MIDDAY MACRO - 6/2/2021

Daily Color on Markets, Policy, and Geo-Politics

MIDDAY MACRO - DAILY COLOR – 6/2/2021

PRICE MATRIX

OVERNIGHT/MORNING RECAP & MARKET WRAP

Narratives:

Equities are mixed, with S&P and Nasdaq higher after NY-open

Treasuries higher as the long-end is well bid

WTI is higher as confusion over the timing of an Iran deal continues

Price Action:

Equities are generally quiet as a flat overnight turned into some NY-open buying

S&P/Nasdaq outperforming Russell

Growth, Low Volatility, and High Dividend Yield factors outperforming

Technology, Energy, and Real Estate sectors outperforming

Gamma gravity continues to be 4200, Call Wall is at 4250, technical levels remain the same with support at 4185 while resistance is 4220

Major Asian indexes are mixed: Japan +0.5%. Hong Kong -0.8%. China -0.8%. India -0.2%.

European bourses are higher, at midday: London +0.2%. Paris +0.3%. Frankfurt +0.1%.

Treasuries high with the curve bull flattening

5yr = 0.79%,10yr = 1.59%, 30yr = 2.27%

WTI higher by 0.9% to $68.30

U.S. gasoline demand reached the highest level since the start of the pandemic last week

Copper lower by -0.6%to $4.62

Reuters reported on Tuesday that the Yangshan copper premium has now sunk to a record low while on the LME, the cash to three month’s time spread has fallen to a $10 contango - all showing falling demand

Aggs are mixed but generally softer

DXY higher, but off AM highs, now around 89.9

Gold flat to $1905

Bitcoin higher by almost 6% to $38.1K

Econ Data:

Eurozone PPI: Headline Eurozone PPI came in at 7.6% YoY in May, the fastest pace of growth in over twelve years. EZ PPI has risen by 14% at an annual rate in the first four months of the year, showing that these significant increases are not base effects. Yesterday’s EZ Markit PMI report noted that average input costs again rose substantially, with the rate of inflation hitting an unprecedented level in line with widespread product shortages. Finally, earlier in the week, Germany’s inflation rose 2.4% in May, its highest rate in more than two years.

Why it Matters: The longevity of this inflationary pulse will be tied to end demand and inventory restocking. There have yet to be signs that demand is weakening, and inventory levels continue to be near historic lows for many industries. As a result, what was expected to be “transitory” continues to be “sticky” globally.

Policy Talk:

Governor Brainard: Remarks yesterday highlighted a belief the Fed is still “far from its goals,” and that there is still downside as well as upside risks to the fulfillment of these goals. As a result, she does not lean into the narrative that it might be appropriate “in upcoming meetings” to begin discussing tapering if the economy continues to improve rapidly. Nevertheless, her remarks suggest we are getting closer to seeing that debate from the FOMC.

FRBSF Economic Letter: The Divergent Signals about Labor Market Slack: A broad dashboard of indicators is sending mixed signals about the state of the labor market. Some indicators have deviated widely from their normal historical relationships since the onset of COVID-19. Because of the uneven economic impact of the pandemic, the labor force participation rate, payroll employment, and the share of job losers among the unemployed have provided more reliable signals about overall conditions than other components of the dashboard. They suggest that labor slack is higher than implied by the current headline unemployment rate.

Why it Matters: Brainard’s comments and the San Fran Fed’s research highlight the risk that policy will remain overly accommodative due to specific labor metric targets taking longer to be reached.

Analysis:

Equity and Treasury markets continue to chop in their recent ranges as increasing warning signs of growing inflation fail to overcome the weight that the historic level of excess liquidity is putting on yields.

The energy, precious metal and basic materials miners, and real estate sectors have been outperforming recently, highlighting an inflationary hedge rotation is occurring.

Floating rate instruments and stocks of companies that plan increases in dividends and buybacks will continue to price at an increasing premium.

The Fed’s balance sheet will reach $8 trillion this week while continued increases in front-end Fed repo operations show that excess liquidity is only growing.

Only tapering and restocking of the TGA account will meaningfully change this.

A day of reckoning is coming for rates and subsequently equities, but currently, supportive financial conditions and a Fed detached from reality support risk appetite and duration demand.

Don’t fight the Fed and instead be patient for a potential final equity melt-up over the summer followed by a taper tantrum-driven correction into year-end.

We continue to favor positioning in equity sectors that fare better under a stronger and longer inflationary backdrop, such as energy, precious metal and basic materials miners, and REITs as well as companies that can defend margins and pass on increasing levels of capital to shareholders.

TECHNICALS / CHARTS

FOUR KEY MACRO HOUSE CHARTS:

Growth/Value Ratio: Value Outperforming on the Week

Chinese Iron Ore Future Price: Iron Ore Higher on the Week

5yr-30yr Treasury Spread: Curve is Steeper on the Week

EUR/JPY FX Cross: Euro Lower on the Week

HOUSE THEMES / ARTICLES

MEDIUM-TERM THEMES:

China Macroprudential and Political Tightening:

Infrastructure REITs: China’s First Publicly Traded Infrastructure REITs Oversubscribed on Debut - Caixin

The strong market sentiment toward the nine REITs will buoy the Chinese government’s drive to introduce private money into infrastructure projects and ease local governments’ heavy debt burden. The nine infrastructure REITs were well received because the projects they fund were screened by the authorities and are all relatively high-quality, an analyst with a securities firm said.

Why it Matters:

These infrastructure-related REITs have a complicated structure. They allow investors to buy shares in mutual funds, which invest in asset-backed securities that hold ownership or management rights of infrastructure projects (which pay off debt from rents and toll fees). Important to watch the various ways Beijing will try to reduce local government debt levels and pass on NPLs to private investors, preferably foreigners. The complexity of these products also raises concerns and may be a prelude to the financial engineering lengths needed to hide the actual problem.

LONGER-TERM THEMES:

National Security Assets in a Unipolar to Multipolar World:

Quantum Comms: Europe picks EuroQCI satellite quantum communications consortium - SpaceNews

The European Commission awarded an Airbus-led group a contract to study a quantum technology-powered network, called EuroQCI, to secure critical infrastructure across Europe. The EuroQCI consortium hopes to run a demonstrator mission by 2024 and begin initial operations by 2027. “The key element is the possibility of using quantum technologies to exchange encryption keys, guaranteeing complete communication security in the management of vast quantities of data,” Leonardo general manager Lucio Valerio Cioffi, member of the group, said in a statement.

Why it Matters:

Security experts see quantum computing as a critical technology for combating cyberattacks that are a growing threat as more devices and operations are connected to communications networks worldwide. Although we do not pretend to be quantum computing experts, we do acknowledge that it is the next great arms race. Nations with superior “quantum” abilities in cyberspace will have the ability to dominate geopolitical relationships.

Electrification, Digitalization, and Cyber Security:

Crypto Card: Now use your Coinbase Card with Apple Pay and Google Pay – Coinbase Blog

Coinbase is partnering with Apple and Google to make it “easier” to spend your crypto, even offering 4% back in crypto rewards. “Splurging for guacamole with your Coinbase Card is a no-brainer when you can earn 1% back in Bitcoin or 4% back in Stellar Lumens,” Coinbase’s announcement states.

Why it Matters:

The further integration of the crypto world into mainstream finance, in this case, payment systems, is always important to watch. The two largest cryptocurrencies, Bitcoin and Etherium, currently have a market capitalization of close to $1 trillion, with the rest of the community adding several hundred billion dollars more. In theory, any increase in the fungibility of crypto holdings into direct purchasing power ability could significantly increase aggregate demand and inflationary pressures.

Ransomware: How to Negotiate with Ransomware Hackers – The New Yorker

In December, the acting head of the Federal Cybersecurity and Infrastructure Security Agency said that ransomware was “quickly becoming a national emergency.” The F.B.I. advises victims to avoid negotiating with hackers, arguing that paying ransoms incentivizes criminal behavior. However, there are about half-dozen ransomware-negotiation specialists, and the insurance companies they regularly partner with, helping people navigate the world of cyber extortion.

Why it Matters:

The article takes a deeper dive into the life of a ransomware negotiator and the general environment many businesses and governments are having to navigate as attacks increase. Given the daily barrage of “attack” headlines and real-life consequences of these attacks, it is essential to understand this world.

ESG Monetary and Fiscal Policy Expansion:

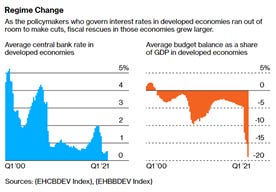

Mission Creep: The Covid Trauma Has Changed Economics—Maybe Forever – BBG

The pandemic has changed how policymakers will likely respond to “crisis” moving forward. Fiscal policy channeled cash directly to households and businesses and ran up record budget deficits. Central banks played a secondary and supportive role, buying the debt and other assets, keeping borrowing costs low. From politicians to central bankers, policymakers felt comfortable supporting the significant response to the pandemic, as no one was to blame for the pandemic.

Why it Matters:

The article highlights that fiscal and monetary policy has crossed the “Rubicon” and may now be more intertwined and active. The coordination of the two types of policies is a critical risk to inflation. Both monetary and fiscal policy are now being coordinated to fight inequalities and climate change as we move on from the pandemic crisis. The loss of confidence in policymakers as they “mission creep” and take on new mandates may lead to runaway inflation.

EU Bonds: EU to Raise $100 Billion in Bonds This Year to Finance Stimulus - BBG

The first syndicated bond issuance is expected later in June, while sales of the so-called “EU-Bills” will begin in September. EU member states have agreed to allow the Commission to raise as much as 800 billion euros ($978 billion) in debt, or about 150 billion euros a year by 2026, to finance investments in green and digital policies and help pull the economy out of recession.

Why it Matters:

These “stimulus fund” sales will make the EU’s executive arm the world’s biggest issuer of social and green debt and one of the most prominent sovereign issuers with a high credit rating. While the fund is meant to be a one-time emergency measure, several officials in Brussels and national capitals are betting on its success to convince hawkish countries, including Germany, Finland, and the Netherlands, to agree on a more permanent instrument. If made permanent, EU bills could become a key competitor to Treasuries and expand the Euro currencies footprint globally, all supporting a de-dollarization of trade and financial markets, although this would of course take some time.

Arctic Oil: Biden suspends oil leases in Alaska’s Arctic refuge - PBS

The Interior Department has suspended oil leases in Alaska’s Arctic National Wildlife Refuge after conducting a required review. Interior said it “identified defects in the underlying record of decision supporting the leases, including the lack of analysis of a reasonable range of alternatives” required under the National Environmental Policy Act, a bedrock environmental law.

Why it Matters:

This was not a surprise following a temporary moratorium Biden imposed via executive order on his first day. It is worth highlighting as it, along with other actions by this administration, is very supportive of oil prices. There has been no meaningful change in U.S. oil demand, as diversifying America's energy portfolio away from fossil fuels will take decades. At the same time, we continue to see future supply availability reduced. As a result, the energy industry should continue to see supportive prices, declining Capex opportunity (rewarding shareholders with higher cashflow capture), and the actual true cost will fall on the American people in the form of increased gasoline and energy bills.