MIDDAY MACRO - 6/7/2021

Daily Color on Markets, Policy, and Geo-Politics

MIDDAY MACRO - DAILY COLOR – 6/7/2021

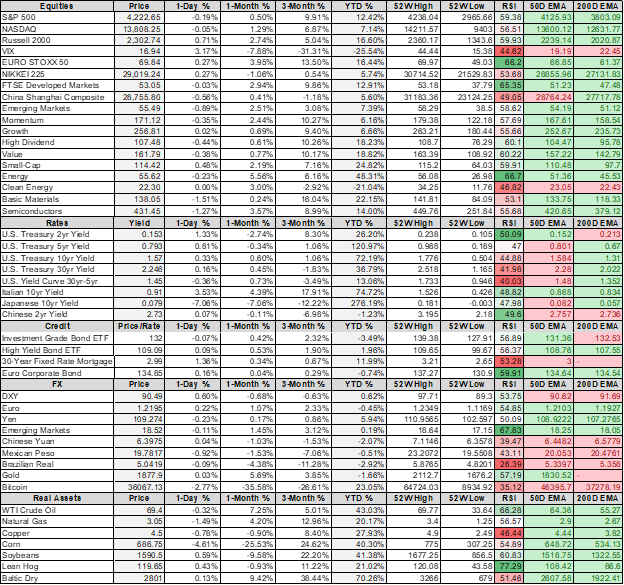

PRICE MATRIX:

OVERNIGHT/MORNING RECAP & MARKET WRAP

NARRATIVES:

Equities are mixed, with Russell rallying at NY-open while S&P and Nasdaq drift sideways

Treasuries flat, as markets begin to focus on supply coming later in the week

WTI is lower, after touching on $70 overnight with little new news

PRICE ACTION:

Equities are quiet, with S&P near recent highs but still range-bound

Russell outperforming S&P/Nasdaq

Small-Cap, Growth, and Low Volatility factors outperforming

Real Estate, Healthcare, and Utilities sectors outperforming

Gamma gravity is 4200 while Call Wall is 4275, technical levels remain the same with support at 4195 while resistance is at 4230

Major Asian indexes are mixed: Japan +0.3%. Hong Kong -0.3%. China +0.2%. India +0.4%.

European bourses are higher, at midday, London +0.2%. Paris +0.1%. Frankfurt flat.

Treasuries flat with the curve slightly flatter

5yr = 0.79%,10yr = 1.57%, 30yr = 2.24%

WTI lower by -0.7% to $69.15

Copper lower by -1% to $4.53

Aggs are flat/lower across the complex, giving back significant overnight gains at NY-open

DXY lower to 90

Gold higher by 0.2% to $1895

Bitcoin lower by -2.5% to $36K

ANALYSIS:

No significant new developments over the weekend and during the overnight have equities and Treasuries little changed at the NY-open as they both continue to stay within recent ranges.

Important to watch how the Treasury supply is absorbed this week.

3, 10, 30-year auctions will help markets gauge demand along the curve.

Internal rotation in equities continues as higher-yielding sectors outperform while reflation trade favorites cool.

Notable that small-cap growth is outperforming small-cap value today.

Major data releases to watch this week in the U.S. include:

NFIB Business Optimism will gauge if cost increases and labor constraints continue to weigh on business output and outlook.

We believe both will continue to be problematic throughout the summer.

JOLTs Job-Opening data will give insight into the continued mismatch of unemployed and openings, as well as whether there is a further increase in the quits rate.

We believe JOLTS will reinforce what was seen in the jobs report Friday, a more selective labor pool with greater bargaining power.

Inflation data Thursday will further reveal how much of the cost increases being experienced by producers are beginning to be passed on to end consumers.

Consensus expectations for MoM increases in core inflation are 0.5% (0.9% last month), which we believe are too low.

Finally, the monthly USDA WASDE report will also be released Thursday, giving insight into crop demand/supply.

Given the level of price increases to date and concerns over China’s continuing demand for U.S. imports, this report will be more critical than usual.

TECHNICALS / CHARTS

FOUR KEY MACRO HOUSE CHARTS:

Growth/Value Ratio: Growth Outperforming on the Week

Chinese Iron Ore Future Price: Iron Ore Lower on the Week

5yr-30yr Treasury Spread: Curve is Steeper on the Week

EUR/JPY FX Cross: Euro Lower on the Week

Dow Transports:

Dow Jones Transportation Average Index has been bull flagging since the beginning of May, breaking below its tactical uptrend last week.

$IYT is still in its March ’20 long-term uptrend.

The daily RSI and MACD are trending lower.

Although we give limited support to Dow Theory, transports are worth watching here.

A break down below the 50DMA could see price challenge the lower support of the current bull flag channel.

Industrials are still looking technically sound, but transports will need to catch up for the market to continue to advance.

HOUSE THEMES / ARTICLES

MEDIUM-TERM THEMES:

Real Supply Side Constraints:

Chips: Chip shortage to last until at least mid-2022, warns manufacturer - FT

Singapore-based Flex, which sits at the heart of the supply chains for the car, medical devices, and consumer electronics industries, said that the manufacturers it relies on for semiconductors have pushed back their forecasts for when the shortage will end. Electronics manufacturers in Asia have also recently warned that the chip shortages were beginning to spread to TVs, smartphones, and home appliances, with the situation made worse through stockpiling by Chinese groups hit by sanctions.

Why it Matters:

Seemingly minor problems can have outsized effects on semiconductor supply chains already under pressure. For example, a recent two-week lockdown in Malaysia, where many semiconductor suppliers are based, is again delaying production. Bottom line, chipmakers are investing in new production capabilities and have begun prioritizing regionalization, but the supply shortages will continue for some time.

LONGER-TERM THEMES:

National Security Assets in a Multipolar World:

Among the 11 newly-added entities on Biden’s new executive order (prohibiting Americans from investing in Chinese companies) were Proven Glory Capital Ltd and Proven Honour Capital Ltd, two dollar bond issuers for Huawei. While Huawei remains a privately-owned company, it has four outstanding dollar bonds (with a total value of $4.5 billion) held by many big overseas financial firms, including funds managed by BlackRock Inc and AXA.

Why it Matters:

Restrictions on US-based investors and US citizens could affect nearly US$60 billion worth of bonds, according to a recent report by JP Morgan. Besides Huawei, at least 10 of the companies included in the list have subsidiaries that have issued dollar bonds, including chip giant Semiconductor Manufacturing International Corp (SMIC) and the Aviation Industry Corporation of China. It is likely the Biden Administration would expand its use of capital market sanctions. Still, ultimately this will only have a limited effect on slowing China’s ability to fund its military build-up.

Fudan: Hungary: Plan to build Chinese university branch protested – Washington Post

An agreement between Hungary and Shanghai-based Fudan University calls for a Budapest campus to be completed by 2024, representing the school’s only foreign outpost and the first Chinese university campus in the 27-nation European Union. Hungarian officials have insisted that Fudan, ranked among the top 100 universities globally, will help raise higher education standards in Hungary. But the university’s links to China’s Communist Party have sparked outrage among liberal-minded Hungarians.

Why it Matters:

Two things of importance here; Orban, a right-wing populist, has fostered closer ties with Russia and China. He faces European Union criticism for his authoritarian ways and staunch anti-immigration stand. Second, the U.S. continues to pressure universities to close their Confucius Institutes. The institutes are seen as a way the CCP advances its state agenda by recruiting and control of academic staff, in the choice of curriculum, and in the restriction of debate.

Electrification Policy:

Legal Tender: El Salvador Plans Bill to Adopt Bitcoin As Legal Tender - BBG

President Bukele believes bitcoin will help improve financial inclusion, fight corruption, and facilitate faster transfers for around $6 billion of remittances a year. El Salvador’s bonds tumbled last month after Bukele’s party used the supermajority it won in February congressional elections to fire five top judges and the attorney general. This is likely also motivating the move to crypto as international investors and organizations question his intentions and reduce support.

Why it Matters:

In theory, financial inclusion and cheaper and more efficient forms of cross-border capital transfers all sound nice and get to the core of the attraction blockchain and crypto present. Unfortunately, as we frequently highlight here, Bitcoin is an inferior technology for transactions, is not environmentally friendly, supports tax fraud and criminal organizations. Hence, we still see crypto as far from being a legitimate replacement to the existing financial system in its current form.

Commodity Super Cycle Green.0:

BioFuels: Renewable-Fuel Push Drives Soyoil Prices to Record High - WSJ

The USDA expects the biofuels sector to consume almost 30% more soyoil this year than last, causing prices to soar by 70% this year. Production capacity this year for soyoil in the U.S. is expected to double from where it was last year. Global supply issues are also a factor pushing vegetable oil prices higher. In Southeast Asia, coronavirus-related labor shortages have reduced palm oil production, an oil used for similar purposes.

Why it Matters:

Companies such as ADM, Cargill, and major oil companies are all investing in expanding the production of biofuels, with much of their focus on soy oil. New entrants in the market site their need to secure supply chains and diversify into renewable fuels. There is also concern alternatives like palm oil are more environmentally destructive, potentially leading consumers to prioritize soyoil.

Hydrogen: Renault, Plug Power Venture to Make Hydrogen Vans This Year - BBG

The venture, now named Hyvia, plans to begin building three types of fuel-cell vans at existing Renault plants in France by year’s end. Fuel-cell vehicles produce no greenhouse gas emissions, and they can refuel far faster than an electric vehicle can recharge its battery pack. Fuel-cell vehicles are also lighter than their battery-electric competitors, a distinct advantage for delivery vans and trucks.

Why it Matters:

Certain renewable energy technologies will have clear applicational advantages over others, such as hydrogen for delivery vehicles. This indicates that there will be a need for an overlapping network of support infrastructure, increasing private and public capital expenditures to build the needed infrastructure. For example, Hyvia, on top of producing vans, will also supply customers with hydrogen to run the vans and charging stations for delivering the hydrogen.

ESG Monetary and Fiscal Policy Expansion:

GMT: Finance Leaders Reach Global Tax Deal Aimed at Ending Profit Shifting –

Finance leaders from the Group of 7 countries agreed to back a new global minimum tax rate of at least 15 percent that companies would have to pay based on where sales and service occurred regardless of where they locate their headquarters. Next month, the Group of 7 countries must sell the concept to finance ministers from the broader Group of 20 nations meeting in Italy. If that is successful, officials hope that a final deal can be signed by the Group of 20 leaders when they reconvene in October.

Why it Matters:

To state the obvious, any deal among G20 members on global tax rates could have far-reaching consequences to various industries, firms, and currencies. The deal would likely standardize how digital taxes work globally, altering tax bills for big tech. IT could also encourage repatriation of overseas profits and increase capital allocation to shareholders. It will be important to continue to watch developments here and gauge winners and losers.