MIDDAY MACRO - 6/17/2021

Daily Color on Markets, Policy, and Geo-Politics

MIDDAY MACRO - DAILY COLOR – 6/17/2021

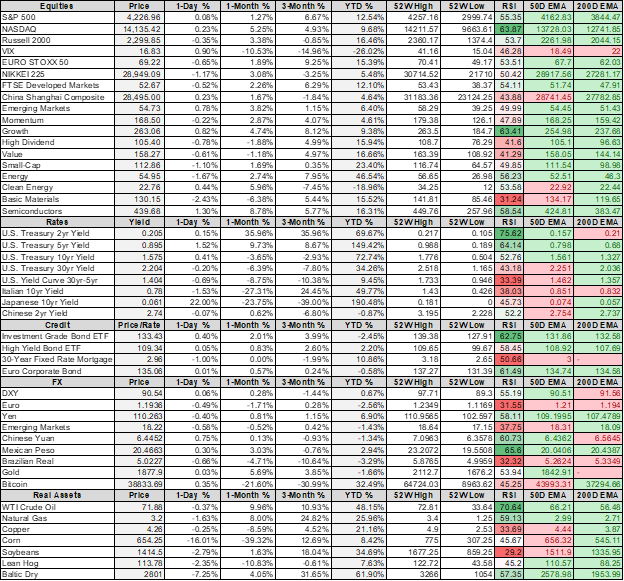

PRICE MATRIX

OVERNIGHT/MORNING RECAP & MARKET WRAP

Narratives:

Equities are mixed, with Nasdaq higher, S&P flat, and Russell down

Treasuries curve is flattening, as long-end is well bid

WTI is lower, with selling increasing after NY-open on Iran talk headlines

Price Action:

Nasdaq is benefiting from the drop in long-end yields

Nasdaq outperforming S&P/Russell

Growth, Low Volatility, Momentum factors outperforming

Technology, Communications, and Health Care sectors outperforming

Zero Gamma Level is 4206 while Call Wall is 4275, technical levels have support at 4170 while resistance is at 4235

Major Asian indexes are mixed: Japan -0.9%. Hong Kong +0.2%. China +0.2%. India -0.6%.

European bourses are mixed, at midday, London -0.5%. Paris flat. Frankfurt flat.

Treasuries mixed with a large bull flattening occurring

5yr = 0.89%,10yr = 1.53%, 30yr = 2.15%

5/30s curve is -14bps since 2pm yesterday and -40bps off march highs

WTI lower by -2.3% to $70.6

Copper lower by -3.8%to $4.21

Aggs are significantly lower

DXY higher by 0.9% to 91.7

Gold lower by -4.5% to $1780

Bitcoin higher by 1% to $38.9K

Econ Data:

Philly Fed Manufacturing Business Outlook: The overall index was little changed on the month, down one point to 30.7. New orders decreased 10 points while the current shipments index rose 6 points. Prices paid rose for the second consecutive month, 4 points to 80.7, its highest reading since June 1979, with 82% of firms reporting increases in input prices.

Why it Matters: Today’s regional Philly Fed data indicates current activity, new orders (although notably lower than last month), and shipments remain elevated. Additionally, both price indexes reached long-term highs. Finally, the survey’s future indexes indicate that respondents expect growth over the remainder of the year.

Policy Talk:

FOMC Recap: There was a more hawkish tilt to yesterday's FOMC meeting as the 2023 rate projection was raised more than expected. Powell also acknowledged “the possibility that inflation could turn out to be higher and more persistent than we expect.” There are now 7 of 18 participants projecting a rate hike in 2022 versus four participants expecting a 2022 hike at the March meeting. The 2021 inflation projection was revised higher (but likely not by enough). The Fed now describes inflation persistently below its goal in the past tense. Finally, Powell indicated that tapering discussions have begun in the press conference, thankfully ending the talking-about talking-about verbiage.

Why it Matters: The Fed gave a more credible message with guidance from the statement, SEPs, and press conference more aligned to the current economy and inflationary backdrop than the previous meeting. Nevertheless, the Fed will still need to raise its 2022 inflation expectations as even when the current blazing three-month annualized rate slows, as it should, their central forecast will be too low.

Analysis:

Equities and Treasuries are doing their correlation dance while the commodity complex looks downright ugly, showing how much say China still has there.

Treasury curve steepener trades continue to be unwound following yesterday’s FOMC.

Growth has been the clear outperformer as reflation/reopening trades have come under significant pressure.

A combo of things is hitting commodities today:

Chinese authorities have gone from jawboning metal prices lower to now releasing strategic state reserves.

Numerous other regulatory actions over the last months continue to weigh on speculatory activity.

Improved weather and crop harvest forecasts have hurt the agriculture complex after last week's WASDE report showed weaker export demand.

The sentiment is hurt by speculative crackdowns in China too.

Oil, the recent outperformer, remains at the mercy of “Vienna Talks” progress between the U.S. and Iran (today’s pullback).

Pushing down on the entire commodity complex is a stronger dollar, which was helped by increases in real rates following a more hawkish FOMC meeting.

The DXY has broken out of its 2020 downtrend after forming a double bottom around 89.3.

The market tells us investor sentiment is changing with the outperformance of growth over value and the Treasury curve flattening, pointing to lower expectations for growth and reduced policy accommodation next year.

Although we agree with a weaker growth outlook for next year, we believe the longer-term trends for higher commodity prices are still intact (due to the longer-term fundamental mismatch of supply and demand).

The current correction is a tactical pullback based mainly on the overshooting of fundamentals (due to excessive speculation) and unsustainable posturing by China.

However, do not try and catch a falling knife, instead look for cooling in China’s PPI (and rhetoric) and a renewal of a weaker dollar to reassess.

TECHNICALS / CHARTS

FOUR KEY MACRO HOUSE CHARTS:

Growth/Value Ratio: Growth Outperforming on the Week

Chinese Iron Ore Future Price: Iron Ore Higher on the Week

5yr-30yr Treasury Spread: Curve is Flatter on the Week

EUR/JPY FX Cross: Yen Higher on the Week

HOUSE THEMES / ARTICLES

MEDIUM-TERM THEMES:

Real Supply Side Constraints:

Battery Shortage: Shortages in Electric-Vehicle Battery Industry Play Havoc With Cell Prices, Executive Says - Caixin

Yang Hongxin, the president of SVolt Energy Technology, said at an industry forum that only 60% to 80% of orders for high-quality batteries were currently being met amid supply shortfalls that took root last year due to a lack of certain raw materials. The comments came as the global EV industry battles a twin scarcity of the batteries that power electric cars and the microchips that run their systems.

Why it Matters:

Some 217,000 new-energy vehicles (NEVs) were sold in China in May, a new record for the month. The figure brings the total number of NEVs sold in China this year to 950,000, more than three times the amount sold in the equivalent period of 2020. This increase in demand for EV batteries along with continued shortfalls in critical materials could see battery prices stabilize or increase globally, instead of the decline that was expected last year.

Limited Growth: Ifo Cuts German 2021 Growth Forecast on Supply Bottlenecks - BBG

Germany’s Ifo Institute cut its 2021 growth forecast to 3.3% from 3.7% as supply chain bottlenecks hold back momentum in Europe’s largest economy. “The main factor dampening growth in the short term are the bottlenecks in the supply of intermediate products,” said Timo Wollmershaeuser, who heads the institute’s forecasts division.

Why it Matters:

Germany’s economy has fared relatively well during the crisis compared to the rest of Europe, in part due to its strong reliance on manufacturing. Recent surveys, however, have shown the service sector driving the recovery as pandemic restrictions are lifted, and factories grapple with unprecedented supply-chain issues amid shortages of parts and raw materials.

China Macroprudential and Political Tightening:

State Supplied: China to Release Metal Reserves in Effort to Tame Commodities Rally – WSJ

China’s latest move targets copper, aluminum, and zinc, among other metals, and outlines a program of public auctions to domestic metal processors and manufacturers, the National Food and Strategic Reserves Administration said Wednesday. Much of the effectiveness of Beijing’s metal auctions will depend on the amount of metals it releases or that it is able to release into the market. The government doesn’t disclose its holdings.

Why it Matters:

Top Chinese officials have increasingly sought to rein in commodity price increases. The State Council last month said it would take steps to ensure adequate supply and stable prices for commodities. It will be critical to watch the Chinese PPI data. When it begins to decline, you may see Beijing reduce its efforts to subdue commodity price increases, as its primary concern seems to be price stability over growth still.

LONGER-TERM THEMES:

National Security Assets in a Multipolar World:

Second Job: Trial of Scientist Accused of Hiding China Work Ends in Hung Jury – WSJ

A federal judge ordered a mistrial Wednesday after a jury deadlocked over whether a former University of Tennessee scientist hid his work in Beijing to obtain U.S. government research grants. Prosecutors alleged that Mr. Hu, who specializes in nanotechnology research, misled his university and the U.S. government by not reporting his Beijing post in University of Tennessee conflict-of-interest forms and in applications for NASA grants. A 2012 law explicitly restricts NASA from funding any collaborations with China.

Why it Matters:

The mistrial verdict shows that it is often hard to find evidence of espionage. In the past two years, federal prosecutors have escalated efforts, charging around a dozen U.S. academics specifically with lying about their China work when seeking U.S. grants to support their research. The Justice Department has also prosecuted some researchers for stealing proprietary information rather than concealing any work in China. Technological innovations are national security assets and will need to be increasingly protected, reducing cross-border collaborations.

Electrification Policy:

Stablecoins: Crypto Lode of $100 Billion Stirs U.S. Worry Over Hidden Danger - BBG

Regulators are worried about hidden risks to investors and even the financial system stemming from stable coins, a form of cryptocurrency with a fixed price, typically one dollar, and is backed by real-money reserves. At the end of May, the total market capitalization of stablecoins, which include ones offered by crypto firms Tether and Centre, broke $100 billion.

Why it Matters:

Lawmakers and officials from the Federal Reserve and the administration have expressed alarm that some consumers won’t be protected should one of the firms fail. They also say the growing size of stablecoins has created a situation where vast amounts of U.S. dollar-equivalent coins are being exchanged without touching the U.S. banking system, potentially blinding regulators to illicit finance. This is just another example of the crypto world coming under further regulatory pressure.

ESG Monetary and Fiscal Policy Expansion:

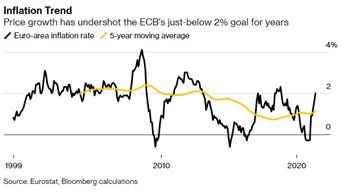

ECB 2.0: How the ECB Is Overhauling Strategy in the Midst of a Pandemic - BBG

The 23 member ECB Governing Council is meeting in person (first time since pandemic) to retool the ECB for the 21st century (20 years in). They will announce a new inflation goal, better ways of measuring the economy, and agreement on how to treat issues such as climate change and inequality. Results are expected ahead of the annual ECB Forum on Sept. 28-29.

Why it Matters:

Since the previous review in 2003, the euro area had grown from 12 members to 19, suffered two major crises, and seen the world economy fundamentally change. Hence, the exercise is far more significant than the previous one and similar to the Fed’s review, which comprised a “Fed Listens” initiative and rewriting the “Long-Run Goals.” Climate change has been the most contentious issue, championed by Lagarde but seen as something outside the scope of monetary policy by other council members. It will be essential to see if any significant changes come out of this review and further alter the ECB into a more ESG cultured entity.