MIDDAY MACRO - 6/24/2021

Daily Color on Markets, Policy, and Geo-Politics

MIDDAY MACRO - DAILY COLOR – 6/24/2021

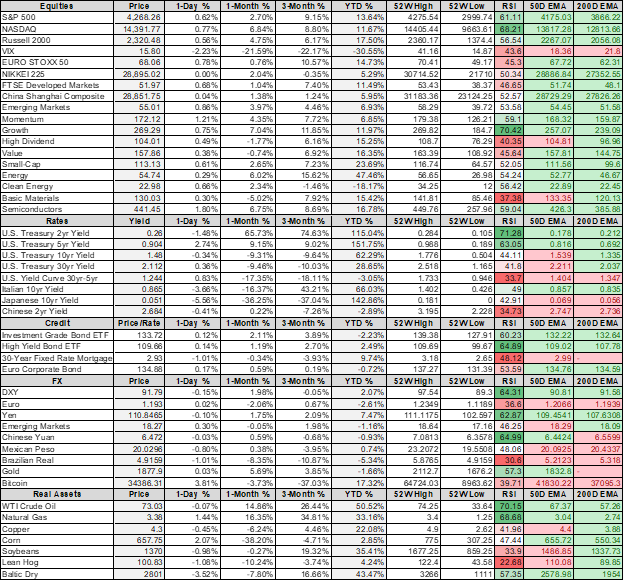

PRICE MATRIX

OVERNIGHT/MORNING RECAP & MARKET WRAP

Narratives:

Equities are higher, with the expected summer melt-up gaining transaction

Treasuries are mixed, eerily quiet as the curve slightly flattens

WTI is flat, bouncing at the NY-open after pre-open selling

Price Action:

Equities rallying with all sectors higher other than Real Estate

Nasdaq outperforming S&P/Russell

Momentum, Growth, and Low Volatility factors outperforming

Communication, Healthcare, and Technology sectors outperforming

Zero Gamma Level is 4209 while Call Wall is 4275, technical levels have support at 4222 while resistance is at 4270

Major Asian indexes are higher: Japan flat. Hong Kong +0.3%. China flat. India +0.8%.

European bourses are higher, at midday, London +0.3%. Paris +1%. Frankfurt +0.8%.

Treasuries higher with the curve flattening

5yr = 0.90%,10yr = 1.48%, 30yr = 2.09%

WTI higher by 0.3% to $73.40

Copper higher by 2.2% to $4.32

China announced the size of metals it is releasing from its strategic reserves, with the copper amount being equivalent to 2.4% of its average monthly production

Aggs are lower

Wetter Midwest weather forecasts and ongoing technical selling is driving the price action

DXY slightly higher by 0.1% to 91.8

Gold lower by -0.3% to $1780

Bitcoin higher by 3.2% to $33.9K

Econ Data:

Durable Goods: The headline index rose 2.3% in May, lower than expected, following a drop of -0.8% in April. New Orders were up 2.3%, their highest level since January. However, excluding transportation orders only increased 0.3% (estimates were for an increase of 0.7%). The volatile Nondefense Aircraft and Parts increased 37.4% on the month. Unfilled orders increased by 0.8%, while inventories grew at 0.7%, the same pace as last month.

Why it Matters: American industry is undoubtedly still growing despite problems with backlogged supply chains and a shortage of workers. Interestingly, “orders for nondefense capital goods excluding aircraft,” a category that tracks business investment, fell slightly by -0.1% in May after rising 2.7% in April. Firms that are flush with cash and seeing strong demand should start to increase production, but the data shows a reluctance to invest.

Policy Talk:

Atlanta Fed President Bostic: In remarks yesterday during an interview with NPR’s “Morning Edition,” Bostic highlighted that he now expects interest rates will need to rise in late 2022 due to the increase in estimated growth (to 7%) this year and inflation well above the Fed’s 2% target. “Given the upside surprise in recent data points, I pulled forward my projection,” Bostic said. He also noted, “temporary is going to be a little longer than we expected initially, rather than it being two to three months, it may be six to nine months.”

Why it Matters: Bostic is a current voter and certainly a more dovish member whose focus has been on promoting an equitable recovery, likely putting his focus more on the full employment mandate. For him to note that things are moving faster than he expected, and price pressures may last longer is a notable development for someone seen as a possible Biden Administration pick to replace Powell down the road.

Analysis:

In what looks to be more mechanical buying, equities continue the week's rally as volatility levels drop and Treasuries settle into a tighter range.

The prediction of a more volatile week, due to the reduction of gamma levels, has not come to fruition yet.

Instead, the widening of the trading range has allowed for a melt-up.

There is a significant level of strikes at 4250, which should create some gravity around current levels.

This week's abundance of Fed speakers has also reversed much of the hawkish takeaway from last week's FOMC meeting.

However, as highlighted before, many Fed officials commented on higher growth with sticker inflation than previously expected this week.

With positioning cleaner, the dollar and Treasuries are now potentially entering into new tactical ranges. At the same time, real rates have reversed some of their post-FOMC gains, all helping financial conditions ease some of the tightening that occurred last week.

We believe there could be a further rally in equities over the summer but would not chase the current rally as daily RSIs have entered overbought conditions, and gamma levels will tighten trading ranges around current price levels.

Even with Fed officials walking back the more hawkish interpretation of last week’s FOMC, the tightening cycle has started and will increasingly weigh on investor sentiment and increase volatility into year-end.

Tomorrow's PCE data will shed further light on the ongoing inflationary pulse.

If there is a significant beat, this week's range for Treasuries could quickly breakdown, and selling could spill over into equities that still have a historically high positive correlation to rates.

We expect the increases in overall inflation from supply-side disruptions to begin to slow in the following months, although not decrease.

It is doubtful this will be reflected in tomorrow's print as ISM, PMIs, and regional Fed surveys did not see any reprieve to disruptions yet.

We still very much expect more structural factors to pick up into year-end.

As a result, this could cause a head fake in inflationary expectations into the fall as “transitory” factors slow while structural ones more methodically rise.

This dynamic should support easier financial conditions temporarily as policy tightening expectations are reduced.

Finally, we are closely watching the amble levels of liquidity being withdrawn by the Fed’s Repo facility and pondering the longer-term effects on the dollar and front-end spreads more generally, but acknowledge these developments have yet to translate into significant changes in behavior by yield seekers there.

TECHNICALS / CHARTS

FOUR KEY MACRO HOUSE CHARTS:

Growth/Value Ratio: Growth Outperforming on the Week

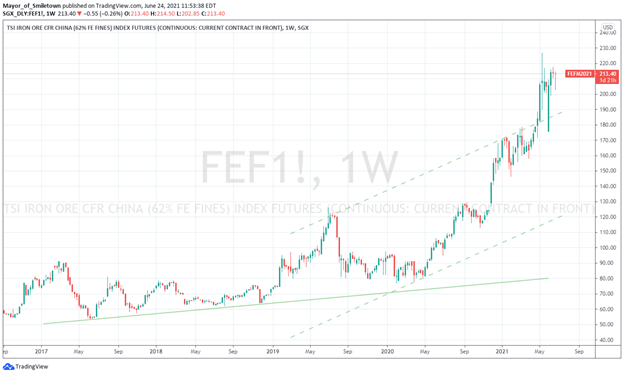

Chinese Iron Ore Future Price: Iron Ore Lower on the Week

5yr-30yr Treasury Spread: Curve is Steeper on the Week

EUR/JPY FX Cross: Euro Higher on the Week

HOUSE THEMES / ARTICLES

MEDIUM-TERM THEMES:

Real Supply Side Constraints:

Dude, Where's My Car?: North America lost vehicle estimates grows: AutoForecast - Argus

Estimates of lost vehicle production rose this week by 15% to 865,000 vehicles, 110,000 more vehicles than the prior week, according to data from AutoForecast Solutions. The number of vehicles deemed "at-risk" also increased, rising by a third to 293,000 vehicles. The increased lost production comes as Ford and GM were able to bring some production back in June.

Why it Matters:

Recent regional Fed surveys, PMIs, and ISM data reports, as well as continued industrial and firm reports, all continue to show production and revenue growth being constrained by supply-side impairments. Although we have been predicting this for some time, it is now important to continually monitor it as the duration of the constraints will be vital in maintaining the initial inflationary pulse we see from cost-push dynamics.

China Macroprudential and Political Tightening:

Changing Course?: China Boosts Short-Term Cash Injection to Ease Liquidity Worries – Bloomberg

The injection of 30 billion yuan ($4.6 billion) marked an end to the People’s Bank of China’s practice of adding 10 billion yuan each trading day for the past three months. The move bodes well for liquidity prospects in the second half, as some 4.15 trillion yuan of medium-term policy loans will mature by December. “The market now believes that they know the PBOC’s cards -- it will keep liquidity reasonable for the remainder of the year,” said Wan Kelin, an analyst at Topsperity Securities.

Why it Matters:

China’s overnight borrowing costs posted the largest one-day decline in almost three months as PBOC’s injection eased money-market jitters fueled by quarter-end regulatory checks on banks and the issuance of local government bonds. The move also suggested that policymakers are matching action with rhetoric after a central-backed editorial recently criticized what it said are “baseless” predictions about a tightening in liquidity. Stepping out, we continue to highlight that it is doubtful Beijing will allow credit tightening to derail economic growth with the current geopolitical backdrop.

Princeling Gifts: Jack Ma’s Ant in Talks to Share Data Trove With State Firms – WSJ

Ant Group Co. is in talks with Chinese state-owned enterprises to create a credit-scoring company that will put the fintech giant’s proprietary consumer data under regulators’ purview as soon as the third quarter of this year. Ant, whose Alipay platform handled the equivalent of more than $17 trillion worth of payment transactions and originated loans to more than a third of China’s population in the year to June 2020, has collected troves of consumer data for years.

Why it Matters:

A few points worth bringing up. One, for all of China’s world-beating advances in mobile payments and financial technology, the country has lacked a robust national credit-scoring system akin to America’s FICO. This is a long-overdue move to change that. Second, the new venture with state-backed investors would override Ant’s previous attempts to spearhead a national credit-scoring system under its own brand. There was never a chance that Beijing wouldn’t seize this data, so no surprise here. Finally, this potentially represents a sign that Jack Ma, the head tech-princeling, is slowly moving back into XI’s favor after a year of exile following some “unpatriotic” remarks, something he now has to pay a high price for.

LONGER-TERM THEMES:

National Security Assets in a Multipolar World:

Solar Ban: U.S. bans imports of solar panel material from Chinese company - Reuters

On Wednesday, the Biden administration ordered a ban on U.S. imports of a key solar panel material from Chinese-based Hoshine Silicon Industry over forced labor allegations. The U.S. Commerce Department separately restricted exports of four other Chinese companies, saying they were also involved with the forced labor of Uyghurs and other Muslim minority groups in Xinjiang.

Why it Matters:

We highlighted Monday that First Solar was increasing production capacity in the U.S., “confident the current administration would have their back.” Two days later, our prediction of Chinese solar importers being penalized for human rights abuses is coming true. Unfortunately, as we have highlighted, this will increase production costs as cheaper monocrystalline silicon and polysilicon from China become less available as the ban is expanded. By the way, the global solar energy supply chain has already been squeezed by record-high costs for polysilicon, labor, and freight.

Electrification Policy:

Hardware vs. Software: Apple's Fight for Control Over Apps Moves to Congress and EU - WSJ

Apple is arguing that allowing users to download apps directly onto their iPhones without using Apple's App Store would harm customers by threatening privacy protections, complicating parental controls, and potentially exposing users' data to ransomware attacks. Apple's defense of its mobile operating system, or iOS, comes ahead of an expected debate Wednesday in the House Judiciary Committee on a package of bills aimed at reining in the nation's largest tech companies.

Why it Matters:

The upcoming ruling on "sideloading" will set an important precedent on whether security standards are more critical than anti-trust concerns. Separately, Apple's recent privacy protection changes have upended the way other tech firms generate revenue. These issues will have massive ramifications on gauging how consumers prioritize privacy concerns vs. connectivity, with privacy likely winning.

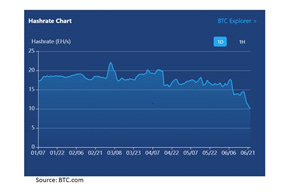

Shovel Sales Down: World’s Top Bitcoin Mining-Rig Maker Halts Sales as Clients Flee – Bloomberg

The world’s biggest maker of Bitcoin machines told the local mining community Wednesday it has stopped selling new equipment after prices for top-tier rigs plunged by about 75% since April. The firm said it will continue to sell gear for future delivery of devices used to mine smaller altcoins.

Why it Matters:

You know the gold rush is over when shovel prices drop. The dumping of used mining machines on the Chinese market coincides with a hashrate (total computational power to mine a Bitcoin) that declined by 50% in over a month. Elsewhere, Coinbase’s stock price is down over 50% from its IPO day high. It's safe to say China’s crackdown on miners has structurally changed the Bitcoin world.

ESG Monetary and Fiscal Policy Expansion:

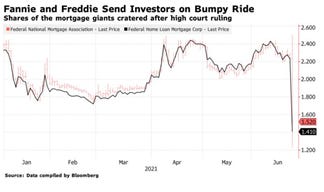

GSE Reform Reform: Fannie-Freddie Fate a Mystery After High Court Market Shock – WSJ

Yesterday's SCOTUS ruling means Fannie and Freddie can continue to stay in conservatorship as long as the current administration and Congress would like. The ruling also made clear that the president can remove the Federal Housing Finance Agency head, Fannie and Freddie’s overseer. Within hours, the White House said Biden would oust FHFA Director Mark Calabria, a libertarian economist who former President Donald Trump installed.

Why it Matters:

For many years we heard about the windfall of back pay the GSEs would payout to investors, and for many years we rolled our eyes. It never seemed realistic that the federal government would pay out over $100 billion to hedge funds while also losing control of a critical housing policy tool. With housing affordability back in the spotlight, the FHFA Director will likely use Fannie and Freddie more strategically to help lower-income renters and homeowners, increasing the risk of capital allocation distortions in the housing market (give it a few years though as GFC lessons will be totally forgotten by then).