MIDDAY MACRO - 6/9/2021

Daily Color on Markets, Policy, and Geo-Politics

MIDDAY MACRO - DAILY COLOR – 6/9/2021

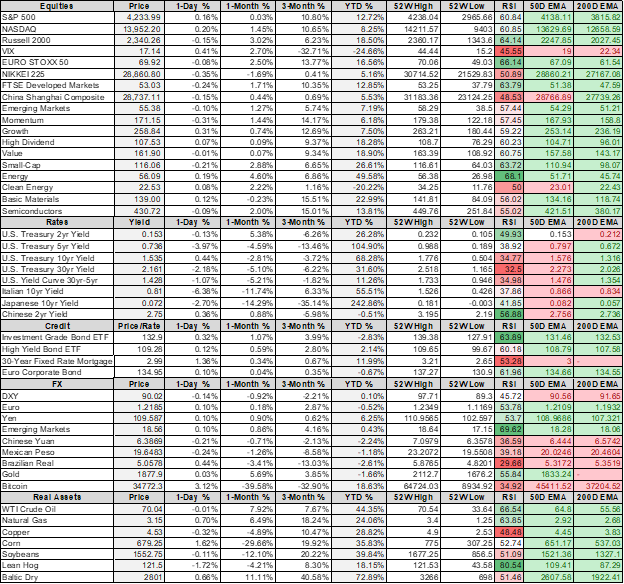

PRICE MATRIX

OVERNIGHT/MORNING RECAP & MARKET WRAP

Narratives:

Equities are slightly higher, with Nasdaq leading thanks to lower yields

Treasuries are higher, but off pre-NY-open highs

WTI is flat, hitting a +$70 high overnight but cooling following this morning’s EIA inventory data

Price Action:

S&P pushing at the higher end of its recent range

Nasdaq outperforming S&P/Russell

Low Volatility, Growth, and High Dividend Yield factors outperforming

Health Care, Technology, and Communication sectors outperforming

Zero Gamma Level is 4188 while Call Wall is 4250, technical levels have support at 4200 while resistance is at 4240, 4270

Major Asian indexes are mixed: Japan -0.4%. Hong Kong -0.1%. China +0.3%. India -0.6%.

European bourses are lower, at midday, London -0.5%. Paris flat. Frankfurt -0.5%.

Treasuries higher with the curve bull flattening

5yr = 0.74%,10yr = 1.49%, 30yr = 2.17%

10yr Treasuries bounced off a key technical resistance level of 1.47%

WTI flat to $70

EIA reported a large build in Cushing and products, with gasoline stocks at their second seasonally highest levels ever, lower than only 2020 levels

Copper lower by -0.7% to $4.52

Markets are waiting for the results of the Peruvian elections, with Socialist candidate Pedro Castillo seeming to be in the lead

Aggs are mixed but generally lower across the complex

WASDE report tomorrow will highlight if Chinese exports can continue at the current historically high-level pace

DXY flat at 90.10

Gold flat at $1895

Bitcoin higher by 8.7% to $35.7K

Econ Data:

Chinese PPI and CPI: China’s producer price index added 9% in May, its biggest year-on-year increase since September 2008 and higher than economists’ forecasts. Chinese PPI has been pushed higher by commodities and raw materials, which form a core part of the index. NBS data showed that prices in the ferrous metal smelting industry rose 38% YoY, while those for coal mining added 30%. Consumer prices in China rose 1.3% YoY in May, the most since September, but fell 0.2 % month on month.

Why it Matters: Chinese producers are being slow to pass on cost increases to end consumers. This is in contrast to what we are beginning to see in the U.S. and reflects the effects of a more centralized economy, given Beijing has been vocal about fighting inflation.

Analysis:

All eyes on the rally in Treasuries as they tried to break out of recent ranges this morning.

Further decreases in yields support our view that we should see a final melt-up in equities before a more volatile period into year-end.

Over the last few sessions, the rally in Treasuries has been less about lower growth expectations and more about technical buying factors forcing short positions to cover as key price levels were hit.

Banks with low loan demand and flush with cash have been significant buyers.

Pensions are better funded, increasing their long-end demand.

Asian buyers have been eager to pick up the extra yield as FX hedging costs have fallen.

Lower levels of volatility are allowing U.S. asset managers to pick up carry in the belly of the curve.

The Fed continues to purchase $120 billion every month.

Finally, turning to our never-ending inflation focus, last week’s jobs report showed a larger-than-forecast pickup in average hourly wages for a second straight month, raising the prospect that a wage-price spiral is beginning to take root.

However, there is still a reluctance by many to believe this is starting, especially among Federal Reserve officials, as best seen by a recent paper from the Atlanta Fed highlighting that the most substantial wage increases are coming from the low-wage service occupations.

The problem is that anecdotal evidence is beginning to show that wage increases are coming to higher-wage sectors after stagnating during the pandemic.

The majority of higher-level service sectors (trade & transportation, information, financial, and professional business services) did not experience the expected level of revenue and productivity losses during the pandemic while suspending increases in wages.

Higher skilled wages will need to catch up after a year of tepid growth due to pandemic uncertainty and we expect this to be confirmed by the data moving into year-end.

Today's two main takeaways are that the Treasury market has become detached from growth and inflation expectations while wage increases are just beginning to work their way to higher-skilled workers.

TECHNICALS / CHARTS

FOUR KEY MACRO HOUSE CHARTS:

Growth/Value Ratio: Growth Outperforming on the Week

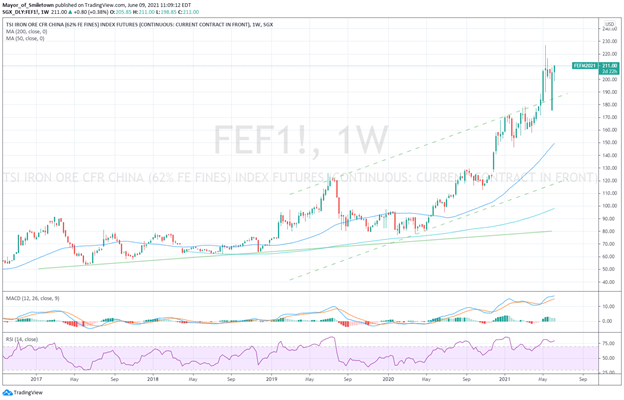

Chinese Iron Ore Future Price: Iron Ore Higher on the Week

5yr-30yr Treasury Spread: Curve is Steeper on the Week

EUR/JPY FX Cross: Euro Higher on the Week

HOUSE THEMES / ARTICLES

MEDIUM-TERM THEMES:

Real Supply Side Constraints:

Slow Seas: Top U.S. Maritime Regulator Sees Shipping Snarls Lasting to 2022 - BBG

The top U.S. maritime regulator said stretched global supply chains pushing ocean-freight rates to record highs may stay strained into 2022, raising concerns about whether small American companies can weather another year of a tangled transport system and much higher costs. The supply snarls are colliding with a surge in demand for goods as the world’s largest economy heads for peak shipping season in July and August when retailers build inventories heading into the year-end holidays.

Why it Matters:

The system is at or beyond its capacity, pretty much everywhere in the world. Container carriers that struggled for most of the past decade with overcapacity and losses face the opposite now: almost no slack to meet all the demand and soaring profits because they’re able to charge three and four times the pre-pandemic cargo rates. Finally, this is just another area of the currently impaired logistical industry telling us the problem will last longer than expected.

China Macroprudential and Political Tightening:

Tech Crackdown: China’s Tech Clampdown Is Spreading Like Wildfire – WSJ

China’s internet-technology sector continues to be hurt from what began as a crackdown on anti-competitive practices but has since become a broader effort to clean up the sector, spanning issues such as data usage and employment practices. The clampdown could result in slower revenue growth and lower profit margins, said Thomas Gatley, an analyst at Gavekal.

Why it Matters:

China has one of the thinnest histories of antitrust regulation among major global economies and has historically used antimonopoly rules to curb the market influence of foreign firms. Domestic internet companies were largely left alone as China sought to nurture its own tech industry. This recent change in attitude toward the tech industry shows Xi’s continues to consolidate power and reign in the tech-princelings, showing them that Beijing is in charge.

LONGER-TERM THEMES:

National Security Assets in a Multipolar World:

Moves and Counter-moves: China unveils new legal weapon to hit the United States and other Western rivals with tougher sanctions - SCMP

China’s top legislative body is set to pass a new anti-sanctions law on Thursday, giving substantive legal backing and protection to the country’s retaliatory measures against punitive actions by Western governments on Chinese officials and companies. “Now the international situation is getting more and more critical, and the US often deviates from international law in dealing with China,” Song said. “I believe that the new law will allow Beijing to hit back, regardless of whether its rivals are following international law or not.”

Why it Matters:

The new rules expand China’s toolbox of countermeasures to address actions that impact Chinese companies' trade and economic activity. These measures, if implemented broadly, could significantly impact how companies operate between the United States and China. We will wait to see the final law before further assessing the impact.

Coal: China’s coal shortage may lead to more power rationing - Argus

State-owned energy producers are being told by local energy regulators to monitor electricity consumption and focus on increasing renewable energy output to counter a worsening power supply crunch. Authorities did not address the crucial issue of raising coal supplies to ease the electricity shortfall. Meanwhile, Beijing's informal ban on Australian coal has given non-Australian producers significant leverage to raise prices.

Why it Matters:

Chinese coal importers may soon run out of options due to limited seaborne cargoes from alternative coal-exporting countries in the absence of Australian coal and competition for supplies from buyers in other northeast Asian countries. Without increased domestic production or alternative sources of energy sourcing, Beijing’s resolve to punish Australia will be tested as further outages will likely worsen over the hotter summer months while prices only go higher.

Electrification Policy:

Privacy Law: Colorado Legislature Advances Legislation to Protect the Privacy of Consumers – Consumer Report

Colorado legislature approved privacy legislation that would give residents the right to access, delete, and stop the sale of their personal information, with additional protections for sensitive data. Colorado is the third state to advance comprehensive privacy legislation, after California and Virginia.

Why it Matters:

While the U.S. Congress has stalled in introducing a comprehensive privacy law, over a dozen states have considered legislation similar to the California Consumer Privacy Act. Legislatures in New York, Massachusetts, and Connecticut have pending privacy bills. Any more extensive restrictions to the use of personal data will change the business model of numerous tech firms.

Search Commodity: Ohio sues Google, seeks declaration of tech giant as a public utility - AP

Ohio Attorney General Dave Yost filed a lawsuit Tuesday asking a court to declare Google a public utility and to regulate it as one. While the lawsuit is not seeking monetary damages, it asks the court to require Google “to offer sources or competitors rights equal to its own,” meaning the company should not prioritize the placement of Google-owned products, services, and websites on its search results.

Why it Matters:

The complaint is just the latest in a series of legal threats the tech giant is facing both in the U.S. and abroad, including a multi-state antitrust lawsuit assailing Google's business practices. Tech regulation and taxation is a longer-term theme that will negatively affect risk-assets given techs' large footprint. Attempts to classify a private firm as a utility shows the length various parties will go to in their attempt to reign in big techs power.

Commodity Super Cycle Green.0:

Low CAPEX: A Commodities Crunch Caused by Stingy Capital Spending Has No Quick Fix – WSJ

Languishing commodity prices led producers to slash capital spending on major resources by nearly half over the last decade, shrinking stocks of industrial metals to two-decade lows and reducing supplies across commodities. Since 2011, investments to develop the energy and mining sectors have fallen 40%, according to asset manager Schroders.

Why it Matters:

The consequences of underdeveloped global resources now stoke worries that producer price inflation, buoyed by demand projections that in critical materials stretch decades ahead, is becoming sufficiently broad and prolonged that it spills onto consumer prices. Readers of this daily will not be surprised by inflation worries seen in this article, and it is being highlighted to show the view is now becoming more consensus.