MIDDAY MACRO - 6/4/2021

Daily Color on Markets, Policy, and Geo-Politics

MIDDAY MACRO - DAILY COLOR – 6/4/2021

PRICE MATRIX

OVERNIGHT/MORNING RECAP & MARKET WRAP

Narratives:

Equities are higher, as the jobs data was seen as a positive for duration sensitive sectors

Treasuries higher, following some initial confusion over how to interpret a headline NFP miss versus increased wage growth

WTI is higher, continuing to grind towards $70 on little new news

Price Action:

Equities were flat overnight, bouncing significantly following the jobs report

Nasdaq outperforming S&P/Russell

Growth, Low Volatility, and Momentum factors outperforming

Technology, Communications, and Healthcare sectors outperforming

Gamma gravity is 4200 while Call Wall remains at 4250, technical levels remain the same with support at 4195 while resistance is at 4225

Major Asian indexes are mixed: Japan -0.4%. Hong Kong -0.1%. China +0.2%. India +0.3%

European bourses are lower, at midday: London -0.3%. Paris -0.1%. Frankfurt flat

Treasuries are higher with the curve bull flattening

5yr = 0.78%,10yr = 1.56%, 30yr = 2.24%

WTI is higher by 0.7% to $69.30

Copper is higher by 1.5%to $4.53

Aggs are higher across the complex

USDA export sale numbers were better than expected

DXY is lower, reversing yesterday’s gains post jobs data to 90.1

Gold is higher by -1.1% to $1895

Bitcoin is lower by -4% to $37.1K

Econ Data:

Job Numbers: Nonfarm payrolls rose by less than forecast, increasing only 559,000 in May. Total payroll gains in the prior two months were revised up by a negligible 27,000. Leisure and hospitality jobs rose 292,000, while employment in the construction and retail sectors fell. The unemployment rate fell to 5.8% from 6.1% (3.5% in February 2020), while the participation rate declined 0.1% point to 61.6% (63.3% in February 2020), and the U6 underemployment rate fell to 10.2% from 10.4% (7.0% in February 2020). Payrolls remain 7.6 million below February 2020, which represents only a 21% closing of the gap.

Why it Matters: Labor supply constraint problems were on full display with labor force participation basically unchanged (since October) helping average hourly wages to increase 0.5% on the month. This further emboldens our view that constraints on production and inflationary pressures will be longer-lasting and more negative to growth than markets have priced in.

Policy Talk:

NY Fed President Williams: Remarks from Williams yesterday reinforced the core theme among the doves that the economy has improved, but it is still far from time to adjust policy. “We’re still quite a way off from reaching the ‘substantial further progress’ that we’re really looking for, in terms of adjustments to our purchases,” Williams said Thursday in a Yahoo! Finance interview. “That said, we have to be thinking ahead, planning ahead, and so I do think it makes sense for us to be thinking through the various options that we may have in the future – talking about talking about how the economy is doing, where we see it going, and understanding how that may play out over the coming months,” he said.

Why it Matters: Following similar comments from other dovish leaning Fed officials this week, Williams acknowledged that the conversation to begin removing accommodative policy will be fully starting over the summer.

Analysis:

What a pickle we are getting into, as even with payrolls still 7.6 million below pre-pandemic levels, wage pressures are ramping up, completing the trifecta of inflationary pressures we have discussed here at nausea.

The sustainability of demand-pull and supply-push inflationary pressures has historically been dependent on the degree of wage-spiral inflation, which is now increasing.

These inflationary pressures have resulted and will continue to be supported by the unprecedented coordination between fiscal and monetary policy.

Sound familiar? A combination of cyclical and structural demand-pull and cost-push inflationary pressures led to a wage-spiral inflationary feedback loop in the ‘60s & ‘70s.

Increases in the governments' social safety net (introduction of Medicare and Medicaid) and the passage of the Humphrey-Hawkins Act showed a significant alignment of monetary and fiscal policy at the time.

Hmm, that does sound familiar... Currently, fiscal policy is delivering; long-lasting pandemic recovery policies, infrastructure and China/reshoring bills, the potential for expansion of child and elderly care (later this year), and increased environmentalism, all likely deficit-financed, while the Fed’s new long-term goals increase their focus on fighting labor inequalities.

But we have always had deflation, so this time must be different? The only difference is no one remembers inflation, and we have been programmed to believe that technology, globalization, and demographics are all deflationary, but (and for another time) these factors are changing to become more inflationary.

Fed officials are still happy to let things run hot, slowly acknowledging the improvement in the economy but still gravitating to a cautious view focused on inequalities in labor and academic approaches to think about price pressures.

Some hope recently came from Kaplan and Bullard, who highlighted that labor market conditions are tighter than the jobs data suggests, but they remain outliers.

The next step up in labor market conditions will occur this fall when the participation rate sees some relief as children return to school (allowing stuck-at-home parents to rejoin the workforce) and extra unemployment benefits finally finish.

The improvement in overall labor conditions at this time will coincide with increasing structural inflationary factors (such as owners' equivalent rent and wages) and a growing likelihood that “transitory” factors have yet to meaningful dissipate.

At this point, the Fed will have a much harder time convincing markets it will continue to remain patient, and expectation for the duration of tapering and the beginning of rate hikes will materially move forward.

Although none of the above means risk assets or Treasuries need to drastically change today (as we are seeing with both higher post-NFP), it does increase the probability that, as we enter the end of the year, we will see higher levels of volatility across assets that continue to remain positively correlated.

TECHNICALS / CHARTS

FOUR KEY MACRO HOUSE CHARTS:

Growth/Value Ratio: Value Outperforming on the Week

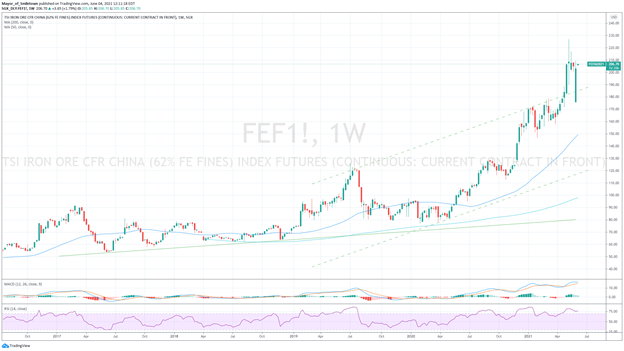

Chinese Iron Ore Future Price: Iron Ore Higher on the Week

5yr-30yr Treasury Spread: Curve is Flatter on the Week

EUR/JPY FX Cross: Yen Higher on the Week

HOUSE THEMES / ARTICLES

MEDIUM-TERM THEMES:

Real Supply Side Constraints:

Chinese Port Problems: Yantian congestion pushes box spot rates to new highs, ceiling still not in sight – Splash247.com

Hobbled by growing congestion at Chinese export gateway Yantian and key receiving terminals such as Oakland and Hamburg, the Shanghai Containerized Freight Index shot up by another 3.3% today to hit new records. The box spot index operated by the Shanghai Shipping Exchange is up 157% year-on-year. “There aren’t currently any barriers preventing rates from continuing their ascent,” said Simon Heaney, senior manager of container research at UK consultant Drewry. “Demand is still surging and port productivity and equipment availability are worsening. Unless those conditions change – we don’t think they will until 4Q21 at the earliest – then prices will go up and up.”

Why it Matters:

Insufficient capacity will likely remain a problem for the remainder of the year, continuing to put price pressure on shipping rates. This is on top of the continued price pressures seen throughout the rest of the end-to-end logistical process, such as warehousing, and trucking. These price increases will increasingly be passed through to the end consumer, adding to an increasing inflationary mindset.

LONGER-TERM THEMES:

National Security Assets in a Unipolar to Multipolar World:

Coal Wars: Australia exports record-high thermal coal to India - Argus

Australia's thermal coal exports in April increased by 14% from the eight-year low in March thanks to high volumes to India but is still 7% below last year’s level. There were no shipments to China for the fourth consecutive month, with initial shipping data suggesting this continues into early June. The decline in exports to China has been partially offset by increased shipments to India, South Korea, Taiwan, and Japan.

Why it Matters:

The ability of Australian exporters to diversify away from China is important in several ways. It limits the political influence China can have on Australian politics and it shows other nations/industries that rely on China’s domestic markets that they are not the only source of demand. Remember, the ban on Chinese thermal coal imports was due to the questioning of the origins of Covid by the Australian PM, a question now echoed by the Biden administration.

Electrification, Digitalization, and Cyber Security:

Crypto Tracking: U.S. Looks Into Cryptocurrency’s Role in Ransomware Hacks – WSJ

In a letter to business leaders Wednesday, Deputy National Security Adviser Anne Neuberger said U.S. officials are working with international partners on consistent policies for when to pay ransoms and how to trace them. This is coming as part of a larger “National Security Study Memorandum on the Fight Against Corruption”, released yesterday.

Why it Matters:

The Biden Administration is prioritizing the “fight against corruption” and directly linking cryptocurrencies as enablers of this corruption. The new executive order comes following the increased focus on fighting ransomware attacks as well as increased funding for the IRS to crack down on tax evasion, both of which negatively use crypto. This all points to a further crackdown on the crypto space by this administration.

Green Energy and Resource Transition:

Green Hydrogen: World’s first multimodal hydrogen refueling station opens in Antwerp – Splash247.com

CMB.TECH, the innovation arm of the Saverys shipping empire, opened the world’s first multimodal green hydrogen refueling station in Antwerp. The station produces hydrogen from water and green electricity with a 1.2MW electrolyzer. In addition to the hydrogen refueling station, CMB.TECH has also launched the first dual-fuel truck running on hydrogen.

Why it Matters:

CMB predicts that ports will be ideal locations for the use of hydrogen due to a concentration of applications difficult to electrified and access to hydrogen and large electrolysis plants. We highlight this development just as another milestone worth watching. The race between hydrogen, ammonium, and biofuels will likely never end in a total winner but instead a world of overlapping and varying “green” energy storage alternatives.

Commodity Super Cycle 3.0:

Where is the Rain?: Worst Drought in Decades Escalates Threats Across U.S. West - BBG

Almost three-quarters of the West is gripped by drought so severe it's off the charts of anything recorded in the 20-year history of the U.S. Drought Monitor. The region saw little precipitation, robbing reservoirs of dearly needed snowmelt and rain. Through the end of April, 1.7 million acre-feet of water melted off California's mountains, down from the normal rate of 8 million.

Why it Matters:

The parched conditions mean the wildfire threat is high and farmers are struggling to irrigate crops. With food prices already on the rise and California a chief producer of many specific crops, there will be additional inflationary pressures coming. The increased occurrences of wildfires could further shake confidence in our infrastructure and utility industry, potentially increasing the likelihood of a bipartisan bill there.

Mine Waste: Copper Boom Has BHP, Freeport Picking Through Waste – WSJ

BHP and Freeport-McMoRan have invested in Jetti Resources, a company that specializes in extracting copper out of mine waste. Jetti can quickly produce copper from abandoned earth where the ore was originally unprofitable to process. Since a mine can take 10 years to develop this approach has the potential to increase supply quickly given miner expected global copper demand to double over the next 30 years.

Why it Matters:

Jetti estimates there are around 234 million metric tons ($2.4 trillion at current price) of this so-called contained copper its technology makes extracting copper from mine waste commercially viable for the first time. New mining technologies that target the ocean or arctic, recycling initiatives, and in this case, reapproaching leftover mining waste will all be crucial in meeting future demand for copper.