MIDDAY MACRO - 5/27/2021

Daily Color on Markets, Policy, and Geo-Politics

MIDDAY MACRO - DAILY COLOR – 5/27/2021

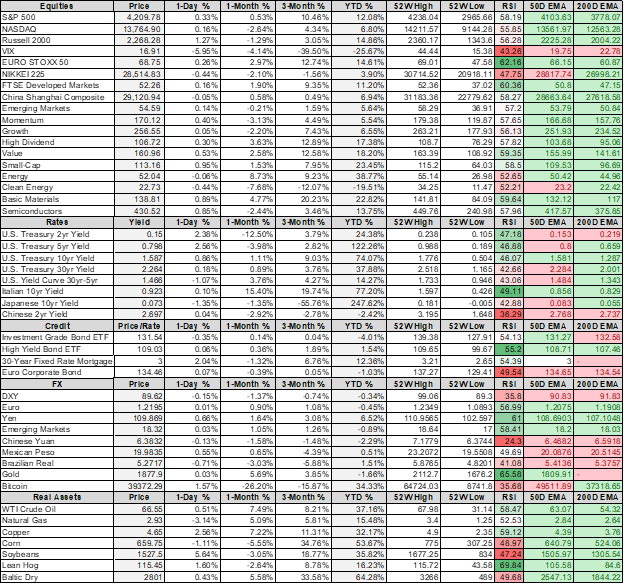

PRICE MATRIX

OVERNIGHT/MORNING RECAP & MARKET WRAP

Narratives:

Equities are higher, with Russell leading for a second day, following this morning’s econ data releases

Treasuries lower following an NYT article that highlighted a rather large first budget proposal from the Biden Administration

WTI slightly higher, attempting to break out of its recent multi-day consolidation range

Price Action:

S&P is pushing on the highs of its weekly range while momentum has picked up for the Russell

Russell outperforming S&P/Nasdaq

Small-Cap, Momentum, and Value factors outperforming (two days in a row)

Industrials, Materials, Consumer Discretionary sectors outperforming

Gamma gravity towards 4200 still strong while the Call Wall is back to 4250, technical levels remain the same with support at 4180 while resistance is 4220

Major Asian indexes are mixed: Japan -0.3%. Hong Kong -0.2%. China +0.4%. India +0.2%.

European bourses are higher, at midday: London 0%. Paris +1%. Frankfurt +0.2%

Treasuries lower with the curve bear steepening

5yr = 0.82%,10yr = 1.61%, 30yr = 2.29%

WTI higher by 0.15% to $66.30

EIA data out yesterday showed that crude stocks at Cushing fell by 1 million barrels to their lowest levels since March of 2020, while total stocks fell by 1.7 million barrels, but neither release was that consequential

Copper higher by 2.5% to $4.64

Chinese ferrous markets recovered overnight after several days of substantial declines, with traders citing previous instances when China resorted to similar restrictive measures having a passing negative effect

Aggs higher at NY-open with corn up 5.4%

Reuters is reporting that China's commerce ministry spokesman told a news conference on Thursday that China and the USA should work together to push for implementing the Phase 1 trade deal. Part of the deal states that China will significantly increase U.S. farm imports.

DXY flat around 90

Gold lower by -0.5% to $1890

Bitcoin higher by 4% to $40.1K

Econ Data:

Durable Goods: Core capital goods orders (excluding aircraft and military hardware) increased 2.3% MoM in May after a 1.6% gain in April. The median estimates called for a 0.8% increase in total durables orders and a 1% gain in core capital goods bookings. Business spending on equipment advanced at a 13.4% annualized rate in the first quarter, helping the economy grow at a 6.4% pace, according to today’s GDP estimates. Shortages of materials and delivery bottlenecks drove unfilled orders for durable goods to rise for a second month.

GDP and PCE Prices: GDP increased by 6.4% YoY in the first quarter, topping economists’ expectations for 6.1%. Personal consumption expenditures grew at a 10.7% annual pace while spending on services was little changed. Headline and core PCE prices increased 3.7% and 2.5%, respectively, marginally beating expectations.

Today’s data supports our view that second-quarter growth continues to look very strong. Growth will be driven by the continued reopening of the service sector where consumption will pick up further. Still, the second half of the year should see inflationary pressure increasingly reduce demand (already occurring in housing) while logistical issues continue to weigh on production capacity and earnings.

Analysis:

Rate sensitivity is beginning to show its head again a little today, with the Nasdaq underperforming as the Treasury curve steepens.

The 10yr Treasuries post-March range has been between 1.5% to 1.75% and, at 1.61% currently, has some ways to go before threatening a breakout into a higher range.

Oil markets look to be moving on from Iranian supply concerns and demand destruction in Asia as prices near their highs for the year.

Several bullish/bearish oil developments worth highlighting:

There is limited new evidence that demand growth is accelerating globally, despite this being a consensus view.

Lockdowns in India (and now other Asian nations) did significantly impact oil demand in April and will likely be worse in May given the increases in cases there as well as in other nations elsewhere in Asia.

The Colonial Pipeline shutdown weakened U.S. gasoline demand temporarily, but leisure activities should continue to grow over the summer, driving demand higher.

The next significant catalysts for further demand will be further office re-openings.

U.S. sanction relief on Iran may take longer to occur even as the deal looks more likely to get done.

Iran’s ability to meaningfully increase production in the interim is questionable given its reduced capacity and needed modernization of facilities.

US total petroleum inventories (crude plus refined products, excluding SPR) have now fallen to the end-of-March 2020 levels when the pandemic was in its early days.

Speculative flows have increased as inflation fears/hedges have intensified.

Bottom Line: We remain cautious on oil prices tactically, given the size and speed of the move higher over the last week, but believe that market sentiment and longer-term fundamentals will increasingly be supportive in the second half of the year.

The futures curve will need to flatten from “peak” backwardation to a more traditional curvature.

TECHNICALS / CHARTS

Four Key Macro House Charts:

Growth/Value Ratio: Growth Outperforming on the Week

Chinese Iron Ore Future Price: Iron Ore Higher on the Week

5yr-30yr Treasury Spread: Curve is Flatter on the Week

EUR/JPY FX Cross: Euro Higher on the Week

CPI – PPI Spread:

The spread between CPI and PPI (both y/y) is deeply negative and its lowest level since December 1974.

The last time that happened, CPI quickly went to 11%.

We see this as a clear indication that there still needs to be a substantial catch-up in consumer prices to producer prices, even following the increases in CPI already seen.

The impact which transitory components (used-auto sales, for example) have had on the headline/core indexes will increasingly be replaced by more significant structural increases, particularly in the owner’s equivalent rent component.

HOUSE THEMES / ARTICLES

Digital Infrastructure Security and the “5th Dimension”

Fake News: Facebook to Limit Reach of Personal Accounts That Spread Misinformation - BBG

Under the new system, Facebook will “reduce the distribution of all posts” from people who routinely share misinformation, making it harder for their content to be seen by others on the service. The company already does this for Pages and Groups that post misinformation, but it hadn’t previously extended the same policy to individual users.

The moves are the latest in Facebook’s effort to curb the spread of misinformation on its networks of nearly 3 billion users. The more interesting debate will be between the rights of private businesses (to protect their reputations and deny business to those they deem a threat to profits) verse the growing backlash over “censorship” of politically aligned propaganda and fringe groups with unorthodox (conspiracy) views.

Energy and Resource Transition

Court Order: Court orders Royal Dutch Shell to cut net emissions by 45 percent – PBS

Despite already investing heavily in low-carbon energy portfolio expansion the Hague’s court decision found that Shell still needs to do more to reduce emissions. The decision could set a precedent for similar cases against “polluting” multinationals around the world. The case in the Netherlands is the latest in a string of legal challenges filed around the world by climate activists seeking action to rein in emissions, but it is believed to be the first targeting a multinational company.

The Hague court did not say how Royal Dutch Shell should achieve the ordered cutback (or who should pay for it), saying the energy giant’s parent company “has complete freedom in how it meets its reduction obligation and in shaping the Shell group’s corporate policy.” Stepping back and acknowledging that climate change is a real threat, this development presents significant new risks to markets and “polluting” industries that are already losing access to financing options. Finally, there is nothing clean about where clean energy materials come from, (how do we define “polluting” multinationals?) because last we checked cobalt mining in the Congo wouldn’t make the Hague’s cut.

Shipping Fuel: Shipping’s Carbon-Cutting Fuel Tanks So Far Remain Empty – WSJ

The industry has agreed to boost the global fleet’s energy efficiency by at least 40% over the next decade and cut overall greenhouse-gas emissions from ship exhaust in half by 2050 compared with 2008 levels. Until a consensus is reached on how to accomplish this owners run the risk of buying the wrong type of cargo ship’s given the average lifespan is around 25 years and it takes around two years to build a cargo vessel.

The focus on new fuel sources marks the biggest change in ship power since the sector switched from coal to the high-polluting heavy oil known as bunker more than 100 years ago. The deadlines, set by the International Maritime Organization, the United Nations marine regulator in 2018, likely will become more stringent in 2023 when the body meets to review its strategy. The alternative fuels attracting the most attention and investment so far include ammonia and biofuels (but both have problems) but current orders for new ships still favor conventional approaches.

Fiscal Policy Expansion

Budget: Biden to Propose a $6 Trillion Budget to Make U.S. More Competitive - NYT

Documents obtained by The New York Times show that Mr. Biden’s first budget request as president calls for the federal government to spend $6 trillion in the 2022 fiscal year, and for total spending to rise to $8.2 trillion by 2031. The growth is driven by Mr. Biden’s two-part agenda to upgrade the nation’s infrastructure and substantially expand the social safety net, contained in his American Jobs Plan and American Families Plan, along with other planned increases in discretionary spending.

The levels of taxation and spending in Mr. Biden’s plans would expand the federal fiscal footprint to levels rarely seen in the postwar era, to fund investments that his administration says are crucial to keeping America competitive. Important to highlight that this does not include money for an expansion of public options for health care, which Biden will expand later with Congress. Two key takeaways, this is an initial proposal so things will likely change, and the economic team is being very conservative with their outlook on the growth effects of the budget.

Production, Inventory, and Logistical Bottlenecks

Pay Upfront: Tesla set to pay for chips in advance in bid to overcome shortage - FT

Tesla is set to take the unusual step of paying in advance for chips to secure its supply of the crucial materials and is also exploring buying a plant as part of efforts to overcome the global shortage. Tesla needs the newest generation mass-production chips, which are made mainly in Taiwan and South Korea, making buying their own plant likely a very long-term investment.

Some contract chipmakers have begun allowing large customers to pay deposits upfront to guarantee certain orders at a fixed price. Such a practice used to be highly unusual for contract chipmakers as the flexibility to allocate capacity to orders from different customers has long been a cornerstone of their profitability. Separately, GM announced this morning that they are opening 5 plants after securing the needed chip supply.

China Macroprudential Policy

Offshore: China Eases Offshore Funding Limit for Foreign Banks - BBG

The level smaller lenders and foreign banks operating in the country can borrow offshore was expanded this week after the People’s Bank of China raised the leverage ratio for such funding to 2 from 0.8 for institutions with capital of less than 100 billion yuan ($15.6 billion). Easing offshore borrowings will be to boon to foreign lenders including HSBC and JPMorgan Chase & Co. since their onshore operations have been handicapped by limited branch networks and access to deposits.

Foreign banks face stiff competition from domestic lenders, especially in consumer finance, and in recruiting top talent, which has made expanding in China challenging. High capital requirements, limited funding, and regulatory requirements have also proved onerous. The increased borrowing is unlikely to add much pressure to the recent yuan rally because foreign financial institutions, as well as multinational companies, are still subject to a foreign debt quota. China has been wary of offshore borrowings as it seeks to ensure the financial system as a whole is not too exposed to foreign debt that led to the Asian Financial Crisis in 1997.

Unipolar to Multipolar World

Taiwan: Risk of Taiwan Strait conflict ‘at all-time high’, Beijing-backed think tank says – SCMP

The think tank’s conclusion was based on an internally created index of the risk level of armed conflict across the strait, which the researchers put at 7.21 for 2021, on a scale of minus 10 to 10. It hovered above 6.5 for much of the 1970s but fell to 4.55 in 1978 when Washington established formal diplomatic relations with Beijing. The risk of conflict was also low in the 1990s, as the mainland embarked on economic reforms that drew investment from around the world, including Taiwan. The changing political dynamic across the Taiwan Strait and Washington’s closer relations with Taipei are two “destructive factors” driving up the risk of conflict currently.

The Economist this month labeled the Taiwan Strait as “the most dangerous place on Earth” as it is Beijing’s most sensitive territorial issue and a major point of contention between China and the US. Beijing claims self-governing Taiwan as its own territory and has not renounced the use of force to bring it under mainland control. We believe that Xi believes that the U.S. would be reluctant to use a military response to any attack/invasion on Taiwan but ultimately we see the threat of an attack/invasion as still highly unlikely.

Competition: Biden’s Top Man in Asia Says the Era of Engagement With China Is Over - BBG

Kurt Campbell, the U.S. coordinator for Indo-Pacific affairs on the National Security Council, stated the U.S. policy toward China will now operate under a “new set of strategic parameters,” Campbell said, adding that “the dominant paradigm is going to be competition.” Chinese policies under Xi are in large part responsible for the shift in U.S. policy, Campbell said, citing military clashes on China’s border with India, an “economic campaign” against Australia, and the rise of “wolf warrior” diplomacy.

China continues to push the narrative that the two countries “stand to gain from cooperation and lose from confrontation” as China Foreign Ministry Spokesman Zhao Lijian said at a regular press briefing Thursday, but the CCP actions and escalations tell a different story. As we have continued to say since Biden became President, there will likely be no de-escalation in the relationship. We are now watching how USTR Katherine Tai addresses the Trade Deal and how hard Biden pushes for a further investigation into the origins of Covid.

Thank you for reading - Mike