MIDDAY MACRO - 7/20/2021

Daily Color on Markets, Policy, and Geo-Politics

MIDDAY MACRO - DAILY COLOR – 7/20/2021

OVERNIGHT/MORNING RECAP & MARKET ANALYSIS

Narratives/Price Action:

Equities are higher, as an overnight consolidation was followed by NY-open buying

Treasuries are mixed, with an overnight rally to five-month highs in the long-end reversing post-NY-open

WTI is higher, bouncing off its recent low of $65 at the NY-open

Analysis:

The S&P looks to be recapturing key levels (4300) this morning, creating the potential for a “volatility smash” (given limited optionality positional changes following yesterday’s sell-off), allowing for the resumption of the melt-up to continue as Treasury yields back up after hitting multi-month lows in early morning trading.

The Russell is outperforming the S&P and Nasdaq with Small-Cap, Momentum, and Value factors, and Financials, Industrials, and Energy sectors all outperforming.

S&P optionality strike levels changed little with the zero gamma strike level moving lower to 4334 while the call wall remains at 4400; technical levels now show support at 4280 and resistance at 4330.

Treasuries are stuck in a bit of a no-man’s land at their current levels as technicals dictate a further drop in yields and flattening of the curve while momentum looks stretched and fundamental dictate yields should be higher.

There is still a historic level of positive factors at play, allowing second-half growth (both domestically and globally) to be stronger than what is currently priced in by markets.

Although the Fed has signaled it is changing tune slowly, it will still be highly accommodative for the foreseeable future while “hard” and “social” infrastructure/fiscal spending is coming at some decent size sooner or later.

Pent-up demand from consumers supported by high net worth, savings, and credit availability is not slowing, and impairments to available supply, whether goods or services, is only pushing demand forward, not losing it.

The increased cases of the Delta variant have not meaningfully changed behavior in America. At the same time, countries such as India were able to slow the spread quickly, reducing the likelihood it is a persistent drag in the second half.

As a result, we do not see a material negative change to growth moving into year-end and question the sustainability of current price levels, specifically regarding Treasury yields and oil, which we both believe will rise.

Yes, inflation is running hot, which is detrimental to profits and ultimately growth, especially for smaller firms with less pricing power. Still, we believe the current high demand levels will allow firms to pass costs on without weakening end-demand materially in at least the next two quarters.

We also expect transitory inflationary pressures to subside before a more persistent structural pulse takes hold next year (in areas such as housing and medical care), supported by broader wage increases, allowing policymakers more time to be “patient.”

Finally, we expect the rise in the Delta variant cases globally to subside faster than expected as vaccinations continue and people’s behavior adapts to the increased risk.

As a result, yields should start trending higher, equities should see value begin to outperform again, and growth correlated commodities will resume an upward trend before a more stagflationary environment takes hold next year.

Econ Data:

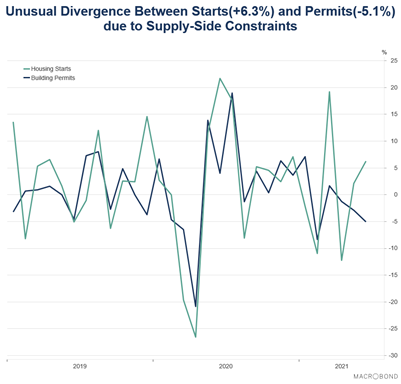

Housing starts increased 6.3% in June to 1.64 million, significantly beating expectations of a 0.8% increase. The increases were broad-based with single-family starts and multi-family starts rising 6.3% and 6.2%, respectively. Building permits, however, unexpectedly fell -5.1% to 1.60 million with a -6.3% decline in single-family permits and a -2.6% drop in multi-family permits.

Why it Matters: There continue to be numerous housing units that have been authorized but not started, which reflects the continuing challenges builders are facing in sourcing materials and labor shortages, all at elevated costs. It also gives us confidence that pandemic-related housing demand is not notably dropping. Instead, housing will continue to contribute to overall growth for some time as demand and supply mismatches work themselves out in the second half of the year.

TECHNICALS / CHARTS

FOUR KEY MACRO HOUSE CHARTS:

Growth/Value Ratio: Growth/Value is little changed on the week thanks to today’s small-cap rally

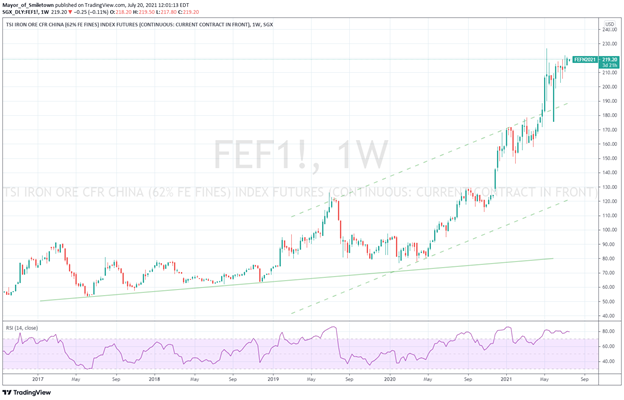

Chinese Iron Ore Future Price: Iron ore is slightly higher on the week, as low supply continues to support prices.

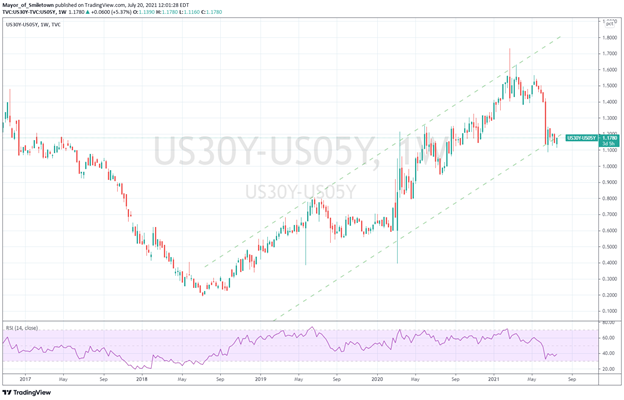

5yr-30yr Treasury Spread: Curve is steeper on the week, as 5yr Treasuries outperform today.

EUR/JPY FX Cross: Yen is higher on the week, maintaining its two-month outperformance trend.

HOUSE THEMES / ARTICLES

MEDIUM-TERM THEMES:

Real Supply Side Constraints:

Flood Disruption: Disruption caused by flooding to European railway networks – Splash247

The North Sea Mediterranean corridor has been significantly disrupted. Infrabel published an overview of the affected railway lines, many of which are part of the corridor that connects France, Belgium, the Netherlands, and ultimately the UK. The Belgian province of Liège was particularly hard hit by the floods, with many railway lines underwater or blocked by mudslides. As alternative routes do not have sufficient capacity and there will be significant delays to rail services.

Why it Matters:

Although it is still a little unclear the full effects of the flooding events, they are significant. Repairs to the damaged rail infrastructure are expected to take several weeks. As a result, we can add this to the list of global supply-chain disruptions that have continued to push up logistical costs and leaving firms short inventory.

Sustained Surge: Port Chief Sees U.S. Import Surge ‘Easily’ Lasting Into 2022 – Bloomberg

Georgia’s Port of Savannah, the largest container gateway on the East Coast after Newark, New Jersey, had its second-busiest month on record in May, following the busiest in March. The increase in activity is being helped by continued disruptions in Asia due to Covid and new impairments to rail movement out of the west due to container pile-ups in the Mid-west. There is also still an above-average wait time at the LA-Long Beach port.

Why it Matters:

It is worth highlighting that a growing number of importers are shifting operations away from west coast ports (due to continuing bottlenecks) towards east coast ones. This will help alleviate some of the problems occurring in the west and potentially improve the return to normality more generally.

LONGER-TERM THEMES:

Electrification Policy:

Bad Pegasus: Israeli Spyware Maker Is in Spotlight Amid Reports of Wide Abuses - NYT

Over the weekend, an international consortium of news outlets reported that several authoritarian governments, including Mexico, Morocco, and the United Arab Emirates used spyware developed by Israeli based NSO Group to hack into the phones of thousands of their most vocal critics, including journalists, activists, politicians, and business executives.

Why it Matters:

The new accusations heightened concerns among privacy activists that no smartphone user, even those using software like WhatsApp or Signal, is safe from governments and anyone else with the right cyber-surveillance tech. NSO denies the accusations, and the Israeli prime minister’s office declined to comment, while the Israeli Defense Ministry said it had not been given enough time to respond to a request for comment. If the hackings are true, which time will tell, it’s a disturbing development for cybersecurity.

ESG Monetary and Fiscal Policy Expansion:

Extra-Large COLA: Social Security's 2022 Benefit Hike Is Looking Bigger and Bigger – Motley Fool

Cost of living adjustment (COLA) to social security is on track to increase by 4% next year. There've only been two years since 1990 that had higher COLAs than that. For purposes of determining inflation adjustments, the key figure to watch was the CPI-W inflation index. That number moved higher by 0.9% for the second straight month in May and is 5.6% higher than it was this time last year.

Why it Matters:

High COLAs are amixed blessing for Social Security recipients. To the extent that CPI increases match up with actual higher costs for retirees, the COLA won't necessarily provide greater purchasing power. Moreover, anticipated increases in Medicare premiums could take away a portion of the raise that Social Security recipients actually see in their monthly payments. However, it's worth noting the increase as the growing number of retirees will continue to have an increasing impact on the economy.

Medical Clarity: Biden administration seeks higher penalties for hospitals that don't publish prices – The Hill

A proposal released Monday by the Centers for Medicare and Medicaid Services would raise the maximum penalty to $2 million a year for large hospitals that don't post online the secret prices they have negotiated with insurance companies for 300 standard services and procedures that can be planned in advance. Hospitals can charge vastly different amounts for the same service. Even in the same hospital, the rates can differ significantly depending on whether the patient is covered by Medicare, Medicaid, or private insurance.

Why it Matters:

This move, first proposed by the Trump administration, is an important step to bring transparency to what seems like almost criminal behavior by the medical community. In theory, it should also increase the demand for medical services for these 300 common procedures, helping reluctant consumers know the real final costs. Second, it should increase the reliability of medical care price changes in the CPI or PCE inflation measures. This sub-component is seen as more structural, having a higher weight in the eyes of policymakers, and has always been a bit of a mess to interpret.

Flood Politics: Will Flood Politics Change Germany and the World? - Bloomberg

The regions along the Rhine and its tributaries haven't seen flooding on this scale in centuries, if ever. As a result, expectations are for the Green party to gain further support in the coming September elections, as the flooding is being blamed on climate change. However, recent blunders by Green Party officials and memories of the abrupt exit from nuclear power due to Fukushima linger in many German voter's minds, making a coalition between the Christian Democrats and Greens more likely than an outright victory.

Why it Matters:

With Siberia, Finland, and the Pacific Northwest swelter under heat domes covered in purgatory-like fires while well-built split-timber houses in the Rhineland are swept from their foundations while people sleep in them, the effects of climate change have never been more evident. As a result, political parties that embrace the need to combat climate change will likely grow in popularity as things worsen. However, this increase in support will not be consistent and vary by region as measures needed to reduce carbon emissions and "green" up the economy will be costly to the everyday voter.