MIDDAY MACRO - 6/23/2021

Daily Color on Markets, Policy, and Geo-Politics

MIDDAY MACRO - DAILY COLOR – 6/23/2021

PRICE MATRIX

OVERNIGHT/MORNING RECAP & MARKET WRAP

Narratives:

Equities are flat, with the Russell have a catch-up day while S&P and Nasdaq are flat

Treasuries are lower, with the curve again steepening

WTI is higher, but off the NY-open high of $74.25

Price Action:

Quiet price action today following a low volume two-day rally

Russell outperforming S&P/Nasdaq

Momentum, Small-Cap, and Value factors outperforming

Energy, Consumer Discretionary, and Financial sectors outperforming

Zero Gamma Level is 4206 while Call Wall is 4275, technical levels have support at 4222, 4205 while resistance is at 4245, 4265

Major Asian indexes are mixed: Japan flat. Hong Kong +2%. China +0.3%. India -0.5%.

European bourses are mixed, at midday, London +0.3. Paris -0.4%. Frankfurt -0.4%.

Treasuries lower with the curve flattening for a third day

5yr = 0.86%,10yr = 1.48%, 30yr = 2.12%

WTI higher by 1.1 % to $73.40

Copper higher by 2.2% to $4.32

Aggs are mixed with Soyoil and Oats outperforming

DXY flat at 91.7

Gold higher by 0.6% to $1790

Bitcoin higher by 3.5% to $33.6K

Econ Data:

Global Markit PMIs: U.S. manufacturing beat expectations while service came in notably below expectations. Overall, the expansion rate softened from the high seen in May. Increases in new orders were weighed down by supply delays and labor shortages in both manufacturing and services. The Eurozone PMI was the strongest in 15 years and had a very similar feel as the U.S. in positive/negative themes.

Why it Matters: The U.S., U.K., and EZ PMI Composites all highlighted worsening real supply-side constraints and increasing inflationary pressures. The Eurozone report noted, “average input prices rose at a rate exceeded only once over the 23-year survey history” and “average prices charged for goods and services meanwhile rose at by far the fastest pace since comparable data for both sectors were first available in 2002, with prices rising in each sector at rates not exceeded for approximately two decades.” The U.S. report note “rate of input price inflation softened slightly but was the second-fastest on record.” And “The increase in selling prices was the second sharpest since data collection began in October 2009.” Again, more data reinforcing our view that although we may be near peak velocity, inflationary pressures will continue for some time.

New Home Sales: New home sales dropped by -5.9%, coming in below expectations. There was also a downwardly revised level for April (revised to 817K from 863K). New home prices were significantly higher as with existing homes, with the median price rising 18.1% from May 2020.

Why it Matters: Whether new or existing, home prices are up, and affordability is down. This problem will persist, but housing fundamentals are strong according to builders, and they will work through shortages and cost pressure constraints. However, until this occurs, owner-equivalent rent will continue to rise.

Policy Talk:

Fed Governor Bowman: During a speech given at a policy summit hosted by the Cleveland Fed, Bowman gave her outlook on the economy and commented on inflationary pressures and maximum employment goals. She highlighted that inflation would likely rise further, and the forces causing it (supply-side bottlenecks) will take some time to get resolved. In addition, she emphasized that employment among lower-income, minorities, and women were still far from the Fed’s goal. “The Federal Open Market Committee views the maximum level of employment as a broad-based and inclusive goal. Thus, these gaps in employment and other measures of economic wellbeing can be interpreted to show that more progress is needed to reach maximum employment.”

Why it Matters: On top of further clarity on the Fed’s AIT tolerance and transitory inflation views (which Powell and a few others are now hinting might last longer), it is essential to watch for further clarification on what maximum employment is. It’s almost comical that an organization that claims it is data-dependent is so reluctant to set thresholds and goals for those data levels. As a result, we continue to believe that even with a robust employment picture developing over the rest of the year, the Fed’s more ESG cultural-tilt will increasingly site “inclusion goals” as reasons to be patient in removing accommodation (increasing the policy error tail-risk towards being too dovish).

Analysis:

In what looks to be another low volume day for equities, the S&P and Nasdaq are floating near their all-time highs while the Russell prepares for a sizeable rebalancing this Friday.

All our favorite meme/Reddit names could see strong flows off this rebalancing, but you probably aren’t reading this daily if you're trading those.

The Treasury curve is again steepening, showing that the unwind of steepener trades last week may have been overdone.

Investors continue to reembrace reflationary-themed positions this week while Fed officials walk back hawkish interpretations of the dots.

Metal markets are calling China out as copper is now over 6% off its recent low, following a drop of 16% from its May highs.

Price increases in thermal coal, aluminum, and contained selling in ferrous metals on the mainland also point to confusion over Beijing’s resolve/ability to reign in price increases.

Oil continues its accent with the rosy fundamental backdrop we have previously highlighted continuing to support the linear rise we see in prices.

Iran sanction relief will likely materialize soon, potentially dropping prices by a few dollars, given the expectations for Iran to draw down its sizeable inventory quickly.

However, even in the face of increased Delta variant cases, demand expectations are unwavering, and at least in the U.S., meaningful production increases seem far away.

This does open up an ascending channel to +$100 WTI by year-end.

We are, of course, nervous about agreeing with what is becoming a very consensus view by the sell-side.

Fundamentals also support a rise in natural gas (outperforming oil), which we hope to elaborate on soon.

WTI should continue to outperform Brent as the threat of OPEC+ production increases will weigh on sentiment there.

The PMI data and housing data today continue to reinforce our conviction that growth is capped by real supply-side constraints while inflationary forces are transitioning into the next phase of the cycle.

We were also encouraged to see further Fed officials beginning to acknowledge the “transitory” factors are not transitioning away soon.

TECHNICALS / CHARTS

FOUR KEY MACRO HOUSE CHARTS:

Growth/Value Ratio: Growth Outperforming on the Week

Chinese Iron Ore Future Price: Iron Ore Lower on the Week

5yr-30yr Treasury Spread: Curve is Steeper on the Week

EUR/JPY FX Cross: Euro Higher on the Week

HOUSE THEMES / ARTICLES

MEDIUM-TERM THEMES:

Real Supply Side Constraints:

Yantian: 6 charts show the effects of Yantian port congestion – Supply Chain Dive

COVID outbreak at the main port of Yantian continues to have massive effects on global shipping. In a more recent update, Maersk said operations at the port are set to improve as workers return. But issues are expected to remain. "While this has a positive impact on gate activity, which is soon expected to reach the same levels as before the incident, schedule reliability will continue to suffer with an average waiting time of 16 days and counting," Maersk wrote to customers Monday.

Why it Matters:

The article elaborates on the numerous ways the shutdown of the Yantian port hurt global trade and increased shipping costs. Between the shutdown of this port and the blockage of the Suez Canal, it is still clear that the global trading system has numerous critical chokepoints that, if disrupted, can have significant negative ramifications for some time.

No Vacancy: Warehouse Rents Surge on Bidding Wars for Scarce Space – WSJ

The competition for warehouse space is driving up industrial rents as retailers and logistics providers race to move goods closer to population centers, with some engaging in bidding wars for the most coveted sites. Industrial taking rents were up 9.7% in the first five months of 2021 compared with the same period last year.

Why it Matters:

The amount of available industrial land for new warehouses near urban centers has declined over the past decade. That’s adding to the pressure on the supply of warehouses. Since there is no immediate fix, the rising rents will likely continue as e-commerce is certainly not subsiding even as the economy re-opens, furthering the increased costs firms are experiencing with logistics and strengthening the inflationary pulse.

Chip-Starved: Wait Times for Chips Hit Record 18 Weeks as Shortage Deepens – Bloomberg

Chip lead times, the gap between ordering a semiconductor and taking delivery, increased by seven days to 18 weeks in May from the previous month, an indication that chipmakers’ struggles to keep up with demand are worsening. Power management chips, semiconductors that regulate the flow of electricity in everything from industrial machinery to smartphones, are a primary reason for the overall increase. Lead times for those chips hit 25.6 weeks, nearly two weeks longer than a month earlier.

Why it Matters:

A little bit of a broken record here, but important to continue to highlight that the disruptions have yet to subside, and as a result, we should continue to see growth capped while inflation pressures continue.

China Macroprudential and Political Tightening:

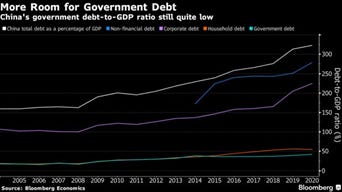

MMT: MMT Makes Inroads in China With Calls for Bigger Fiscal Stimulus - Bloomberg

China’s government is facing more calls to reduce its concerns about debt, with several influential economists arguing that authorities should follow the U.S. playbook and borrow more to spur the economy. “There’s a new understanding of debt in macroeconomics,” Liu Lei, a senior researcher at the National Institution for Finance and Development, a top government think tank, said in an interview. “Unlike the private sector, the government can continue to borrow new funds to repay old debts. The only requirement for this to go on is that interest rates remain low.”

Why it Matters:

It continues to seem highly unlikely to us that Beijing will allow its economy to cool while increasing its current more aggressive international posturing and trajectory. Xi himself took the economic failings of the west during the GFC and Eurozone debt crisis as a sign it was China’s time to assert itself on the global stage (which set the grounds for the massive credit expansion that still exists). Hence, it is meaningful that many top Chinese economists are advocating for greater coordination between fiscal and monetary policy to manage/promote growth.

LONGER-TERM THEMES:

National Security Assets in a Multipolar World:

Semi Production: U.S. Firm GlobalFoundries Invests $4 Billion in Singapore Chip Plant - Bloomberg

The U.S.-based company GobalFoundries, controlled by the Abu Dhabi SWF, joins rivals from Taiwan Semiconductor Manufacturing Co. to Samsung Electronics Co. in expanding capacity to help address a persistent shortfall of chips for everything from cars to smartphones. GlobalFoundries, which is prepping for a U.S. initial public offering that could value the chipmaker at $30 billion, said it’s focusing on Singapore but will also devote $1 billion apiece to building out its Dresden, Germany, and U.S. sites.

Why it Matters:

There are two main points to highlight here. First, chipmaking facilities typically start producing chips 18 months to two years after breaking ground. Even with the major foundries announcing production increases, it will be sometime before supply constraints abate. Second, the company explained the decision to expand in Singapore because it is the region where current capacity is stretched. It will still be a challenge to bring home production even with generous incentives proposed by the Biden Administration and Congress as existing supply chains and end demand favor Asia.

Electrification Policy:

EU Cyber: EU to launch rapid response cybersecurity team - Politico

The European Commission will present its plan on Wednesday to set up what it calls the "Joint Cyber Unit," which would allow national capitals hit by cyberattacks to ask for help from other countries and the EU, including through rapid response teams that can swoop in and fight off hackers in real-time, according to the draft.

Why it Matters:

The Commission first promised to set up a Joint Cyber Unit in 2019 to stop the cyberattacks. Still, it took months to finalize because the EU doesn't have competence over national security, and EU countries have been hesitant to give away control over it. Things are getting so bad now that nations are more willing to band together and create new capabilities.

Tech Reg: Google Faces EU Antitrust Probe of Alleged Ad-Tech Abuses – WSJ

The European Commission, the EU's top antitrust enforcer, said Tuesday that its investigation, which has been underway informally since at least 2019, will look at a broad array of allegedly anticompetitive business practices around the Alphabet Inc. unit's brokering of advertisements and sharing of user data with advertisers across websites and mobile apps—one of the newest areas of antitrust scrutiny for the company.

Why it Matters:

Tuesday's case is the first time the commission has formally opened a new investigation against Google since it issued three antitrust decisions against the search giant, backed by $9 billion in fines, between 2015 and 2018. It is on top of the probes into Google's privacy policies (third-party cookies use) and numerous cases against other big-tech firms in various areas. We highlight this to stress that the global big-tech regulation crackdown continues and will ultimately hurt earnings growth for these firms as they are forced to change their business models.