MIDDAY MACRO - 6/22/2021

Daily Color on Markets, Policy, and Geo-Politics

MIDDAY MACRO - DAILY COLOR – 6/22/2021

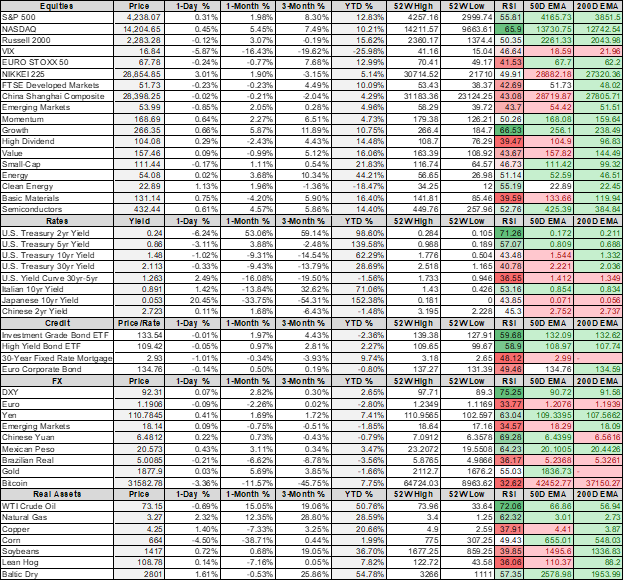

PRICE MATRIX

OVERNIGHT/MORNING RECAP & MARKET WRAP

Narratives:

Equities are higher, with buying picking up after the NY-open

Treasuries are mixed, with the curve marginally steepening

WTI is slightly lower, however, gasoline and natural gas are rallying higher

Price Action:

Nasdaq is outperforming despite rising long-end yields

Nasdaq outperforming S&P/Russell

Momentum, Growth, and Low Volatility factors outperforming

Consumer Discretionary, Materials, and Energy sectors outperforming

Zero Gamma Level is 4223 while Call Wall is 4275, technical levels have support at 4205 while resistance is at 4245

Major Asian indexes are mixed: Japan +3.1%. Hong Kong -0.8%. China +0.8%. India flat.

European bourses are mixed, at midday, London flat. Paris -0.1%. Frankfurt +0.3%.

Treasuries mixed with the curve flattening

5yr = 0.86%,10yr = 1.48%, 30yr = 2.11%

WTI lower by -0.4% to $72.80

Copper higher by 1.3% to $4.24

Aggs are mixed but generally higher

DXY lower by -0.1% to 92

Gold lower by -0.3% to $1780

Bitcoin lower by -4% to $31.2K after forming a “death-cross”

Econ Data:

Existing Homes Sales: While sales were down -0.9% on the month, the median existing-home price for all housing types saw a record year-over-year increase of 23.6%. This month was the fourth month of declines, however, sales in total are up 44.6% from a year ago. "Home sales fell moderately in May and are now approaching pre-pandemic activity," said Lawrence Yun, NAR's chief economist. "Lack of inventory continues to be the overwhelming factor holding back home sales, but falling affordability is simply squeezing some first-time buyers out of the market.”

Why it Matters: The more granular data around existing home sales is alarming. Prices continue to rise, and inventory continues to drop. There is now a drop in first-time buyer activity while a continued second-home buyers activity is increasing (mostly all-cash), hurting affordability. Looking at the big picture and considering the buying activity by private equity recently, housing policy is more and more likely to be included in any infrastructure or stand-alone legislation.

Richmond Fed Manufacturing Index: The composite index rose from 18 in May to 22 in June. This was primarily driven by an increase in the new orders index. Manufacturers continued to report shrinking inventories, growing order backlogs, and lengthening vendor lead times. Many manufacturers increased employment and wages in June and expected further increases in the next six months. Firms continued to struggle with finding workers while the average growth rates of both prices paid and prices received by survey participants declined slightly.

Why it Matters: Today's report showed that firms expect price increases to begin to stabilize while hiring and wage increases are likely to persist. This aligns with our view that we will continue to transition from cost-push inflationary pressures (caused by disruptions from the pandemic) to more demand-pull and eventual wage-spiral inflationary regimes.

Policy Talk:

NY Fed President Williams: At remarks to the Midsize Bank Coalition yesterday, Williams spoke about developments in replacing LIBOR and his economic outlook. He highlighted that the economy is recovering much faster than initially expected and sees two main downside risks. First, a slower international recovery that “could spill over to the U.S. recovery.” Secondly, a reversal of currently occurring inflationary pressures next year. He believes there is a risk that the forces causing the uptick in inflation now could quickly correct and, as a result, pull inflation down next year, causing it to undershoot their target. He sights used cars and lumber as examples of transitory price action.

Why it Matters: Williams is the second Fed official to use lumber prices as an example of supply and demand quickly correcting; hence the transitory inflationary narrative will be correct. The problem with this is that, yes, lumber is down 40% from its recent highs but is still up over 150% from last year's lows, and there is no guarantee it doesn’t go back up. Our point is that the Fed is now grasping for any signs of transitory activity while the multitude of forces pushing and pulling on inflation have yet to show signs of subsiding.

Analysis:

Today’s theme is “Everything but Bitcoin,” as both equities and commodities are generally well bid while Treasuries continue to unwind the flattening that occurred last week slightly.

S&P is essentially unchanged from a week ago; however, the total option positions are much lower, inferring higher market movement and less dealer resistance and support.

Two-day gains in copper and gasoline point to the reloading of reflation trade favorites.

The 2-yr auction today and Powell’s testimony should be non-events, but of course, could always stir things up.

Bitcoin is bouncing off morning lows but technically looks set to fall further, likely to around $15k.

As last week's post-FOMC turmoil subsides from rate markets, it is worth relooking at some of the developments that came out of the meeting.

Thirteen out of the eighteen committee members now see upside risk to inflation compared with only five at the March meeting.

All eighteen participants saw more significant uncertainty in their core inflation outlook in June versus sixteen in March.

Core PCE inflation will have to average a monthly increase of 0.1% through year-end to meet the Fed’s year-end core inflation forecast of 3%.

This is highly unlikely even as transitory pressures (used-car prices and other re-opening themed areas) subside due to the increases now occurring in owner’s equivalent rent and goods and services more generally.

Chair Powell continues with the mantra that inflation is transitory, but the implied five‐year average PCE inflation rate at the end of 2023 is now above target at 2.1% on the median SEP path.

At a minimum, the Fed has to raise its 2021 inflation forecasts in September while acknowledging greater upside risks and tremendous uncertainty surrounding the forecast.

This means the Fed can potentially increase the number of expected hikes in 2023 in following meetings without signaling a real tightening of policy.

Signaling the potential for two rate hikes in 2023 did not represent a tightening of policy in June versus the March forecast but instead an adjustment of the policy stance to a higher inflation projection.

If the Fed had left the dots unchanged on this raised inflation outlook, the SEP guidance would have represented an easing of policy.

As a result, we continue to question the initial price reaction following last week’s FOMC meeting.

Markets indicated that they believe inflationary forces are transitory and will be contained by a faster-moving policy tightening response.

While there has undoubtedly been a regime shift by the Fed, and a sequence of accommodation removal is beginning, we believe the Fed is still naïve to the strength and length of the inflationary pulse we have entered.

Further inflation outlook increases followed by increased rate hike projection through the SEPs in subsequent meetings will keep policy neutral, not actually tighter.

In conclusion, the view that the Fed is becoming more hawkish and will be able to contain inflation easily is wrong, and markets need to price this more appropriately.

TECHNICALS / CHARTS

FOUR KEY MACRO HOUSE CHARTS:

Growth/Value Ratio: Growth Outperforming on the Week

Chinese Iron Ore Future Price: Iron Ore Lower on the Week

5yr-30yr Treasury Spread: Curve is Steeper on the Week

EUR/JPY FX Cross: Euro Higher on the Week

HOUSE THEMES / ARTICLES

MEDIUM-TERM THEMES:

Real Supply Side Constraints:

Passing it on: Chip Shortages Are Starting to Hit Consumers. Higher Prices Are Likely. – WSJ

Price increases are snowballing their way through suppliers and critical materials in chip-making as the industry rushes to meet rising demand and plug supply holes. As a result, many of the world’s large chip makers are raising prices they charge to the brands that make PCs and other gadgets. For example, HP has raised consumer PC prices by 8% and printer prices by more than 20% in a year, while other PC makers have struck a similar note.

Why it Matters:

Long-time readers (for the two months we have been publishing) know that we firmly believe that a more prolonged inflationary wave is upon us. However, until recent months it has been primarily seen through increases in input and logistic costs borne by firms. There is now overwhelming evidence in the data, and from companies, significant end-product price rises are set to occur for some time. We feel it's necessary to continue to point this out, especially following last week's deflation of the reflation trade.

Wage Gains: Wage Gains at Factories Fall Behind Growth in Fast Food – WSJ

Manufacturers are losing workers to the service sector as wage increases are now luring workers there. The average hourly rate factory workers made in April is 27% more than the average pay for retail workers, down from a 40% premium for factory workers 10 years ago. The premium manufacturers pay has fallen due to global competition, outsourcing, lower unionization rates, and wider use of contractors. Jobs in manufacturing, in many cases, still offer better healthcare and retirement benefits than some other industries. However, the recent movement shows that this premium is not enough to keep workers from leaving.

Why it Matters:

Two main takeaways worth highlighting. First, the fact that manufacturers are losing workers to the service sector shows that the labor pool is much smaller than thought, and worker's ability to demand higher wages is getting stronger. Second, firms in the service sector are increasing offered benefits to attract labor, increasing employer costs and pushing final consumer prices higher.

China Macroprudential and Political Tightening:

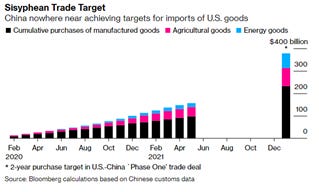

Trade Deal: China’s Progress on U.S. Trade Deal Slowed Again in May - Bloomberg

China bought almost $10 billion worth of manufactured, agricultural, and energy goods from the U.S. in May, the lowest monthly total since October 2020. That took total imports to almost $157 billion since January 2020, 41.4% of the two nations' targets agreed at that time.

Why it Matters:

Capitalist peace theory dictates that those that trade with each other are less likely to enter into a conflict. Given the deterioration in the relationship, the unlikelihood that China meets its trade deal obligations is a further troubling sign.

LONGER-TERM THEMES:

National Security Assets in a Multipolar World:

Subsidized Solar: Can America’s Solar Power Industry Compete with China’s? One Firm Tries – WSJ

First Solar is trying to compete with government-subsidized solar panel manufacturers in China. It has just committed to building a new $680 million panel factory in Ohio. A key reason is the company’s confidence that Washington will have its back with its reshoring policy plans.

Why it Matters:

The article gives a good overview of the global solar panel industry and the general challenges of reshoring production domestically. Specific to solar, the Biden administration already supports extending tax credits for solar panel purchases. It is weighing whether to back tax credits that would give domestic panel makers a lift and disadvantage imports. Recently human rights concerns have also increased the likelihood that Chinese imports may be penalized.

Commodity Super Cycle Green.0:

Shale 2.0: Cash gushes freely in shale oil bonanza - Argus

Most shale firms are just spending enough to keep output flat and using excess cash to accelerate debt repayments and increase shareholder dividends. Output remains stalled in the lower 48 US states this year, but benchmark WTI is up by two-thirds at over $70/bl. The shale industry is expected to earn record revenues this year before taking hedging into account, consultancy Rystad Energy says. Yet firms are unwilling to spend more to boost output until oil market fundamentals tighten.

Why it Matters:

The future of the shale industry looks very different from its past as investors come to terms with the energy transition. Shale firms are keen to show that they can now offer higher rates of return than many other investments. But the oil majors are shedding upstream assets as they diversify away from hydrocarbons. And about $17bn in private equity money has announced an exit from the shale sector so far this year, with more expected to follow. This is all very supportive of oil prices continuing to rise.

Swine Flu 2.0: Swine Fever Variants Lead to Mass Outbreaks Across China - Caixin

A new, difficult-to-detect variant of the African swine fever virus is circulating in China. The spread of the disease to pig herds across the country this year has led to rising incidents of mass infection on farms and stepped-up control measures to stop swine fever’s further spread into livestock supply chains.

Why it Matters:

The rebuilding of China’s pig herds was a significant driver of grain demand from the U.S. in the past. It is important to watch the development of this new strain as it will also profoundly impact grain demand in the long run if it comes anywhere close to being as deadly as the previous strain.

ESG Monetary and Fiscal Policy Expansion:

BoGreen: BOJ to launch new scheme for fighting climate change, keeps policy steady - Reuters

The Bank of Japan surprised markets on Friday by unveiling a plan to boost funding for fighting climate change, committing to releasing a preliminary outline of its plan at its next policy-setting meeting. “While the BOJ does not rule out buying green bonds in the future, the new scheme is better suited to address climate change in Japan where most companies rely on bank loans rather than raise funds from the market,” Kuroda said.

Why it Matters:

Kuroda is eluding that regulatory forces can alter capital allocation from the banking sector to more green endeavors while also supporting green bonds through open market operations. This approach is similar to the ECB and pairs with green fiscal policy initiatives in Japan. Unfortunately, much of Japan's energy production is coal-based following Fukushima, while it still has heavy industrial interests to consider. It is certainly an interesting development but likely the beginning of a long road to transition to a more green economy.