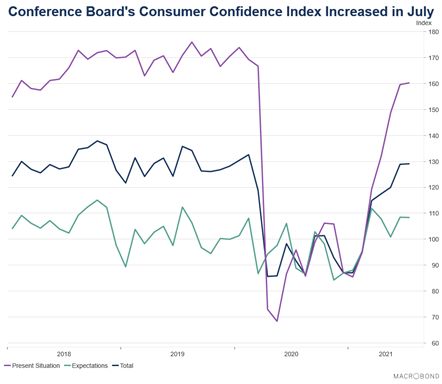

Yesterday’s Consumer Confidence Index, put out by the Conference Board, increased slightly in July. Consumers’ view of present-day conditions rose, suggesting economic growth in Q3 is off to a strong start. Consumers’ optimism about the short-term outlook held steady, and they continued to expect that business conditions, jobs, and personal financial prospects will improve. Short-term inflation expectations eased slightly but remained elevated. Spending intentions picked up in July, with a larger percentage of consumers saying they planned to purchase homes, automobiles, and major appliances in the coming months.

Why it Matters: This was a more upbeat report that showed the consumer has yet to change behavior due to increasing inflationary costs. Plans to buy larger ticket items such as autos and appliances increased. The one-year inflation expectation remained elevated at 6.6% in July which was in line with both May (6.5%) and June's (6.7%) expectations and well above the pre-pandemic reading of 4.5%. Finally, the increase in labor market differential gained slightly and is at historical highs, helping consumers feel confident about future job prospects. Friday will bring us the Univ. of Michigan, which has been cooling lately, helping complete the consumer confidence picture.

TECHNICALS / CHARTS

FOUR KEY MACRO HOUSE CHARTS:

Growth/Value Ratio: Value is higher on the week as the completion of an infrastructure bill may be helping reflation factors

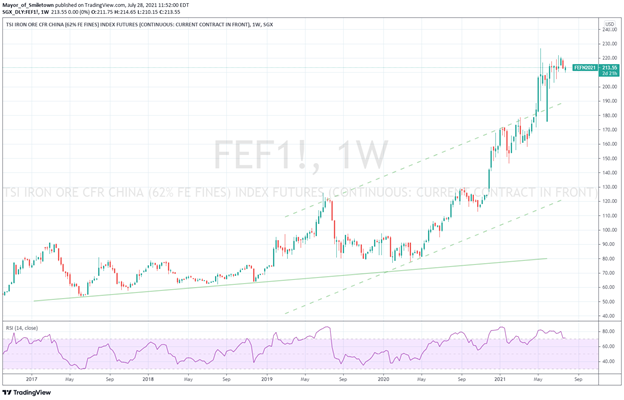

Chinese Iron Ore Future Price: Iron ore is higher on the week given supply disruptions

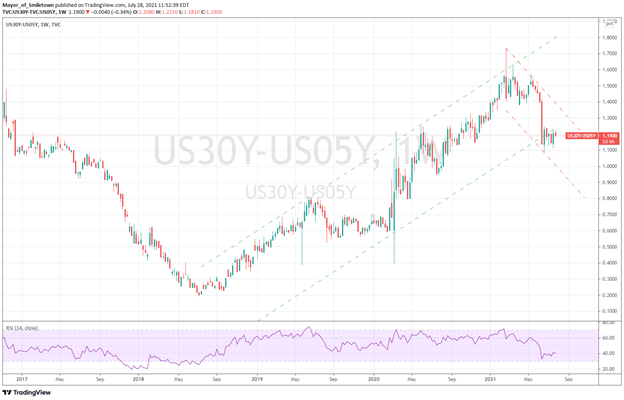

5yr-30yr Treasury Spread: The curve is flatter on the week as FOMC and infrastructure uncertainty keep traders patient

EUR/JPY FX Cross: Euro is little changed on the week, as Asia growth was downgraded by IMF

HOUSE THEMES / ARTICLES

MEDIUM-TERM THEMES:

Real Supply Side Constraints:

Now it’s the Actual Fuel: Airlines Struggle With Fuel Shortages at Some Smaller Western U.S. Airports – WSJ

Many carriers during the pandemic added flights to destinations that became popular among travelers looking to avoid congested cities. But getting enough fuel to some of those airports has grown harder in recent weeks due to a dearth of truck drivers and insufficient space on pipelines, airline officials have said. At the same time, there is growing competition for jet fuel in the region from planes that fly over wildfires and drop water and retardant to squelch blazes.

Why it Matters:

The jet fuel shortage is the latest challenge to the industry and consumers alike as a travel boom this year has collided with labor shortages and other logistical challenges as airlines try to revive a business hobbled by the pandemic. There is some indication the jet fuel problems could spread beyond the West. American Airline Group said it might have to add fuel stops to specific routes and told pilots they might need to carry extra fuel on some flights.

China Macroprudential and Political Tightening:

What’s All This Now?: Spiraling Debt Crisis Confronts Evergrande Billionaire — and Xi - Bloomberg

China Evergrande is quickly becoming the biggest financial worry in a nation with no shortage of financial worries. In 12 short months, the company’s stock price has collapsed more than 70%, and its bonds have dropped below 50 cents on the dollar to record lows. S&P Global Ratings cut Evergrande’s credit rating by two notches Monday. Three banks with combined exposure to Evergrande of $7.1 billion recently decided not to renew some loans when they mature this year. The company will now sell assets and likely need a state-sponsored bailout of some sort.

Why it Matters:

Evergrande is too big to fail, in our opinion. As much as Xi wants to rein in freewheeling billionaires, CEO Hui is not that type and in good standings with the Party. Further, a collapse of the company would be felt by many millions of ordinary Chinese, and that can’t happen as big brother is always there to help the little guy. We also disagree that bailing out Evergrande would set a bad precedent. That message is clear, as seen elsewhere, and reckless business practices (that exploit individuals) will continue to be punished.

Sanctions are the New Tariffs: China Move to Fight Sanctions Gives Hong Kong Banks New Worry – Bloomberg

The National People’s Congress Standing Committee will take the first steps toward imposing anti-sanctions laws to the annexes of the charters of both Hong Kong and Macau. The move follows the NPC’s passage of an anti-sanctions law last month that gives the Chinese government broad powers to seize assets and deny visas to those who formulate or implement sanctions against the country. It also empowers individuals and companies to sue “individuals and organizations” to seek compensation for discriminatory practices in Chinese courts.

Why it Matters:

While much depends on how strictly Beijing chooses to enforce the anti-sanctions legislation, the measure could create new headaches for thousands of foreign companies that operate in the two former colonies. International banks have been dealing with increasing concerns over Hong Kong, and they now risk being caught between potentially conflicting U.S. and Chinese laws. More to come here but important to watch given the increased use of sanctions between China and Western nations.

There Can Be Only One: China’s Top Court Rules Facial Recognition Without Consent Is Illegal in Civil Cases - Caixin

China’s Supreme People’s Court on Wednesday ruled in a judicial interpretation that using facial recognition technology without consent would violate the law in civil cases, amid rising concerns about the technology’s misuse in public venues and residential compounds. The release is the country’s latest effort to protect residents’ personal information, including facial information, and punish violators, according to a statement on the ruling.

Why it Matters:

Continuing our thoughts from yesterday’s analysis section and quoting the vastly underrated Highlander movie, “there can be only one,” and his name is Xi. This is an example of a critical tech being confiscated by Beijing and banned for private use. Again, the CCP wants to look like they are protecting their citizens from greedy private sector actors only to use and sell the technology abroad to increase their own power. Expect this theme to continue to play out with AI, quantum computing, and other evolving new technologies.

LONGER-TERM THEMES:

Electrification Policy:

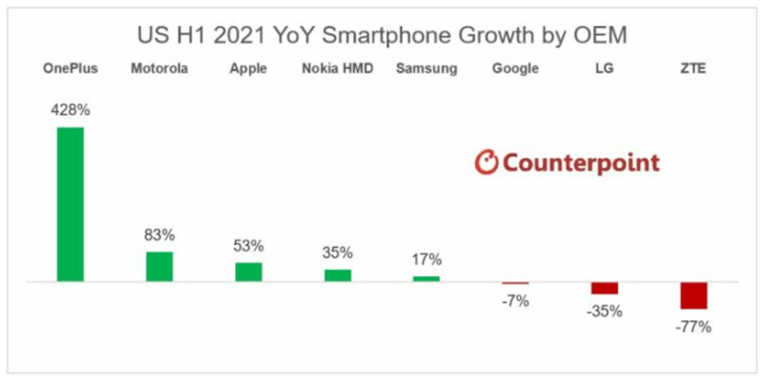

Still Growing: US Smartphone Market Grows 27% YoY in H1 2021 Despite Shortages; OnePlus, Motorola, Nokia HMD Gain as LG Exits – CounterPoint Research

The US smartphone market saw a 27% YoY increase in H1 2021 sales as carriers continued pushing 5G upgrades and heavily discounted 5G smartphones. Both Apple and Samsung devices were the top sellers in the premium segment with 53% and 17% YoY growth, respectively.

Why it Matters:

Demand is being driven by the expansion of 5G and internal changes in network use by carriers. Verizon’s purchase of Tracfone has many T-Mobile and AT&T users migrating to Verizon’s network. Verizon has committed to shutting down its CDMA network by December 2022, so the migration of users is already occurring to the new network, given the millions that will need to be moved. Although this is all happening often without users' knowledge, it is important to highlight the growth in new 5G smartphones and changing network dynamics.

ESG Monetary and Fiscal Policy Expansion:

Buy America: Biden seeks to bolster ‘Buy American’ drive ahead of Pennsylvania visit - FT

The Biden Administration is planning to sharply increase domestic content requirements for products sold to the federal government. The proposal would raise the threshold for products to qualify for the domestic content requirement currently in place. It would also help address supply chain vulnerabilities that emerged during the coronavirus pandemic, which triggered problematic bottlenecks.

Why it Matters:

In January, shortly after he took office, Biden signed an executive order to boost domestic procurement, which the new rules will build on. An administration official said the proposal would have no effect on the country’s “trade obligations,” but officials and executives from US trading partners have in the past raised concerns that “Buy American” provisions were discriminatory and aimed at cutting out international competition. The reshoring effort will be slow, methodical, and disruptive, but it is happening.