MIDDAY MACRO - 7/23/2021

Daily Color on Markets, Policy, and Geo-Politics

MIDDAY MACRO - DAILY COLOR – 7/23/2021

OVERNIGHT/MORNING RECAP & MARKET ANALYSIS

Narratives/Price Action:

Equities are higher, as positive earnings and better global data supports risk sentiment

Treasuries are lower, as the curve is steeper on the more favorable market tone

WTI is little changed, consolidating in a tight range after a three-day rally lost some momentum yesterday afternoon

Analysis:

Earnings continue to come in better than expected improving risk sentiment and propelling equities to finish the week on a positive note while Treasuries are somewhat weaker but little changed on the week overall.

The Nasdaq and S&P are outperforming the Russell with Growth, Momentum, and Low Volatility factors, and Communication, Healthcare, and Consumer Discretionary sectors are all outperforming.

S&P optionality strike levels increased with the zero gamma level moving to 4339 while the call wall remains at 4400; technical levels unchanged with support at 4340 and resistance at 4385, then 4415.

Treasuries are under some pressure but price action is somewhat muted compared to the volatility that was seen over the week with the overnight session less supportive (than normal) and traders possibly reentering steepeners (as opaque positioning seems to have cleaned up) going into next week’s plethora of econ data and FOMC meeting.

Next week brings us a number of important econ data points, the core of earnings season ($12 trillion of market cap), and a Fed FOMC meeting that will potentially shed further light on tapering intentions but likely be a balk.

On the domestic economic front, we will be eager to see if new data reinforces our 2H growth outperformance view with PCE Prices and Personal Spending, Durable Goods, New Home Sales, and Case-Shiller Home Prices, Wholesale Inventories, Richmond and Dallas Fed Manufacturing Surveys, as well as how consumer sentiment is holding up in the Michigan Consumer Report. (There’s a lot!)

The Fed will more formally “debate” when and by how much to reduce monthly Treasury and MBS purchases next week, with many members wanting a path to rate hikes in late 2022. Given the econ data water is still muddy, we don’t expect any notable change in rhetoric that may spook markets coming out of the statement or press conference.

If the data, earnings, and FOMC meeting go as we expect, momentum currently occurring will likely continue, producing a further melt-up in equities and retracement of Treasuries next week, starting to reverse the positive correlation that has been prevalent for some time, but we are approaching long-term technical resistance on the S&P and entering a more headwind filled environment in August.

Econ Data:

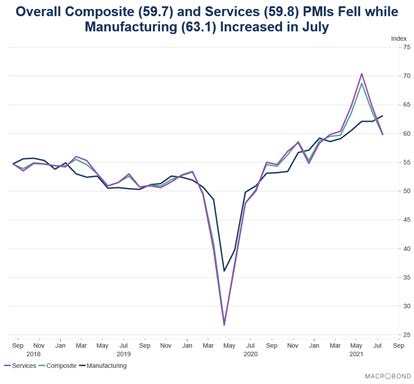

IHS Markit Composite (manufacturing and services combined) PMI Index fell to 59.7 in July from 63.7 in June. The rate of output growth was the slowest in four months. Manufacturers registered a slight acceleration in the pace of expansion in production, but service providers recorded a further loss of growth momentum amid labor shortages. Cost burdens rose robustly once again. Alongside reports of higher raw material and transportation prices, firms also noted greater wage bills as staff had to be enticed with higher pay. As a result, the rate of selling price inflation for goods and services remained historically steep in July, as firms sought to pass on higher costs to clients. The pace of increase was the third-sharpest on record.

Why it Matters: Even with the high level of supply-side disruptions not abating meaningfully, growth remains very strong. Today’s report gives us further confidence that we will experience a highly supportive domestic economic backdrop into year-end. The early stages of a more prolonged inflationary cycle are not necessarily growth negative as strong consumer demand absorbs cost increases. We believe this is exactly where we are in the cycle. We also don’t see wage increases as problematic yet and instead supportive of aggregate demand and consumer confidence after decades of capital commanding a greater share of profits over labor. This will change moving forward, but we are simply not there yet.

TECHNICALS / CHARTS

FOUR KEY MACRO HOUSE CHARTS:

Growth/Value Ratio: Growth is back in control even with more positive data and earnings generally

Chinese Iron Ore Future Price: Iron ore had one of its worst recent weeks due to increased supply and falling demand

5yr-30yr Treasury Spread: The curve is steeper on the week as positive correlations between rates and equities weaken

EUR/JPY FX Cross: Euro is higher on the week, helped by EZ PMI data beating expectations today

HOUSE THEMES / ARTICLES

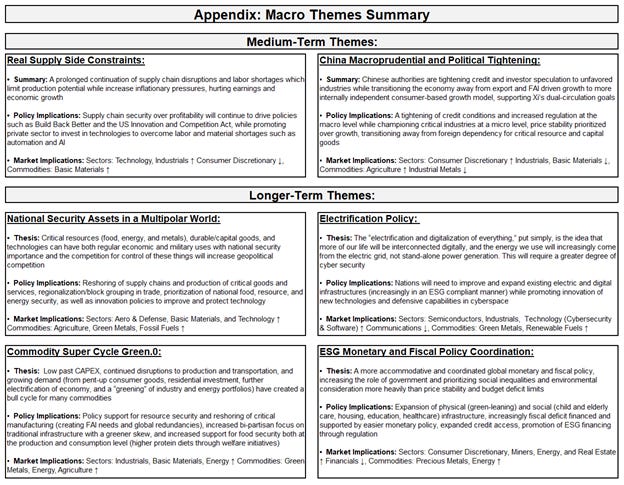

MEDIUM-TERM THEMES:

Real Supply Side Constraints:

Where is Casey Jones?: Shortage of Railroad Workers Threatens Recovery – WSJ

According to shippers and trade groups, America's freight railroads are struggling to bring back workers, contributing to a slowdown in the movement of chemicals, fertilizer, and other products that threaten to disrupt factory operations and hinder a rebound from the pandemic. Across the freight rail network, employment levels remain below pre-pandemic levels. CSX and others say they have ramped up hiring lately to handle the increased shipping demand but face the same hiring headwinds seen elsewhere.

Why it Matters:

The worker shortages are being exacerbated by congestion from products entering and exiting the rail system. Backlogs at ports mean strains on the freight railroads that are pulling cargo inland, while a tight market for trucking also creates pinch points when trains transfer containers to the highways. The bottom line, the rail part of the supply chain is likely to stay impaired and problematic for some time still.

China Macroprudential and Political Tightening:

Cyber Wolf: How China’s Hacking Entered a Reckless New Phase - Wired

On Monday, the White House joined the UK, EU, NATO, and governments from Japan to Norway in announcements that spotlighted a string of Chinese hacking operations. The US Department of Justice separately indicted four Chinese hackers, three of whom are believed to be officers of China's Ministry of State Security. These hacking activities are increasing and changing from the historical activities of IP theft, and Beijing is increasing its use of outside contractors.

Why it Matters:

"They go bigger. The number of hacks went down, but the scale went up," says Adam Segal, director of the Digital and Cyberspace Policy Program at the Council on Foreign Relations, who has long focused on China's hacking activities. The new use of contractors offers the Chinese government a layer of deniability and efficiency. However, they also lead to less control of operators and less assurance that the hackers won't use their privileges to enrich themselves on the side. All of this shows a continuation of tightening of control by Beijing on all policy fronts.

LONGER-TERM THEMES:

National Security Assets in a Multipolar World:

Unity: Record U.S. Coal Shipment to China Highlights Australia’s Pain - Bloomberg

Exports of coal in March from the U.S. to China were at their highest level since 2013. This is due to China banning coal from Australia after calling out Beijing for greater virus origination transparency. BHP Group, one of the biggest coal producers in Australia, said earlier this week that it expected the ban to remain in place for a number of years.

Why it Matters:

It’s a little disappointing that the U.S., which under Biden has developed a bilateral approach centered around its Indo-Pacific “Quad” alliance to contain China’s Wolf Warrior posturing, is profiting from the coal ban imposed on Australia. Especially since the U.S. itself has echoed Australia’s concerns over China’s cover-up of Covid’s origins. If multilateralism is to work against China, countries will have to forgo economic gains and prioritize ideology.

Electrification Policy:

Ransomware Stats: 740 ransomware victims named on data leak sites in Q2 2021: report – Zdnet

More than 700 organizations were attacked with ransomware and had their data posted to data leak sites in Q2 of 2021, representing a 47% increase compared to Q1, according to a new research report from cybersecurity firm Digital Shadows. The report notes that in the broader ransomware market, many groups disappeared or emerged out of nowhere.

Why it Matters:

Digital Shadows' Photon Research Team found that under the surface, other ransomware trends were emerging. Since the Maze ransomware group helped popularize the data leak site concept, double extortion tactics have become en vogue among groups looking to inflict maximum damage after an attack. "Ransomware operations will likely continue to operate brazenly into the third quarter of 2021, giving limited thought to who they are targeting and more to how much money they might make," the researchers wrote.

Commodity Super Cycle Green.0:

To the Last Drop: The Saudi Prince of Oil Prices Vows to Drill ‘Every Last Molecule’ - Bloomberg

“In order to force OPEC+ members to agree to significant production cuts at the dawn of the pandemic, Saudi Arabian Energy Minister Prince Abdulaziz bin Salman on March 7, 2020, ordered an increase in his country’s oil output for April. The move dramatically accelerated a price drop and precipitated negotiations that led to the deepest production cuts in history and a rebound in prices.” A truly incredible time for oil markets worth revisiting.

Why it Matters:

The article details who Saudi Energy Minister Prince Abdulaziz bin Salman is, the events of March 2020, and future plans for oil by the Kingdom. Personnel is policy, so learning about the views of the energy minister is essential. The Saudi’s currently see an opening, invest now, and capture market share. As the world moves away from oil, the Saudi's plan is to be the last supplier standing.

ESG Monetary and Fiscal Policy Expansion:

Homeowners Too: New Aid Planned for Mortgage Borrowers at Risk of Foreclosure - WSJ

New modification options will be offered for borrowers with Federal Housing Administration loans and other federally guaranteed mortgages, as the Biden Administration plans to expand assistance programs for borrowers who fell behind mortgage payments during Covid. The changes would aim to extend the length of their mortgages and lock in lower monthly principal and interest payments to keep more borrowers in their homes.

Why It Matters:

According to the mortgage-data firm Black Knight Inc, there are 1.55 million homeowners who are seriously delinquent in active forbearance. That represents about 2.9% of the 53 million active mortgages, down from a high of about 4.4% in August and September 2020. Research since the 2008-09 financial crisis has found that deferring mortgage payments, reducing interest rates or extending the term of mortgages, and thus reducing the monthly payments, are effective ways to aid homeowners short on cash. It will also reduce housing supply and expand the government's outsized role in that industry