Hot Mics and Head Fakes: Fed Re-Emphasizes Inflation Going into Next Week’s CPI Report - Midday Macro – 11/10/2023

Hot Mics and Head Fakes: Fed Re-Emphasizes Inflation Going into Next Week’s CPI Report - Midday Macro – 11/10/2023

Color on Markets, Economy, Policy, and Geopolitics

Hot Mics and Head Fakes: Fed Re-Emphasizes Inflation Going into Next Week’s CPI Report

Midday Macro – 11/10/2023

Market’s Weekly Narrative and Headlines:

Today’s more risk-on tone, driven by an outperformance of large-cap growth, which occurred all week more generally, is saving what was increasingly looking like a reversal in last week’s fortunes. As we highlight in our “Deeper Dive” section, this week’s catalysts skewed more negatively with too many Fed speakers to keep track of, SLOOS data that moved sideways, and three major Treasury auctions, on top of little new economic data outside of today’s University of Michigan Survey, which showed on aggregate a more negative level of consumer sentiment and higher inflation expectations, albeit notably differentiated by wealth levels and political affiliation. Many Fed officials, including Powell, walked back worries of tighter financial conditions (given declines in longer-dated yields) and struck a more hawkish tone, reinforcing that the Fed may not be done raising rates and is certainly not near easing policy. Throw in a large amount of Treasury supply, which culminated in a historically terrible 30-year auction due to low demand and technical problems from a primary dealer, and equities saw leadership change throughout the week while the Treasury curve flattened. Small caps gave up about 2/3rds their gains from last week, while the Nasdaq is pushing in new recent highs after the S&P put in a rare eight days of gains.

Oil looks to be attempting to put in a base after WTI hit $75 midweek, with two weeks of relentless selling slowly ending. Traders focused on the growing levels of production and inventory even as demand estimates stabilized and grew. The energy complex, from RBOB to natural gas, was generally under more pressure these last few weeks. Copper was also lower on the week, as the constant drip of fiscal stimulus out of China is wearing thin while demand elsewhere looks more mixed. The agg complex continues to be a tale of two cities, with softs continuing to outperform hards as grain supply rose further while increased demand for beans has supported prices there. Finally, the dollar retraced some of last week’s weakness, with the $DXY finishing the week near 105.8. The yen continued to drift higher, while the Euro was also weaker on the week. AUD failed to keep gains despite a rate hike from the RBA and an upgrade in inflation expectations.

Deeper Dive:

We continue to have a low level of conviction in our market outlook. Our high level of uncertainty over the path of the economy and inflation makes us neither overly optimistic nor negative on risk sentiment. Hence, we expect a choppy rangebound environment until there is clear evidence that the demand-pull forces on inflation have subsided meaningfully enough to allow the Fed to change its tune and begin to tease markets with “talks of talks” of rate cuts. This still requires a below-trend period of growth, something we believe is starting now, as higher frequency data increasingly picked up a slowing in consumer activity in October. However, this slowing in spending data and increasing weakness in both business and consumer sentiment readings come alongside a still historically strong labor market and a potential further firming in inflation readings next week. This has left Fed officials having a tough time communicating their policy outlook, balancing the uncertain effects of tighter financial and credit conditions with worries that policy is still not restrictive enough given the economy's strength. As a result, we see Treasuries more rangebound and biased towards a flatter curve. This will cap how far risk assets can rally, given a cooling growth backdrop likely means gains in stocks will come from multiple expansion versus actual earnings growth. In summary, our expected lack of progress on inflation over the next few months will counter any weakening in economic activity, keeping the Fed in a “higher for longer” stance well into Q1 before the totality of the data can finally give markets greater clarity on how long policy will be held in restrictive territory.

*Sentiment got very bullish very quickly last week, with cooler heads prevailing this week

*Credit card spending cooled in October, according to BofA data

*There is a lot of uncertainty over the lagged effect of tighter policy on top of tighter credit and financial conditions

As last week provided a string of positive catalysts that supported a broader risk-positive tone, which caused the largely short covering rally to grow over the week, this week’s lack of new economic data, more hawkishly toned Fed speakers, and Treasury supply has again changed the narrative to a more neutral setting. All eyes will now be on next week’s string of inflation data, especially the CPI report, because, once again, inflation is front and center after Powell re-emphasized that monetary policy may not be sufficiently restrictive and that inflation data has done “head fakes” before. As a result, we will be in this dove-hawk-swinging Fed pendulum world for a while as Fed officials stress their more two-side risk-management meeting-to-meeting, let’s look at the “totality” of the data approach. With that said, we will use the rest of our “Deeper Dive” section to highlight a few good things occurring in the U.S. economy. We plan to cover the bad in next week's writing.

*Tighter credit conditions are indicating a high probability of a recession

*The 30yr auction’s tail was one of the worst seen in a long time, renewing fears about future demand in light of increased supply

Turning to the positives first, third-quarter earnings grew at a near 3.7% pace, while revenue is on track to grow 2.3% from a year ago, according to FactSet. This was mainly driven by margins holding up better than expected, as firms generally noted a better ability to manage costs while still enjoying some pricing power on aggregate. Of course, individual sectors/industries are all experiencing this differently. On the other side, consumers saw real disposable income become positive and stabilize after being negative for much of the post-pandemic period. This supported spending as, despite job security weakening, the labor market remains tight by historical standards, allowing consumers to continue to drive growth. Although, as Fed officials are increasingly noting, there is a slowing in hiring, causing a better balance between demand and supply, an outright contraction through growing levels of layoffs seems unlikely to materialize into year-end. Moving forward, we would expect reduced spending on discretionaries like leisure and hospitality, but a still historically strong labor market, as seen during Q3, indicates a strong balance sheet and stable real disposable income story for Main Street may still have legs. Yes, access to credit is becoming harder and more expensive. Still, as this week's Fed data showed (highlighted in the “Policy Talk’ section), lending standards are changing more unevenly, with lower income/credit-scored individuals being hit hardest, while middle and higher income cohorts have seen greater stabilization or even loosening. Renewed rises in financial markets have also improved sentiment through the wealth effect channel. Further, the cost of gas is falling, freeing up disposable income. This will be offset by some of the drag from higher childcare costs and a resumption of student debt payments, but overall, it should support retail sales during the holiday season, especially for lower-income households.

*Margin expansion helped support Q3 earnings while sales grew at a more tepid 1% pace

*The average U.S. household balance sheet is still in pretty good shape

*Layoffs remain subdued, but it is taking longer to find a new job, consistent with a cooling labor market

*The national average price for gas continues to fall, with several states now having gas with a $2 handle

Finally, it is worth noting how significant the recent improvement in productivity is to the Fed, which wants to see increased participation rates and know that these workers are entering the workforce in a non-wage spiral inflation-accelerating way. Put another way, continued job creation does not need inflation-accelerating wage growth if new workers' unit labor cost is negative. Hence, the Fed can stop tightening even with an expanding labor market. Better productivity also supports harder data remaining resilient, such as factory orders and construction spending, as firms can weather any downturn better, as cooling input costs and higher productivity allow firms to navigate declining demand more effectively. Changing gears, it is also worth noting that higher rates, although punitive to many firms, especially smaller ones, can also be supportive given the general lack of leverage and credit demand currently due to the terming of debt taken and capex undertaken when rates were lower. Couple this with high levels of cash holdings, and nonfinancial firms have seen a decrease in their net interest expense.

*A boost in productivity is occurring again as firms learned to do more with less during the pandemic and invested heavily in digital and physical automation

*AI is likely to keep these productivity gains going for a while

*As a result, and music to the Fed’s ears, unit labor costs fell for all the right reasons in Q3

*Termed-out debt, low demand for new debt, and high cash balances have lowered the net interest expense firms are paying currently

*The mock portfolio has given up recent gains in its FX positions due to a stronger dollar this week, while our long long-dated Treasury position is higher

As always, thank you for reading, and please share our newsletter.

Feel free to reach out with any questions or comments.

- Michael Ball, CFA, FRM

Policy Talk:

A significant amount of Fed officials spoke this week, covering both economic and policy outlooks but also regulatory and other more niche topics. We highlight key takeaways in this week’s “Policy Talk” section. Chairman Powell, as always, stole the show, giving opening remarks at the "Monetary Policy Challenges in a Global Economy" panel at a conference hosted by the IMF, effectively reiterating comments made last week in a more hawkish way and more forcefully pushing back on the belief the Fed was done tightening policy. He highlighted that the real Fed fund rate level was above 2%, making policy "probably significantly restrictive." He again noted the balance of supply and demand in labor markets was “gradually easing.” He, however, was “attentive” to the risk that stronger growth could undermine recent progress in restoring the balance there and jeopardize the goal of moving inflation back to target. As a result, he continued to be “gratified” by the retreat in price pressures but, given past “head fakes” where core PCE has proven more persistent than policymakers expected, was “not confident that the Fed had achieved a “stance” that was sufficiently restrictive. However, he stressed that the Fed would continue to move carefully, making decisions meeting by meeting based on the totality of the data. Powell concluded by focusing on the “difficult questions” that the zero lower bound created for policymakers during periods of stress like the pandemic, noting the Fed would be starting their next “five-year” review of its framework in the second half of next year, and this would be at the heart of the review.

The interim president of the St. Louis Fed, Paese said the Fed “can afford to wait for further data,” supporting the decision last week to leave rates unchanged while giving prepared remarks on the economy and policy in Kentucky. She noted that businesses she hears from indicated inflation pressures and labor shortages were easing. In an interview with the WSJ, Chicago Fed President Goolsbee said the Fed must closely watch the effects of higher longer-term bond yields on the real economy. “The historical evidence suggests that long rates, even more than short rates, have a very substantial effect on real economic performance in a number of predictable areas—construction, investment, consumer durables,” Goolsbee said. Richmond Fed President Barkin pushed back on this on a webcast with MNI on Thursday, saying the movement in long-term bond yields may be capturing headlines, but it isn’t a great guide for deciding what to do with interest rates. “I don’t think long rates are quite useful as a policy variable,” Barkin said, adding, “They can move, you know, pretty significantly over a relatively short time period.” Minneapolis Fed President Kashkari spoke on Bloomberg TV and in an interview with the WSJ, arguing it was safer to overtighten policy in the current situation rather than allow inflation to remain persistent and not fully fall back to target. “Undertightening will not get us back to 2% in a reasonable time,” he said.

Governor Cook gave prepared remarks at Duke University and later in Dublin, Ireland,on the economy, policy, and financial stability, where she noted that U.S. households, businesses, and banks were still in stable shape. She highlighted that household debt such as car loans, credit cards, and mortgages “remains at modest levels.” In addition, most of the debt is owned by those with “strong credit histories or considerable home equity,” she added. Meanwhile, at the Cleveland Fed, a search is in the works for a new president as Loretta Mester approaches retirement. Governor Bowman continued her campaign to push back on the recent uptick in new regulation in a speech in Palm Beach, Florida. She covered her views on the economy and policy before delving into regulatory issues, where she highlighted “considerable progress” on lowering inflation but still sees parts of core service inflation as problematic. As a result of that and the resilience in the economy more generally, despite improvements in the balance of the demand and supply of labor, she expects the Fed will need to increase rates further. She commented that the reason for the rise in term premiums was unclear but saw the rise in longer-term yields as volatile while also noting that Treasury market liquidity has “held up well.” She went on to give a rather lengthy review of the ongoing reform of the bank regulatory framework. Several other Fed officials (Jefferson, Williams, Waller) spoke throughout the week, but in general, the mosaic of the message turned more hawkish given the loosening of financial conditions since the November FOMC meeting. We go into further detail below on Bostic and Barkin, who both spoke numerous times this week, and Dallas Fed President Logan, given she was the first to highlight the worries that rising yields could supplement a further rate hike.

Atlanta Fed President Bostic and Richmond Fed President Barkin both spoke at a Central Bank Business Survey Conference hosted by the Atlanta Fed. Bostic noted the current stance of policy was sufficiently restrictive. He was confident inflation would get to 2% and expects policy to remain restrictive “until that happens, or until we are sure that is going to happen.” Bostic echoed comments he made last week in an interview on Bloomberg TV and has been one of the most dovish policymakers, arguing since the summer that the Fed should hold off on further rate hikes as the cumulative tightening of policy to date was enough to re-trend inflation back to target. He saw tighter credit conditions, distress in commercial real estate markets, and a reduction in labor hoarding as signs that growth was cooling and policy was working. He also highlighted improvements in labor productivity as an “unsung story of the more recent period,” changing the labor market tightness-inflation dynamics as it lowers labor costs. Barkin indicated he believed there was a wide range of possible economic outcomes, and the stronger-than-expected Q3 GDP reading countered anecdotal evidence he has heard from businesses he speaks with. He also believed that the real economy had yet to feel the full effects of the Fed’s tighter policy, and a slowdown in activity is coming.

“They’re not looking to lend as robustly as they might have otherwise. And when they do, it’s usually for less than they would have before. So I think there is clear evidence of the slowdown, and that mindset I don’t expect will change in the next several months.” – Bostic

“But if there’s heightened productivity happening, if hiring is happening, that’s all on the supply side. And if you do your charts on a piece of paper, if the supply moves out, you can get more growth, and prices can come down. And so that’s part of the dynamic that I think has been quite interesting. Now, is this a new steady state? I don’t know.” – Bostic

“I believe there’s a slowdown coming, I believe we’re going to need that slowdown because I think that’s what it’s going to take to convince price-setters that the days of pricing power are over.” - Barkin

Dallas Fed President Logan gave remarks earlier this week where she came across as slightly more hawkish than her Octo 7th speech at a NABE Conference. She said she supported leaving policy where it currently is, given the uncertainty over the effects of tighter financial conditions on the real economy. As a reminder, Logan was one of the first Fed officials to highlight that the effects of rising long-end yields could supplement additional rate hikes, given the effect of tighter financial conditions on slowing the real economy. However, this week, she worried that inflation would have trouble getting from 3% to 2%. She noted that although loosening, the labor market remained too tight. She also noted that after the November FOMC, yields had fallen off highs, loosening financial conditions.

"We're going to continue to need to see tight financial conditions in order to bring inflation to 2% in a timely and sustainable way… I'm going to be looking at the data, and I'm going to be looking at financial conditions as we get closer to the following meeting."

The Board of Governors October Senior Loan Officer Survey showed banks continued to have historically tight standards for business and consumer loans in the third quarter. Still, things did not tighten further, as feared, with middle-sized firms seeing some easing in credit conditions. Banks reported tighter standards for commercial and industrial and CRE loans to firms of all sizes, and the tightening was accomplished in premiums for riskier loans, spreads of loan rates over the cost of funds, and costs of credit lines. There was weaker demand for loans from firms of all sizes. Many banks reported that the number of inquiries from potential borrowers dropped sharply. For household loans, banks reported that lending standards tightened across all categories of residential real estate loans other than government residential mortgages, for which standards remained unchanged. In addition, a “significant” number of banks tightened lending standards for credit cards, automobiles, and other consumer loans. Demand also weakened for consumer loans. The October SLOOS included a set of special questions that asked banks to assess the likelihood of approving credit card and auto loan applications by borrower FICO score in comparison with the beginning of the year. Banks reported that they were less likely to approve such loans for borrowers with FICO scores of 620 and 680 in comparison with the beginning of the year, while they were more likely to approve credit card loan applications and about as likely to approve auto loan applications for borrowers with FICO scores of 720 over this same period. The report also inquired about banks’ reasons for changing standards for all loan categories in the third quarter. Banks most frequently cited a less favorable or more uncertain economic outlook, reduced tolerance for risk, deterioration in the credit quality of loans and collateral values, and concerns about funding costs as important reasons for tightening lending standards over the third quarter.

*There was some reduction in the rate of tightening of standards in the third quarter

*Credit card loans saw a slight easing in standards, mainly due to higher FICO-scored borrowers, while auto loan standards were little changed

*Standards tightened further for multi-unit residential construction while non-residential construction eased slightly

*Demand improved from large and middle-sized firms while small ones weakened slightly

Total consumer credit increased by $9.06 billion in September, from a downwardly revised $15.7 billion decline in the previous month and below market expectation of an $11.7 billion rise. Revolving credit increased by $3.1 billion on the month, a 2.9% annual rise. Non-revolving credit, primarily auto and student loans, rose by $5.9 billion from the prior month, or a 2.4% annualized increase.

*Consumer credit saw both revolving and non-revolving credit rise on the month, recovering some of the decrease in the prior month

*Real revolving credit, or credit card balances, is still below pre-pandemic levels

Total household debt rose by 1.3% to reach $17.29 trillion in the third quarter of 2023, according to the latest Quarterly Report on Household Debt and Credit from the NY Fed. Mortgage balances increased by $126 billion to $12.14 trillion, while HELOC balances increased by $9 billion to $349 billion. Mortgage originations, measured as appearances of new mortgages on consumer credit reports and including both refinance and purchase originations, was $386 billion in Q3, a decline from the previous quarter and well below the trillion-dollar-plus quarterly origination volumes observed between 2020 and 2021. Credit card balances rose by $48 billion or 4.7% to $1.08 trillion. Auto loan balances increased by $13 billion to $1.6 trillion. Student loan balances increased by $30 billion to $1.6 trillion. Credit quality was steady, with 4% of mortgages and 16% of auto loans originating from borrowers with credit scores under 620. The median credit score for newly originated mortgages was flat at 770, while the median credit score of newly originated auto loans increased slightly to 719 from 716. Aggregate delinquency rates were increased in the third quarter of 2023. As of September, 3.0% of outstanding debt was in some stage of delinquency, up by 0.4 percentage points from the second quarter. The NY Fed’s Liberty Street Blog highlighted where credit card delinquencies were coming from in a recent blog post, noting that ‘even though the increase in delinquency appears to be broad based across income groups and regions, it is disproportionately driven by Millennials, those with auto or student loans, and those with relatively higher credit card balances.”

*The growth rate of auto loans has slowed while credit card debt has increased

*Credit card delinquencies have picked up, while other delinquency rates are more stable

*The combination of growing debt levels is making borrowers prioritize payments, with credit cards the last to be paid

The Atlanta Fed's Wage Growth Tracker was 5.2% in October, the same as for September. For people who changed jobs, the Tracker in October was 5.6%, also the same as in September. For those not changing jobs, the Tracker was 4.8%, down from 5.0% in September.

The National Financial Conditions Index (NFCI) ticked down to -0.36 in the week ending November 3, suggesting financial conditions loosened. Risk indicators contributed –0.16, credit indicators contributed –0.09, and leverage indicators contributed –0.10 to the index in the latest week.

U.S. Economic Data:

The University of Michigan consumer sentiment fell to 60.4 in November compared to 63.8 in October and forecasts of 63.7, preliminary estimates showed. The gauge measuring current economic conditions fell to 65.7 from 70.6, while future expectations declined to 56.9 from 59.3. Inflation expectations for the year ahead increased for a second month to 4.4%, reaching the highest since April, and expectations for the five-year outlook also increased to 3.2%, a level not seen since March 2011.

Key Takeaways: This was the lowest reading in six months, mainly due to growing concerns about the negative effects of higher interest rates and the ongoing wars in Gaza and Ukraine. “Overall, lower-income consumers and younger consumers exhibited the strongest declines in sentiment. In contrast, the sentiment of the top tercile of stockholders improved 10%, reflecting the recent strengthening in equity markets,” said Survey Director Joanne Hsu. The higher reading in inflation expectations mainly came from Republican-leaning respondents (4.9% one year ahead), while Independents were flat (4.3%), and Democrats continued to trend lower (2.4%). This was driven by gas price expectations, both over the short and long run, rising to their highest readings this year despite recent notable decreases in prices at the pump. In the final November report, we may see some notable revisions (improvements in sentiment and decreases in inflation expectations) as Republican drivers see increasing levels of $2-handle gas prices on the road and the situation in the Middle East potentially stabilizes.

*Sentiment readings broadly declined, keeping the post-summer negative trend alive

*Inflation expectations jumped notably higher due to Republican respondents

Technicals, Positioning, and Charts:

The Nasdaq outperformed the S&P and Russell on the week. Technology, Communications, and Industrials were the best-performing sectors, while Growth and Momentum were the best-performing factors. Large-cap growth was the best-performing size/factor combo.

@Koyfin

S&P optionality strike levels have the Zero-Gamma Level at 4322 while the Call Wall is 4400 and the Put Wall is 4000.

@spotgamma

S&P technical levels have support at 4400, then 4377, with resistance at 4465, then 4483.

@AdamMancini4

Treasuries are higher on the day, with the 10yr yield lower by 1bp to 4.61%, while the 5s30s curve is flatter by 5bp on the session, moving to 7 bps.

Four Key Macro House Charts:

Growth/Value Ratio: Growth is higher on the day and the week, with Large-cap Growth the best-performing size/factor on the week.

Chinese Iron Ore Future Price: Iron Ore futures are higher on the day and the week.

5yr-30yr Treasury Spread: The curve is flatter on the week.

EUR/JPY FX Cross: The Euro is stronger on the day and the week.

Other Charts:

AAII sentiment: "Bulls now at 42.6% (vs 24.3% last week) and Bears now at 27.2% (vs. 50.3% last week)...The one-week positive change in the Bull-Bear spread is the largest since January 2009." - Goldman Sachs

Last week’s rally increased equity exposure intentions.

The S&P remains historically expensive, mainly due to the “Magnificent Seven,” especially in comparison to small caps, which are now at extremely cheap valuation levels to their large-cap brethren.

Tighter financial conditions should increasingly weigh on the S&P 500 over time.

Better defense of margins saved the Q3 earnings season as top-line growth continued to weaken.

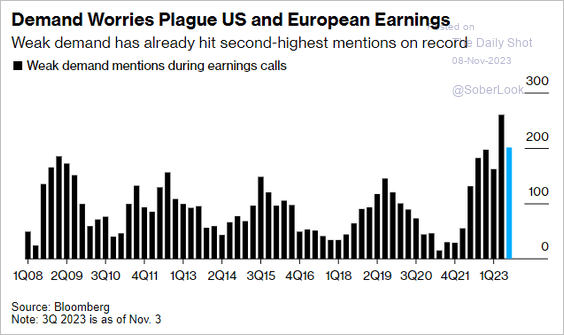

Companies remain very concerned about weaker demand.

An analysis of S&P 500 earnings calls reveals the number of discussions related to 'job cuts' across different sectors. Financials and Technology are leading the conversations - @M_McDonough

"Until earnings revisions breadth and performance breadth] reverse in a durable manner, we find it difficult to get more excited about a year-end rally at the index level." – Mike Wilson at Morgan Stanley

Tail of two cities in agg world, with softs hitting highs and grains oversupplied

Homebuilders are increasingly offering incentives.

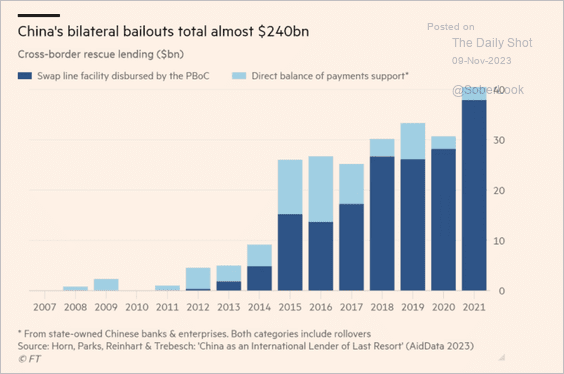

For China, the BRI has won valuable overseas business for its large state-owned enterprises and strengthened diplomatic ties with the countries in the so-called global south. Those links have increased China’s influence within other international organizations, such as the UN, and allowed it to advance Xi’s political vision for the world. However, Belt & Road bailouts have been accelerating.

Articles by Macro Themes:

Medium-term Themes:

China’s Post-Pandemic Life:

Inflection: The oil demand outlook in China, the world’s biggest importer, isn’t offering much inspiration to bulls as the end of the year approaches. Refining margins are falling, crude and fuel stockpiles are building, and a hoped-for sharp jump in air travel still hasn’t eventuated. That’s mirroring the situation in the wider economy, where business and consumer confidence remain low despite government efforts to juice growth. - China’s Oil Demand Outlook Is Worsening as Winter Approaches - Bloomberg

Old Playbook: China will accelerate the issuance and use of government bonds, according to new finance minister Lan Foan. The finance ministry will steadily promote the resolution of local government debt risk and increase efforts to better leverage the role of special bonds to boost the economy. "The Ministry of Finance will continue to implement a proactive fiscal policy, focus on improving efficiency, and better play the effectiveness of fiscal policy," said Lan, who also noted the "complex domestic and international situation." - China to accelerate issuance of government bonds, finance minister says - Reuters

Strained Ties: China’s premier, Li Qiang, pledged that his nation would expand access to markets and also boost imports, which have fallen this year. China’s No. 2 official also vowed “to protect the rights and interests of foreign investors in accordance with the law.” That comment came after a measure of foreign investment into the world’s second-largest economy turned negative for the first time since records began in 1998. The promise to boost imports from other nations comes despite the slowdown in the Chinese economy, which has hurt demand for goods from around the world. China earlier reported that imports decreased 6.2% in September, down for the seventh month in a row. - China’s Li Vows to Boost Imports, Expand Market Access – Bloomberg

Longer-term Themes:

Cyber Life and Digital Rights:

Walking Became More Difficult: For millions of Australians who could not pay for goods, book rides, get medical care or even make phone calls, a nine-hour near-total service blackout from the company which provides 40% of the country's internet became a lesson in the risks of a society that has moved almost entirely online. Optus, which is owned by Singapore Telecommunications, (STEL.SI) gave no explanation for the outage except to say it was investigating it. Most of its services were restored by the afternoon. For one talkback radio caller, the first sign something was wrong with Australia's second-largest internet provider, Optus, came when her cat's wifi-powered food dispenser failed to serve breakfast at 6:10 a.m. and her pet woke her.” - Chaos as Optus outage disconnects half of Australia - Reuters

A lot of Bots: The conflict between Israel and Hamas is fast becoming a world war online. Iran, Russia, and, to a lesser degree, China have used state media and the world’s major social networking platforms to support Hamas and undercut Israel, while denigrating Israel’s principal ally, the United States. The deluge of online propaganda and disinformation is larger than anything seen before, according to government officials and independent researchers — a reflection of the world’s geopolitical division. Officials and experts who track disinformation and extremism have been struck by how quickly and extensively Hamas’s message has spread online, boosted by extensive networks of bots and, soon afterward, official accounts belonging to governments and state media in Iran, Russia, and China — amplified by social media platforms. - In a Worldwide War of Words, Russia, China and Iran Back Hamas - NYT

A.I. All Day:

Nick Clegg: Facebook owner Meta is barring political campaigns and advertisers in other regulated industries from using its new generative AI advertising products, a company spokesperson said on Monday, denying access to tools that lawmakers have warned could turbo-charge the spread of election misinformation. Meta publicly disclosed the decision in updates posted to its help center on Monday night, following publication of this story. Its advertising standards prohibit ads with content that have been debunked by the company's fact-checking partners but do not have any rules specifically on AI. "As we continue to test new Generative AI ads creation tools in Ads Manager, advertisers running campaigns that qualify as ads for Housing, Employment or Credit or Social Issues, Elections, or Politics, or related to Health, Pharmaceuticals, or Financial Services aren't currently permitted to use these Generative AI features," the company said in a note appended to several pages explaining how the tools work. - Meta bars political advertisers from using generative AI ads tools - Reuters

Energy’s Midlife Crisis:

Purple Fuel: The Biden administration’s climate push has gotten little love from the other side of the aisle. Many Republicans have railed against the government’s subsidies for wind and solar, excoriated its support for electric vehicles, and decried moves to curb oil and gas. But one clean-energy candidate has broad support from some of the reddest parts of the U.S.: hydrogen. Hydrogen doesn’t produce carbon emissions when burned, and companies are looking at it for use in cars, power generation, and steel manufacturing. One feature is that it can be produced using either renewables or fossil fuels. Many environmentalists warn that the flexibility could end up hurting the climate by prolonging the use of oil and gas. But it is also a reason for hydrogen’s bipartisan appeal. - The Green Fuel That Even Red America Loves - WSJ

$24.7 Billion: Since the International Energy Agency was founded five decades ago, it has compiled data on the government research and development budgets devoted to energy in its 31 member countries, which now allocate more money to energy R&D than any other point in the past 50 years. For almost the entire period covered by the data set, nuclear energy has received the most R&D budget of any technology. Renewable energy saw growing research budgets through the 1970s and a similar peak in the early 1980s. The total then fell back until it steadily rose after receiving a huge boost in 2009, thanks to the US, and has remained in the range of $3 billion since 2014. Energy efficiency follows a different pattern. Unlike nuclear or renewables, its budget has grown steadily almost every year, having tripled from less than $2 billion at the start of the century to $6 billion in 2021. Efficiency is now the single largest recipient of IEA member countries’ energy R&D budgets. - Nuclear Is Out, Hydrogen Is In: Where Countries Put Energy R&D Money - Bloomberg

Food: Security, Innovations, and Climate Change Implications:

Moderate Intensity: Peru’s agricultural exporters are bracing for tough times as a second year of bad weather upends a prolonged period of growth that turned the Andean nation into a fruit and vegetable powerhouse. The El Nino weather phenomenon means revenue from farm shipments probably will shrink 5% this year and stay flat next year, said Gabriel Amaro, head of agribusiness group AGAP. That’s a trend breaker in an industry that grew through the depths of the pandemic and when El Nino last struck in 2017. The uninterrupted expansion made Peru the top exporter of grapes and blueberries and among the biggest suppliers of mangoes, asparagus, and avocados. - El Nino Is Set to Put an End to Peru's Long Run of Fruit Export Growth - Bloomberg

Lab Cultivated Meat: Just last week, the US Department of Agriculture gave the green light to two companies to make and sell their cultivated chicken products in the U.S. This is a huge milestone for the industry, and it’s been the talk of Future Food Tech this week. There had been a looming question about whether this sort of product would be legitimized and now it is, at least in the US. Cultivated meat had previously been approved only in Singapore, and it has been served in a restaurant there over the past couple of years. - Lab-grown meat just reached a major milestone. Here’s what comes next. - MIT Tech Review

Authoritarianism in Trouble?:

Change the System: Nearly two-thirds of U.S. adults (65%) say the way the president is elected should be changed so that the winner of the popular vote nationwide wins the presidency. A third favor keeping the current Electoral College system. Democrats and Democratic-leaning independents are far more likely than Republicans and Republican leaners to support moving to a popular vote system for presidential elections (82% vs. 47%). Ideological differences are wider among Republicans. A clear majority – 63% – of conservative Republicans prefer keeping the current system, while 36% would change it. - Majority of Americans continue to favor moving away from Electoral College – Pew Research

Other Articles of Interest:

Capital Risk Transfer: U.S. Bank are selling complex debt instruments to private-fund managers as a way to reduce regulatory capital charges on the loans they make. These so-called synthetic risk transfers are expensive for banks but less costly than taking the full capital charges on the underlying assets. They are lucrative for investors, who can typically get returns of around 15% or more. Regulators have been raising capital requirements for years, and they proposed even tougher measures after the banking panic that began in March. Higher interest rates are eroding the value of banks’ investment portfolios, which can also eat into regulatory capital levels. In most of these risk transfers, investors pay cash for credit-linked notes or credit derivatives issued by the banks. The notes and derivatives amount to roughly 10% of the loan portfolios being de-risked. Investors collect interest in exchange for shouldering losses if borrowers of up to about 10% of the pooled loans default. - Big Banks Cook Up New Way to Unload Risk – WSJ

Done So Well: The economy is still generating jobs, but the job market is moderating but not buckling, a message reinforced by a variety of data, including low levels of weekly unemployment claims and layoffs. This wasn’t the sort of job market the Fed expected. When policy makers offered projections last December, they forecast that the unemployment rate would average 4.6% in this year’s fourth quarter. Economists got it wrong, too. They put the chances of a recession within the next 12 months at 63%. By last month, they dropped the recession chance to 48%. The jury is out on what happens next. The cooling in the job market could turn into a lurch lower, for example, as the full effect of the Fed’s past rate increases begins to take hold. But the chances of the economy avoiding a recession seem stronger now than they did even a few months ago. - The Improbably Strong Economy – WSJ

Podcasts and Videos:

VIEWS EXPRESSED IN “CONTENT” ON THIS WEBSITE OR POSTED IN SOCIAL MEDIA AND OTHER PLATFORMS (COLLECTIVELY, “CONTENT DISTRIBUTION OUTLETS”) ARE MY OWN. THE POSTS ARE NOT DIRECTED TO ANY INVESTORS OR POTENTIAL INVESTORS AND DO NOT CONSTITUTE AN OFFER TO SELL -- OR A SOLICITATION OF AN OFFER TO BUY -- ANY SECURITIES AND MAY NOT BE USED OR RELIED UPON IN EVALUATING THE MERITS OF ANY INVESTMENT.

THE CONTENT SHOULD NOT BE CONSTRUED AS OR RELIED UPON IN ANY MANNER AS INVESTMENT, LEGAL, TAX, OR OTHER ADVICE. YOU SHOULD CONSULT YOUR OWN ADVISERS AS TO LEGAL, BUSINESS, TAX, AND OTHER RELATED MATTERS CONCERNING ANY INVESTMENT. ANY PROJECTIONS, ESTIMATES, FORECASTS, TARGETS, PROSPECTS AND/OR OPINIONS EXPRESSED IN THESE MATERIALS ARE SUBJECT TO CHANGE WITHOUT NOTICE AND MAY DIFFER OR BE CONTRARY TO OPINIONS EXPRESSED BY OTHERS. ANY CHARTS PROVIDED HERE ARE FOR INFORMATIONAL PURPOSES ONLY, AND SHOULD NOT BE RELIED UPON WHEN MAKING ANY INVESTMENT DECISION. CERTAIN INFORMATION CONTAINED IN HERE HAS BEEN OBTAINED FROM THIRD-PARTY SOURCES. WHILE TAKEN FROM SOURCES BELIEVED TO BE RELIABLE, I HAVE NOT INDEPENDENTLY VERIFIED SUCH INFORMATION AND MAKE NO REPRESENTATIONS ABOUT THE ENDURING ACCURACY OF THE INFORMATION. I MAY OR MAY NOT HAVE POSITIONS IN ANY STOCKS OR ASSET CLASSES MENTIONED. I HAVE NO AFFILIATION WITH ANY OF THE COMPANIES OTHER THAN EXPLICITLY MENTIONED.