MIDDAY MACRO - 5/14/2021

Daily Color on Markets, Policy, and Geo-Politics

MIDDAY MACRO - DAILY COLOR – 5/14/2021

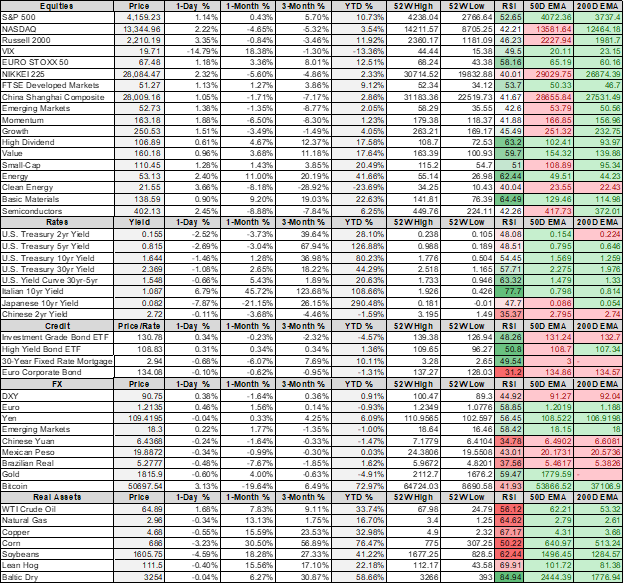

PRICE MATRIX

OVERNIGHT/MORNING RECAP / MARKET WRAP

Narratives:

Equities continue their post-CPI sell-off relief rally

Treasuries were well bid overnight but weaker post open

Ag complex is mixed as logistical issues continue to weigh on corn

WTI higher as pipeline focus fades

Price Action:

Equities melting higher on dip buying and dealer hedging

Russell/Nasdaq outperforming S&P

Momentum, Growth, Small-Caps factors outperforming

Technology, Cons. Discretionary, Energy sectors outperforming

Call wall is back at 4150 (4165) with support at 4100, 4125 is technical support with resistance at 4160-70

Major Asian indexes higher: Japan +2.3%. Hong Kong +1.1%. China +1.8%. India +0.1%.

European bourses higher from midday lows: London +0.6%. Paris +0.7%. Frankfurt +0.6%.

Treasuries bull flattening as long-end is outperforming

5yr = 0.82% and 10yr = 1.64%

WTI higher by 1.6% to $64.8

Copper lower by 1%, looks to be bull flagging

Aggs mixed as soy is outperforming corn and wheat

Corn futures tumbled by their limit Thursday on speculation that barges had been blocked by a crack in a bridge over the Mississippi River.

DXY under pressure overnight to 90.4

Gold higher by 0.7% to $1837

Bitcoin higher 6% to $51.3K

Econ Data:

Retail Sales: Retail sales were weaker than expected, remaining unchanged in April. This report does not suggest weakness on the part of consumers despite the unexpected drop in core retail sales measures in April. It is important to remember that these April declines follow massive increases in March (which were upwardly revised) and that core retail sales in April were still up 14.2% at an annual rate from the first-quarter average.

Import Prices: Total import prices rose 0.7% in March, slightly higher than expected. Import prices have surged 10.6% over the last 12 months versus a 7.0% gain on this basis in March. Inflation is the topic on the top of the minds of market participants, and this is the third April inflation report that surprised the upside. The import price inflation might be termed pipeline price increases, with lumber up 195.8% over the last year, unfinished metals up 47.6%, plastic materials up 18.9%, and finished metals up 15.1%. There is not much imported finished goods inflation at this point, with capital goods up only 1.3% over the last year and consumer goods prices up only 0.8%.

University of Michigan: The University of Michigan's consumer sentiment index fell to 82.8 in early May from 88.3 in April. Five-to-ten-year inflation expectations jumped 0.4% point to 2.7% in early April (this was 2.3% in February 2020), while one-year inflation expectations surged to 4.6% from 3.4% (versus 2.4% in February 2020). Consumers do not like inflation. This report shows that the price increases are beginning to feed into expectations with the 5-10 year price expectation at the highest rate since March 2011 and the one-year rate of 4.6%, the joint-highest reading since August 2008. The one-month increase in five-to-10-year inflation expectations was the largest in 28 years.

Analysis:

A continuation of positive price action in both equities and Treasuries today, showing that a growing inflation focus increases correlations between asset classes.

After more than a decade in mostly negative territory, the 60-day correlation between Treasuries and the S&P 500 Index has reached its highest level since 1999.

As a result, risk parity strategies (which depend on those two asset classes in particular hedging one another) have dropped 3% in the past four days.

The negative correlation between equities and bonds that has existed for the last two decades is not a permanent feature of markets and, in fact, contingent on low and not volatile inflation.

Given the growing probability of a more persistent inflationary pulse (that should have higher volatility), it is likely portfolio diversification benefits will be reduced, and this may, in turn, alter capital allocation and reduce leverage in the financial system.

Increases in more "transitory" components caused by supply or logistical disruptions and re-opening demand (used cars, leisure, and hospitality…) will continue to rise over the summer.

Longer-term slower-moving components like owners equivalent rent and healthcare are only now gaining momentum and likely to pick up speed over the summer as well.

Combining the pull and push these two types of inflation (as seen by the Fed) should bring this summer will likely increase inflation volatility.

Bottom line: We expect assets more generally to reflect a greater level of volatility over the summer, driven by higher levels of inflation (volatility), increasing cross-asset correlations, and reducing diversification benefits, forcing lower levels of risk-taking.

Increased policy uncertainty

Fed's conviction will be increasingly questioned.

Fiscal spending expectations fall as it is seen as inflationary.

Increased growth and earning uncertainty.

Increased concerns for a stagflationary environment next year.

Increased focus on companies' abilities to pass on rising costs and defend margins.

Reduced optionality levels, allowing a wider trading range.

Reduced retail trading activity and hence dealers hedging activity.

Reduced participation

by risk parity community and other volatility/correlation/diversification driven investors.

TECHNICALS / CHARTS

Four Key Macro House Charts:

Growth/Value Ratio:

Chinese Iron Ore Future Price:

5yr-30yr Treasury Spread:

EUR/JPY FX Cross:

S&P Correction:

This week’s correction (-5%ish) in the S&P has been well contained. The lower level of the larger longer-term channel (started March 2020) acted as support, with the index bouncing methodically off it. This rising support line has now been tested and held four times. Daily RSI has also reset to mid-range. Any true breakdown or correction in the current rally would need to break meaningfully through this channel. Although concerns are shifting towards a more stagflationary environment next year the technicals continue to support a further melt-up.

HOUSE THEMES / ARTICLES

Digital infrastructure security and the “5th Dimension”

Auto Data: China Seeks to Clamp Down on Auto Data Collection by Tesla and Others - Caixin

Draft rules published Wednesday by the Cyberspace Administration of China would ban the unapproved overseas transfer of data on Chinese road traffic and vehicle positioning, as well as images and other information gathered by onboard cameras and sensors. The move shows China, the world's largest auto market, is looking to wall off data that could inadvertently leak information on military installations and other sensitive areas.

The draft rules, which are based on a 2017 cybersecurity law, would apply not only to automakers and car dealers but also to ride-sharing services that use mobile apps. The restrictions span data on the type and amount of vehicles being driven on Chinese roads, facial recognition, measurements exceeding the accuracy of government-approved maps, and electric-vehicle charging networks. Where data is physically stored and who can access it will continue to be a sensitive subject between governments, firms, and consumers given the growing level of information being collected.

Surveillance: Student's Death in China Spurs Questions About Surveillance - WSJ

A student died on Sunday evening shortly after falling from a building on the campus of No. 49 High School in the city of Chengdu. The death in Chengdu caught public attention after a person claiming to be the student's mother posted messages on China's Twitter-like Weibo platform, accusing the school of first refusing to show her surveillance footage and later showing her only some of it. The incident was notable because of the outsize response it drew on Chinese social media, where a flood of people demanded to see the full recording.

Of the more than one billion cameras expected to be used for surveillance worldwide by the end of 2021, China is set to account for greater than 50%, according to industry researcher IHS Markit. That rollout has encountered little public resistance, though it has raised expectations around public safety and exposed authorities to bitter criticism when the surveillance systems fail or are misused.

Ransomware: Irish health service shuts down IT systems after 'sophisticated’ ransomware attack - CNBC

Ireland’s health service shut down its computer systems on Friday after being hit with a “sophisticated” ransomware attack. The attack was believed to have been perpetrated by the hacker group DarkSide. DarkSide is a relatively new group, but cybersecurity analysts believe they are dangerous.

The group claimed on Wednesday to have attacked three more companies, despite the global outcry over its attack on Colonial. Toshiba Tec, a division of Japanese tech conglomerate Toshiba, said its European business was the victim of a ransomware attack on May 4, according to Reuters. The company said the attack came from DarkSide.

Infrastructure

Broken Bridge: U.S. Coast Guard stops vessel traffic on Mississippi River around the damaged bridge at Memphis – WREG.com

Authorities in Arkansas and Tennessee, along with the U.S. Coast Guard, stopped all traffic related to the Hernando de Soto Bridge on Interstate 40 after inspectors discovered a crack in the steel structure. As of this morning, river traffic has been allowed to resume.

Another example of key physical infrastructure in need of repair or replacement. Also, another example of delayed logistics and transportation of goods in the country.

Commodity Cycle

Windfall: Commodities Boost Economic Recoveries, Mirroring Aftermath of Financial Crisis – WSJ

Australia, which accounts for more than 50% of global iron-ore exports, is an example of how fortunes can turn for the better when commodity prices run hot. On Tuesday, it unveiled a forecast budget deficit for the 12 months through June of 161 billion Australian dollars, equivalent to $126 billion. Six months earlier, it had expected the deficit would balloon to nearly 200 billion Australian dollars.

China’s inability to find alternatives to Australian Iron Ore supply while stopping coal imports again reinforces the limits China has when using its domestic markets as a geopolitical weapon. “The biggest buyer on the planet is buying it from the biggest seller on the planet,” said Stephen Halmarick, Commonwealth Bank of Australia’s chief economist. “There’s nobody else that can sell the quality and quantity that China demands.”

Logistical Bottlenecks

Car Inventory: Empty Lots, Angry Customers: Chip Crisis Throws Wrench Into Car Business – WSJ

The market mismatch is driving up prices, and many buyers expecting to drive new cars off the lot have to wait weeks or months for their vehicles to arrive. Some showroom models sell for thousands of dollars over the sticker price. Dealers had fewer than 2 million vehicles on the ground or en route to stores at the end of April, roughly half the normal number and the lowest level in more than three decades, according to research firm Wards Intelligence.

Automakers have been forced to cut production of more than 1.2 million vehicles in North America because they can’t get enough chips that are used for everything from safety systems to brakes and engines, research firm AutoForecast Solutions estimated. The timing couldn’t be worse. Shoppers flush with savings and federal stimulus checks are clamoring to buy. Automakers posted one of their best ever two-month stretches of U.S. vehicle sales in March and April.

Defining National Security Assets in a Dual Use Environment

Semiconductors: Chinese state media pushes back on chip nationalism after social media vilifies TSMC’s Nanjing expansion - SCMP

In a sign that Beijing is trying to temper nationalist sentiment, state-owned Xinhua News Agency has published an op-ed pushing back against the rising tide of discontent on the country’s social media against plans by Taiwan Semiconductor Manufacturing Co (TSMC) to invest almost US$3 billion to expand production at its Nanjing fab.

A good example of how stirring up nationalist animosity can hurt domestic growth and needed to be reigned in by Beijing. The op-ed emphasized that making chips is not only very difficult but represents the pinnacle of global cooperation. This highlights the greatest weakness China still has, an overreliance on foreign innovation.

Unipolar to Multipolar World

Trans-Pacific Partnership: USTR Katherine Tai under pressure on Asia-Pacific trade pact - SCMP

Tai’s hearing before the Senate Finance Committee reflected strong bipartisan support to re-engaging in the Trans-Pacific Partnership. “A number of us have talked about the TPP, whether in some revised and updated form, but the geopolitics of that seem very obvious as well as the economic benefits,” said Senator John Cornyn, a Republican from Texas.”

China’s exclusion from the TPP, negotiated during the administration of former President Barack Obama, was a key attribute for the US and other countries looking to check the regional influence Beijing had been gaining in tandem with its economic growth, even if such sentiments were never openly expressed. “In the absence of US leadership in the region, our allies will have to look elsewhere,” said Senator Crapo from Idaho. “If the United States has to pursue a worker-centered trade policy we need to be mindful that American workers lose when China writes the rules.”

Thank you for reading - Mike