MIDDAY MACRO - 6/18/2021

MIDDAY MACRO - 6/18/2021

Daily Color on Markets, Policy, and Geo-Politics

MIDDAY MACRO - DAILY COLOR – 6/18/2021

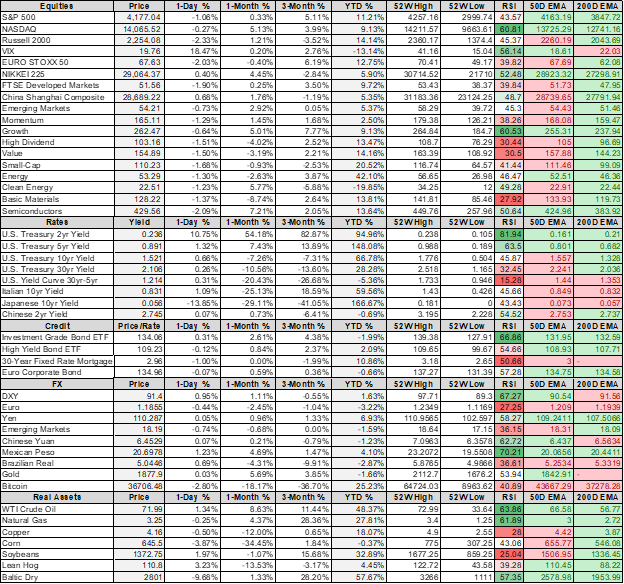

PRICE MATRIX

OVERNIGHT/MORNING RECAP & MARKET WRAP

Narratives:

Equities are lower, with quad-witching OPEX today driving price action

Treasuries curve is again flattening, although 5yr Treasuries are recovering from post-Bullard comments selling

WTI is higher, with strong buying at the NY-open

Price Action:

Nasdaq is weaker but outperforming, again helped by a flatter Treasury curve.

Nasdaq outperforming S&P/Russell

Growth, Low Volatility, Momentum factors again outperforming

Real Estate, Technology, Communication sectors outperforming

Zero Gamma Level is 4228 while Call Wall is 4250, technical levels have support at 4165 while resistance is at 4205

Major Asian indexes are mixed: Japan -0.2%. Hong Kong +0.9%. China flat. India +0.3%.

European bourses are lower, at midday, London -0.9%. Paris -0.2%. Frankfurt -0.6%.

Treasuries are mixed with a continuation of a curve flattening

5yr = 0.90%,10yr = 1.47%, 30yr = 2.03%

WTI higher by 1.2% to $71.60

Copper lower by -0.8% to $4.14

Aggs are higher in whats looks to be a relief rally

DXY higher by 0.9% to 92.4

Gold flat to $1780

Bitcoin lower by -2.5% to $38.9K

Policy Talk:

St. Louis Fed President Bullard: In an interview on CNBC this morning, Bullard said he sees an initial interest rate increase happening in late-2022 as inflation picks up faster than expected. “We’re expecting a good year, a good reopening. But this is a bigger year than we were expecting, more inflation than we were expecting,” the central bank official said on “Squawk Box.” “I think it’s natural that we’ve tilted a little bit more hawkish here to contain inflationary pressures.”

Why it Matters: Bullard, although not a voter, has become a much more vocal hawk, joining Kaplan in expecting faster removal of policy accommodation. Following this week's FOMC meeting (which signaled a regime shift), it is another warning sign that the punch bowl is starting to be taken away.

Analysis:

Equities are weaker and sitting at key technical support levels with a larger than normal expiration of optionality on today’s “quad witching,” likely keeping them somewhat contained.

There is $2.2 trillion in index option gamma set to expire today, reversing the oversupply of vol selling that had been occurring recently.

This large expiration opens up the range and increases volatility until gamma exposure has been reloaded.

Treasuries continue to signal that the Fed will be tightening sooner than initial thought, and inflationary pressures will be contained.

Historical week for curve flatteners trades while 5yr Breakevens have moved back to late February levels, pushing real rates higher.

Looking at the rotation back into growth and the flattening of the curve, one can only conclude a regime shift is underway.

Powell and company have changed their tune, so markets must now adjust.

Be defensive as next week will likely see selling pressure increase for equities.

TECHNICALS / CHARTS

FOUR KEY MACRO HOUSE CHARTS:

Growth/Value Ratio: Growth Outperforming on the Week

Chinese Iron Ore Future Price: Iron Ore Lower on the Week

5yr-30yr Treasury Spread: Curve is Flatter on the Week

EUR/JPY FX Cross: Yen Higher on the Week

HOUSE THEMES / ARTICLES

MEDIUM-TERM THEMES:

Real Supply Side Constraints:

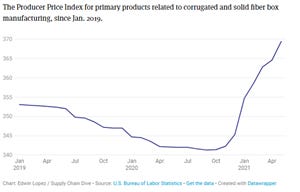

Boxes Needed: Increased containerboard output not enough to keep prices down – Supply Chain Dive

Recent data from the American Forest and Paper Association suggests the containerboard industry is producing close to full capacity. As production reaches capacity, corrugated packaging manufacturers are raising prices. Prices shot up during the first half of 2021, after remaining fairly flat in 2020 despite an uptick in demand.

Why it Matters:

Although AFPA found that containerboard production increased 9% in March compared to March 2020, the boost in supply was not enough to keep prices from going up this month. Rising containerboard prices could hurt companies relying on packaging to deliver goods ordered online to their customers. If prices continue to shoot up, companies will likely set higher prices to absorb the increase. Important to flag this as another area that is still seeing price increases.

Housing Shortages: Historic shortage of homes for sale fueled by builders' supply chain woes – Yahoo Finance

A labor shortage and lack of ready-to-build land and materials have limited the pace of construction. A new report from the National Association of Realtors (NAR) finds the housing market needs to build at least 5.5 million new units, both single-family and multi-family homes, to keep up with demand and keep homeownership affordable over the next decade.

Why it Matters:

Although the theme of low inventory, lack of labor, land, and higher costing materials is not new in housing, it is worth highlighting a few things. First, impairments that are increasing costs are now hurting builder’s ability to get loans, reducing confidence, and delaying the supply of finished homes. Second, given estimates by the NAR for needed supply, the inflationary pressure from housing, which has started to pick up, will likely be maintained for some time as builders continue to pass on cost increases and face strong demand. Finally, keep an eye on whether any housing investment policy makes it into an infrastructure bill.

China Macroprudential and Political Tightening:

Decoupling: China Growth Decouples From Credit, With Global Implications - BBG

Even though Beijing has been slowing credit expansion in the economy, that doesn’t have to mean slower growth or less demand for commodities. That’s because the traditional link between credit and growth is not as strong as it once was. Foreign demand is likely to keep exports strong, while domestically, more financing is being funneled to private-sector businesses. Service and technology companies, which require less credit to expand, make up a bigger portion of the economy.

Why it Matters:

China watchers look at the “credit impulse,” which measures the growth in new financing as a share of gross domestic product, as an indicator of business cycles. The article highlights the ways this business cycle barometer is becoming less relevant due to the evolution of the Chinese economy away from an investment-driven model to a domestic consumer-based one. The bottom line is that the slowdown occurring in China (being linked to the reduced credit pulse) is likely short-lived.

LONGER-TERM THEMES:

National Security Assets in a Multipolar World:

Reshoring: North America will not see significant supply chain reshoring in 2021-25 - Economist

Despite growing optimism among US policymakers that American companies could reshore production to North America, companies will be deterred by a lack of competitiveness, protectionism, and cross-border tensions, limiting optionality in the region. These factors will discourage the types of investment required to transform North America into a viable, self-sustaining supply-chain ecosystem.

Why it Matters:

A report by the Economist elaborates on the challenges to bringing manufacturing back to North America. There is a reason why much of the world's manufacturing moved to Asia, and it will take a significant effort to create a landscape in North America that can compete and beat Asia. Reshoring is a big and complicated issue, and it is worth highlighting any report which identifies the challenges.

Electrification Policy:

New Regime: Lobbyists for Silicon Valley Giants Like Facebook Find Glory Days Are Over – WSJ

Mr. Biden has shunned job applicants with ties to large technology companies. His decision to appoint Ms. Khan as FTC chairwoman Wednesday made one thing clear: There is to be no sequel to the tech industry’s glory days during Barack Obama’s eight years in the White House.

Why it Matters:

The appointment of two prominent big tech critics and the numerous bills that congress has put forth without feedback from tech lobbyists shows that there is a bipartisan disdain right now toward Big-Tech. With Big-Tech stocks currently rallying, it is worth remembering that these firms face a structurally different, more adverse landscape.

Commodity Super Cycle Green.0:

Cycles?: Top agricultural traders predict a ‘mini supercycle’ - FT

According to some of the world's top traders, agricultural commodities are at the start of a “mini-supercycle,” with prices expected to be boosted for several years by demand from China and for biofuels. Traders did acknowledge one of the considerable uncertainties was China. “Out of all big demand-driven areas in the world, China is the most opaque and the hardest to predict,” said Gary McGuigan, head of global trade at Archer Daniels Midland.

Why it Matters:

The current pullback in the agriculture complex is due to several factors such as weather, speculation, and uncertainty over Chinese demand. It is worth highlighting that the demand from China is one of the most challenging aspects to gauge. China’s use of trade as a geopolitical weapon, as seen with Australia and the uncertainty of the U.S.-Chinese trade deal, with negotiations set to start again, all add to the challenge.

Cocoa Farms: Supreme Court rules in favor of Nestlé USA and Cargill in human rights abuses case – FoodDive.com

The U.S. Supreme Court threw out a lawsuit against Nestlé and Cargill that claimed the companies were complicit in contributing to slavery at cocoa farms in Ivory Coast. However, the court sidestepped a broader ruling on the permissibility of suits accusing American companies of human rights violations abroad. A final ruling is expected by the end of June and could further shake up how American food companies monitor their international suppliers.

Why it Matters:

If the justices were to rule in favor of Nestlé and Cargill, it could curtail how international victims of human rights violations are able to use U.S. courts to sue. But if the court rules for the food giants, more companies could face lawsuits for crimes their suppliers commit internationally. Whether for geopolitical or ESG reasons, supply chain security will be an essential ongoing theme to watch. This particular case could significantly impact how resource firms run their business.

SG Monetary and Fiscal Policy Expansion:

Mandated ESG Disclosure: House Passes Bill That Would Mandate Disclosure of Climate Risks - BBG

Publicly traded companies would be required to disclose financial risks related to climate change under legislation approved by the House Wednesday and sent to the Senate, where it faces an uncertain future. The legislation would also require disclosure of other so-called environmental, social, and governance information related to political spending, tax jurisdictions, and executive pay raises.

Why it Matters:

More than 70% of companies don’t share climate-related information across categories recommended by the Financial Stability Board’s Task Force on Climate-related Financial Disclosures. The measure is unlikely to muster the Republican support needed to pass the narrowly divided Senate, but it comes as the SEC is preparing its own set of new corporate disclosure requirements for climate change risks, board diversity, and companies’ workforces by October.