MIDDAY MACRO - 10/12/2021

Daily Color on Markets, Policy, and Geo-Politics

MIDDAY MACRO - DAILY COLOR – 10/12/2021

OVERNIGHT/MORNING RECAP & MARKET ANALYSIS

Narratives/Price Action:

Equities are mixed, as inflationary fears continue to drive sentiment, with the S&P chopping around in the middle of its recent range

Treasuries are higher, with the curve notably flattening into this week’s long-end auction supply

WTI is higher, however off yesterday’s highs, and consolidating currently despite increased energy concerns in India and China

Analysis:

The S&P is little changed on the day, after partially recovering from a sell-off emanating out of Asia last night due to the growing energy crisis there, helping Treasuries get a better bid despite coming supply as traders await tomorrow's CPI data and the beginning of the 3rd quarter earnings season.

The Russell is outperforming the S&P and Nasdaq with Low Volatility, Small-Cap, and Growth factors, and Real Estate, Consumer Discretionary, and Utilities sectors all outperforming.

S&P optionality strike levels have the zero-gamma level moved higher to 4388 while the call wall is 4500. This Friday’s OPEX marks a substantial level of put interest rolling off, which could reduce downside hedge support. Until then, the large gamma strikes are 4300 and 4400.

The technical levels have support at 4345, then 4320, and resistance at 4460, then 4420. The S&P is in choppy waters, with big resistance for the current down channel around 4410-20, and the real test for a resumption of the melt-up at the 50dma which is around 4430.

Treasuries are higher, as the 5s30s curve is steeper by 4.4 bps, with 10yr yields still near recent highs going into today’s auction.

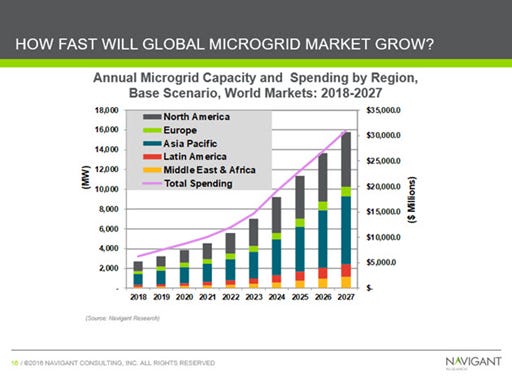

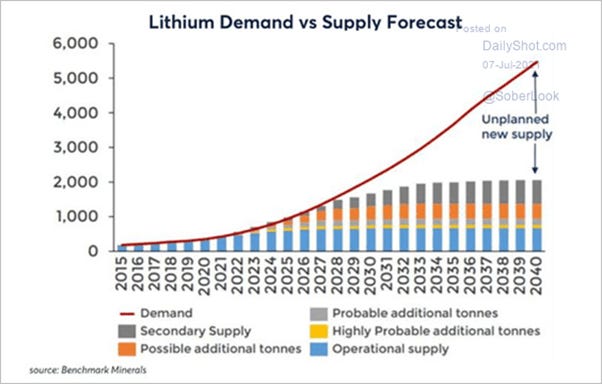

We are recommending the addition of a lithium and battery technology ETF ($LIT) to our (newly created) portfolio as we believe the current energy crisis will lead to broader adoption of energy storage batteries for microgrids (to store renewably generated energy) and EVs on top of the existing electrification and digitalization trends of increased mobile and IoT devices, all requiring significant more amounts of lithium batteries.

More broadly, we believe basic materials and energy prices will continue to rise due to fundamental mismatches in demand and supply, helping those sectors continue to outperform (since mid-September), supporting our general thesis of higher lithium prices and greater need for energy storage.

We also believe the current energy crisis has shown the need for energy storage to accompany renewable energy sources (the sun doesn’t always shine, and the winds don’t always blow), and although there will undoubtedly be new technological innovations in the future, the current realities support lithium-based batteries.

This developing trend, as well as the ever-increasing electrification and digitalization of our world, which is bringing more and more mobile devices and wearables along with increased electric vehicles and standalone robotic devices (drones, warehouse automation…), gives us conviction that demand will continue to increase (more than what is priced in).

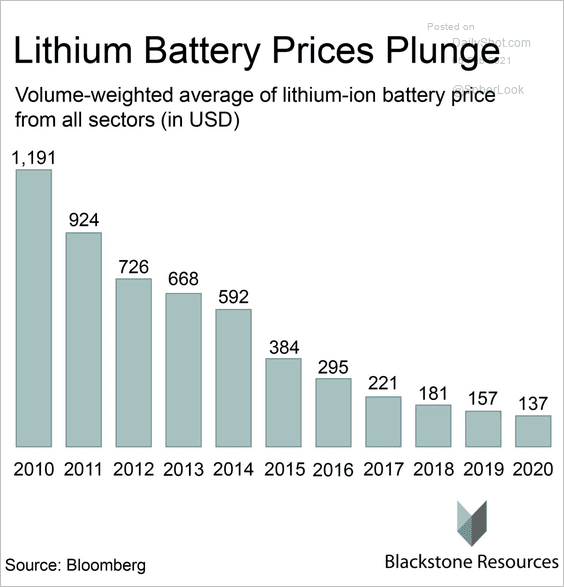

As a result, we believe lithium miners will benefit from rising prices (helped by better price discovery through a growing spot market), while battery companies will be able to pass on increased raw material input costs to end consumers due to the inelasticity of demand for their products while realizing more significant economies of scale in production, stabilizing recent price decreases and increasing profit margins.

We acknowledge this is not a groundbreaking investment theme and although we have highlighted it for some time (generally) are late in recommending an actual investment; however, we believe it is a critical area that one needs exposure to.

We see the Lithium & Battery Tech ($LIT) ETF as a good way to get broad exposure to these themes. The prospectus for the $LIT ETF can be viewed here (and please do your own homework) and shows the company/sector/country breakdowns as well as fee costs.

It certainly isn’t perfect with exposure to more speculative/expensive companies such as Tesla and 50% of the companies domiciled in China (which have broader micro/macro crosscurrents currently) as well as having appreciated 4X since pandemic lows. Still, we believe it is the right mix of various companies that will benefit from powerful trends for a retail-level investor.

Econ Data:

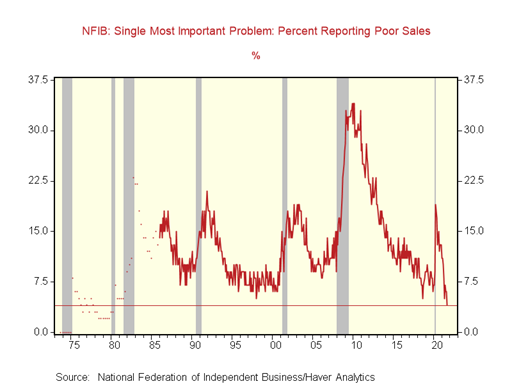

The NFIB Small Business Optimism Index edged down -1 pt to 99.1. The Uncertainty Index increased five points to 74. Owners expecting better business conditions over the next six months fell -5 pts to a net -33%. Fifty-three percent of owners reported capital outlays in the next six months, down two points from August and historically a weak reading. Of those making expenditures, 37% reported spending on new equipment, 21% acquired vehicles, and 12% improved or expanded facilities. Fifty-one percent of owners reported job openings that could not be filled, and a net 42% of owners reported raising compensation, both 48-year record highs. According to NFIB, the percent of small businesses reporting "poor sales" as their single most important problem fell to a fresh low of 4 in September, the lowest in several decades. The net percent of owners raising average selling prices decreased three points to a net 46% SA.

Why it Matters: Over 35% of owners report supply chain disruptions have had a significant impact on their business. Only 10% of owners reported no impact from recent supply chain disruptions. Labor shortages and intentions to increase wages slightly increased again. Despite this, positive profit trends increased one point, although still a net negative. “Small business owners are doing their best to meet the needs of customers, but are unable to hire workers or receive the needed supplies and inventories,” said NFIB Chief Economist Bill Dunkelberg. “The outlook for economic policy is not encouraging to owners, as lawmakers shift to talks about tax increases and additional regulations.” The bottom line, much of the same here, with no signs of improving fundamentals for small businesses, as continued shortages are increasing costs and weighing on sentiment.

The number of job openings dropped by 659k from a month earlier to 10.4 million in August, from an all-time high of 11.1 million and below market expectations of 10.9 million. It was the first month of decline in the level of the openings since December 2020. The largest decreases came from health care and social assistance (-224k), accommodation and food services (-178k), and state and local government education (-124k). Meanwhile, the number of hires declined by 439k to 6.3 million, while total separations (quits, layoffs and discharges, and other separations) were little changed at 6 million. The number of quits increased in August to 4.3 million (+242,000). The quits rate increased to a series high of 2.9%. Over the 12 months ending in August 2021, hires totaled 72.6 million, and separations totaled 66.7 million, yielding a net employment gain of 5.9 million.

Why it Matters: Again, another economic report that has the effects of Delta all over it. It also shows labor continues to have the upper hand in wage negotiations (after three decades of losing its share of profits). In conjunction with Friday’s jobs report, we continue to believe the worst of Delta’s effects on labor shortages have played out and things should gradually improve, helping reduce longer-term structural inflationary fears (wage-spiral). We see this concern/fear as different than the current cyclical inflationary concerns caused by supply chain disruption and energy price increases (supply-push and demand-pull) which are continuing to be seen by central banks as transitory. A self-sustained wage-spiral inflationary pulse would be much more problematic and increase the needed speed to tightening policy by the Fed. Currently, we still see a pandemic effected labor pool that will increasingly return to work in the coming months.

TECHNICALS / CHARTS

FOUR KEY MACRO HOUSE CHARTS:

Growth/Value Ratio: Growth is higher on the week, with the ratio unchanged on the day

Chinese Iron Ore Future Price: Iron Ore futures are higher on the week, up 1.75% today despite growing concerns that continued energy shortage will weigh on industrial output

5yr-30yr Treasury Spread: The curve is flatter on the week, as inflationary concerns are weighing more on the belly due to increased central bank tightening expectations

EUR/JPY FX Cross: The euro is higher on the week, breaking through the crosses Yen positive down channel

HOUSE THEMES / ARTICLES

MEDIUM-TERM THEMES:

Real Supply Side Constraints:

Chipped: China Auto Sales Drop as Chip Shortage Endures – WSJ

Sales of passenger cars in China in September fell 17% from a year earlier, the worst decline since March last year, as the global chip shortage continues to hold back the world’s largest auto market. In China, on top of shortages of car inventory, tight monetary policy, a weakened real estate market, and declining earnings in the manufacturing sector have hurt consumer confidence, said Cui Dongshu, secretary-general of the passenger car association.

Why it Matters:

The world’s major auto markets have been grappling with a historic chip shortage, and China hasn’t been spared. Aside from the semiconductor shortage, carmakers and component producers also face price increases for materials including cobalt, lithium, steel, and aluminum, according to China’s auto industry regulator, automakers, and suppliers. As Chinese consumer demand is typically strong in the fourth quarter, the impact of supply chain disruptions on sales is likely to be further magnified into year-end.

Enduring: ‘It’s Not Sustainable’: What America’s Port Crisis Looks Like Up Close – NYT

U.S. ports are contending with a staggering pileup of cargo, something that once seemed like a temporary phenomenon, is now increasingly viewed as a new reality that could require a substantial refashioning of the world’s shipping infrastructure. It is not merely that goods are scarce. It is that products are stuck in the wrong places and separated from where they are supposed to be by stubborn and constantly shifting barriers.

Why it Matters:

The supply chain is overwhelmed and operating at an unsustainable level. There are numerous plans for port expansions, but this will not alleviate the current situation. If anything, given the increase in the capacity set to come online, the shipping industry will eventually be entering a reversal of the current period, with falling shipping costs and increased automation of the end-to-end logistical process. We will first need to get through the holiday seasons (Western and Chinese) before a peak in consumer demand can reduce supply chain pressures.

China Macroprudential and Political Tightening:

Now the Banks: China Starts Inspection of Financial Regulators, State Banks - Bloomberg

China is inspecting the nation’s financial regulators, biggest state-run banks, insurers, and bad debt managers for the first time in six years to root out corruption. A team led by the Central Commission for Discipline Inspection will start a two-month anti-graft check of the China Banking and Insurance Regulatory Commission and accept complaint reports from whistleblowers until December 15.

Why it Matters:

Chinese President Xi Jinping is zeroing in on the ties that China’s state banks and other financial stalwarts have developed with big private-sector players, expanding his push to curb capitalist forces in the economy and root out corruption. While previous tours covered other central and local government agencies and state-owned companies, the latest zeros in on entities including the People’s Bank of China, the China Securities Regulatory Commission, the Shanghai and Shenzhen stock exchanges, the biggest state-owned banks, as well as bad-debt managers including China Huarong Asset Management Co.

LONGER-TERM THEMES:

Electrification and Digitalization Policy:

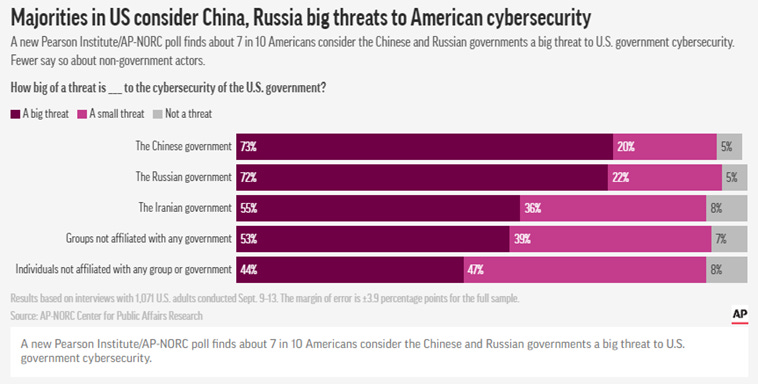

Key Issue: Cyberattacks concerning to most in U.S.: Pearson/AP-NORC poll – AP News

A poll by The Pearson Institute and The Associated Press-NORC Center for Public Affairs Research shows that about 9 in 10 Americans are at least somewhat concerned about hacking that involves their personal information, financial institutions, government agencies, or certain utilities. About two-thirds say they are very or extremely concerned. Roughly three-quarters say the Chinese and Russian governments are major threats to the cybersecurity of the U.S. government, and at least half also see the Iranian government and non-government bodies as threatening.

Why it Matters:

The broad consensus highlights the growing impacts of cyberattacks in an increasingly connected world and could boost efforts by President Joe Biden and lawmakers to force critical industries to boost their cyber defenses and impose reporting requirements for companies that get hacked. Biden has made cybersecurity a key issue in his young administration, and federal lawmakers are considering legislation to strengthen public and private cyber defenses. We are, however, in early innings here with the U.S. behind.

Commodity Super Cycle Green.0:

Parabolic Too: Energy crunch sees LNG carriers head the way of capesizes – Splash247

LNG shipping rates have followed the parabolic path of LNG prices in Asia and Europe, which have spiked to record levels in the past ten days. A new report from Evercore ISI shows LNG shipping rates for modern ships, which were languishing around $50,000 a day in late September, have more than doubled in the last two weeks alone, with Fearnleys quoting $120,000 a day for vessels.

Why it Matters:

When demand-driven spikes drive commodity prices skyward, the ships needed to meet these needs usually join along for the ride. As the energy shortage potentially deepens as temperatures get colder into winter, there is a good chance that the substitution of more abundant oil for coal and LNG could have a similar impact on the tanker market that is just starting to show signs of life.

Greenwashing: Rise of the ‘carbon neutral’ hydrocarbons - FT

About 30 liquefied natural gas offset deals have been agreed since 2019, with BP, Total, and Gazprom among companies to have sold cargoes. The cost of buying enough carbon offsets to cover the emissions from the production, transport, and use of one LNG cargo rose from about $1.1m in July to $1.8m in September as offset prices rose, according to S&P data.

Why it Matters:

Many companies are looking to make polluting activities more palatable by coupling them with carbon capture technology or carbon offsets. Each offset, generated by projects such as planting trees, is supposed to represent a tonne of carbon that has been permanently avoided or removed from the atmosphere. The developing trend of pairing them with LNG cargoes comes amid rising skepticism about the role of natural gas in the energy transition (due to high carbon intensity) while also increasing the overall cost.

Blue Ammonia: Ammonia terminal and storage facility to be built at the Port of Rotterdam – Port Technology

Norwegian clean energy company Horisont Energi has signed a Memorandum of Understanding with Koole Terminals B.V. to develop an ammonia terminal and storage facility at the Port of Rotterdam. The agreement will see both companies explore the establishment of a strategic and collaborative relationship for storage of ammonia produced and shipped from Norway to Rotterdam, as well as technical and commercial conceptual models for storage of ammonia products, services solutions, and technologies for further distribution to meet forecasted demand.

Why it Matters:

Ammonia, along with hydrogen and biofuels, will play an increasing role in future liquid energy carriers, so we want to highlight this significant development. Currently, producers, suppliers, and end consumers are only starting to develop relationships and create storage, handling, and transportation infrastructure. We will be closely watching to see if any of the emerging “green” fuel sources begin to gain market share (against the other), but we are still very early innings, and it seems demand is strong enough to allow parallel growth.

ESG Monetary and Fiscal Policy Expansion:

Well Subscribed: EU’s first green bond attracts more than €135bn of orders – FT

The €12bn sale of 15-year debt attracted more than €135bn of orders and marked the largest green bond deal, narrowly eclipsing the UK’s £10bn debut last month. Tuesday’s issue is the first of an expected €250bn of the European Commission green bonds, making up about a third of the bloc’s €800bn Covid-19 recovery fund. Brussels’ green bonds will be based mainly on the EU’s sustainable finance rules known as the taxonomy, although this has yet to be finalized as governments are split over whether to include gas and nuclear as green activity.

Why it Matters:

The EU attracted strong demand from investors for its inaugural green bond on Tuesday, as Brussels kicked off its efforts to become the world’s biggest issuer of sustainable debt. Brussels has joined a host of member states, including Germany, France, Spain, Italy, and Poland, in issuing green debt. Demand for green securities has been intense owing to the fund management industry’s focus on ESG. The bottom line, expect much more issuance given the strong demand backdrop, increasing the number of green endeavors that will be coming.

VIEWS EXPRESSED IN "CONTENT" ON THIS WEBSITE OR POSTED IN SOCIAL MEDIA AND OTHER PLATFORMS (COLLECTIVELY, "CONTENT DISTRIBUTION OUTLETS") ARE MY OWN. THE POSTS ARE NOT DIRECTED TO ANY INVESTORS OR POTENTIAL INVESTORS, AND DO NOT CONSTITUTE AN OFFER TO SELL -- OR A SOLICITATION OF AN OFFER TO BUY -- ANY SECURITIES, AND MAY NOT BE USED OR RELIED UPON IN EVALUATING THE MERITS OF ANY INVESTMENT.

THE CONTENT SHOULD NOT BE CONSTRUED AS OR RELIED UPON IN ANY MANNER AS INVESTMENT, LEGAL, TAX, OR OTHER ADVICE. YOU SHOULD CONSULT YOUR OWN ADVISERS AS TO LEGAL, BUSINESS, TAX, AND OTHER RELATED MATTERS CONCERNING ANY INVESTMENT. ANY PROJECTIONS, ESTIMATES, FORECASTS, TARGETS, PROSPECTS AND/OR OPINIONS EXPRESSED IN THESE MATERIALS ARE SUBJECT TO CHANGE WITHOUT NOTICE AND MAY DIFFER OR BE CONTRARY TO OPINIONS EXPRESSED BY OTHERS. ANY CHARTS PROVIDED HERE ARE FOR INFORMATIONAL PURPOSES ONLY, AND SHOULD NOT BE RELIED UPON WHEN MAKING ANY INVESTMENT DECISION. CERTAIN INFORMATION CONTAINED IN HERE HAS BEEN OBTAINED FROM THIRD-PARTY SOURCES. WHILE TAKEN FROM SOURCES BELIEVED TO BE RELIABLE, I HAVE NOT INDEPENDENTLY VERIFIED SUCH INFORMATION AND MAKES NO REPRESENTATIONS ABOUT THE ENDURING ACCURACY OF THE INFORMATION OR ITS APPROPRIATENESS FOR A GIVEN SITUATION.